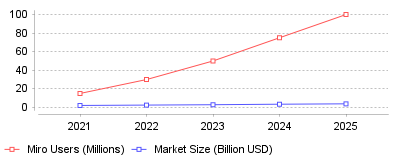

The data presented tracks the explosive growth of the visual collaboration and digital whiteboard market over the past five years, highlighting both overall market valuation and user adoption rates for industry leaders. This trend is particularly interesting because it demonstrates that visual collaboration tools have transitioned from niche pandemic-era utilities into permanent, enterprise-grade

| Year | Miro Users (Millions) | Market Size (Billion USD) |

|---|---|---|

| 2021 | 15 | 2.1 |

| 2022 | 30 | 2.5 |

| 2023 | 50 | 2.9 |

| 2024 | 75 | 3.44 |

| 2025 | 100 | 3.86 |

The data illustrates a relentless, compounding growth trajectory in both the user base of leading platforms like Miro and the broader collaborative whiteboard software market from 2021 to 2025 [source]. Specifically, Miro's user base skyrocketed from 15 million to over 100 million, while the global market size nearly doubled to reach approximately $3.86 billion [source]. This quantifies a decisive shift in how organizations facilitate teamwork, moving from physical conference rooms to boundless, cloud-based digital canvases.

On a micro level, this trend signifies that daily workflows for product, design, and engineering teams have fundamentally changed, relying heavily on infinite canvases for synchronous and asynchronous alignment [source]. Individual contributors are now utilizing these platforms not just for brainstorming, but for end-to-end project management, prototyping, and technical diagramming. On a macro industry level, visual collaboration tools have achieved mainstream enterprise adoption, effectively becoming a core pillar of the digital workplace alongside mainstays like Slack and Microsoft Teams [source]. Major enterprises are standardizing their tech stacks around these platforms, leading to lucrative multi-year contracts and aggressive market consolidation [source]. Consequently, vendors that fail to provide enterprise-grade security, data residency controls, and zero-trust architectures are rapidly losing market share to incumbents [source].

This rapid expansion is critically important because it redefines the benchmark for corporate productivity and cross-functional alignment in distributed environments. As businesses continue to navigate hybrid work models, the ability to centralize context, decisions, and creative processes in a single visual layer prevents information silos and reduces project friction [source]. Furthermore, the massive user scale achieved by these platforms creates powerful network effects, meaning that proficiency in digital whiteboarding is now a mandatory competency for modern knowledge workers [source].

The initial catalyst for this surge was undoubtedly the global transition to remote work during the pandemic, which forced teams to find digital alternatives to physical whiteboards [source]. However, the sustained growth over the last 12 to 24 months has been driven by the aggressive integration of generative AI capabilities directly into these platforms. Features like automated diagram generation, sticky note clustering, and AI-driven content summarization have drastically reduced the manual labor associated with digital collaboration, increasing the return on investment for enterprise buyers [source]. Additionally, the strategic bundling of these tools with existing software ecosystems, such as deep integrations with Atlassian, Workspace, and Microsoft 365, has eliminated friction and made adoption seamless for thousands of large organizations [source].

The digital whiteboard category has successfully evolved from a temporary remote-work solution into an indispensable, AI-powered innovation workspace. As platforms continue to expand their capabilities with workflow automation and advanced integrations, their influence over enterprise productivity will only deepen. The prominent takeaway is that visual collaboration is no longer just a digital substitute for physical whiteboards; it is the definitive, AI-powered central hub for enterprise productivity and agile business operations.

Global visual software deployments generated $1.17 billion in 2026. This market will reach $5.11 billion by 2035 at an annual growth rate of 17.79% [1]. Organizations moved past their initial remote adoption phase long ago. Corporate buyers now demand measurable returns on software investments rather than merely prioritizing connectivity. Active users of visual workspaces achieve a 349% return on investment over three years. This yields an average of $4.47 million in annual organizational benefits [2]. Analysts calculate that active daily users on major platforms work with the equivalent output of 320 additional full-time employees [2]. Enterprise adoption drives this expansion. Large organizations comprise 61% of total market usage [1]. Cloud-based deployments account for 70% of these installations. Software buyers reject ambiguous value propositions. The macroeconomic environment dictates that companies justify every licensing seat. Technology executives prioritize platforms that demonstrably accelerate project delivery timelines.

Miro achieved $665 million in annual recurring revenue in 2024. The company expanded its user base to over 100 million [3]. This scale affords the provider significant pricing power and development capital. The software vendor reached a $17.5 billion valuation following a $400 million funding round in 2022 [4]. While top vendors continue to capture market share, mid-market providers face operational headwinds. Mural executed multiple rounds of structural headcount reductions between 2023 and 2024 to simplify operations and manage costs [5]. The disparity between these two pure-play vendors illustrates a broader trend in software procurement. Enterprise buyers prefer consolidating software contracts over maintaining standalone applications. Organizations constantly evaluate their broader project management and productivity tools to eliminate redundant licensing. Platform incumbents possess a distinct advantage. They can bundle visual features into existing enterprise agreements at zero marginal cost. Standalone vendors must validate their premium pricing through superior interface design. Vendors failing to reach sufficient scale face severe acquisition risks. They struggle to fund necessary research and development cycles. Consequently, smaller providers either get acquired by larger portfolio companies or slowly bleed active users to integrated suites.

Adding software often decreases team output. Forty-five percent of workers use five or more productivity applications daily. Forty-two percent report frustration with fragmented communication channels [6]. Technology departments face mounting pressure to reduce this administrative burden. Atlassian capitalized on this operational friction by releasing Confluence Whiteboards. The vendor captured 600,000 board creations shortly after launch [7]. The company noted in its April 2024 earnings report that one technology customer saved $60,000 annually by switching from a competing visual tool to Atlassian's native offering [8]. Consolidation efforts reduce context switching. They also lower training costs for new hires. As software budgets tighten, IT leaders scrutinize their digital whiteboard and visual collaboration tools for overlap. The presence of multiple similar applications creates isolated information repositories across different departments. Marketing teams might use one vendor while engineering teams use another. This division prevents seamless cross-functional planning. Employees waste hours manually copying data between disparate systems. Unified platforms solve this fragmentation by centralizing work artifacts into a single database. Forrester research calculates that standardizing on a single collaborative suite can save a composite organization $758,000 in operating expenses over three years [6].

By 2026, 40% of enterprise applications will feature task-specific artificial intelligence agents [9]. Microsoft integrated Copilot directly into Microsoft Whiteboard to automatically organize user notes into thematic categories [10]. Zoom similarly embedded AI Companion into its unified client. This implementation generated $33.2 million in estimated productivity value for composite organizations by reducing manual meeting documentation [11]. Rather than starting from a blank screen, teams use brainstorming tools with AI idea generation to populate initial concepts rapidly. Zoom reports that 64% of its top-tier customers have enabled artificial intelligence features [12]. However, this rapid deployment introduces new management challenges. OutSystems research shows 94% of organizations worry that unchecked artificial intelligence deployments will increase technical debt and security risks [9]. The transition from manual input to automated generation requires strict governance. Administrators must ensure intelligent agents do not accidentally expose strategy documents to unauthorized internal users. Misconfigured permissions can allow search models to index highly sensitive financial projections and display them to junior staff members. Technology teams must establish clear guardrails before activating generative features company-wide.

Bizzdesign launched Unify in April 2026 to solve the disconnect between visual mapping and formal business architecture [13]. Traditional drawing applications lack structural data. When business analysts outline transformation plans, they draw diagrams that remain disconnected from infrastructure databases. Managers mapping out feature dependencies require digital whiteboard tools for product workshops that tie directly into underlying engineering databases. Bizzdesign Unify synchronizes live portfolio data with a canvas. This allows cross-functional groups to see technical constraints during the planning phase [14]. This integration prevents product teams from designing workflows that conflict with existing software architecture. By grounding visual sessions in actual enterprise data, companies accelerate their decision cycles. The market demands platforms that convert unstructured ideation into actionable execution tickets instantly. Freeform drawing holds little value if engineers must manually recreate those diagrams in separate tracking systems. Integration protocols ensure that moving a sticky note updates the corresponding database entry immediately. This bidirectional syncing eliminates manual data entry tasks completely.

The shift toward hybrid models altered how agencies present concepts to buyers. McKinsey found that 83% of employees prefer hybrid work arrangements [15]. This demographic preference forces services firms to adapt their delivery mechanisms. Agencies rely on specialized digital whiteboard tools for client collaboration to maintain presentation standards outside the corporate network. These external engagements require precise permission controls. Administrators must prevent clients from viewing internal comments or unrelated project boards. Teams structure these remote meetings using whiteboard tools with templates and frameworks to ensure external participants understand the interaction rules immediately. Establishing visual boundaries helps facilitators guide clients through design reviews without technical confusion. Poorly managed remote sessions damage client trust and prolong approval cycles. Consultants must master these digital environments to justify their billing rates. Buyers expect polished interactions that match the quality of traditional boardroom presentations. Visual software bridges this gap by providing professional collaborative spaces that function flawlessly across external firewalls.

The UK Competition and Markets Authority permanently altered software acquisitions when it blocked Adobe's $20 billion purchase of Figma [16]. Adobe and Figma mutually terminated the merger in December 2023. This cancellation triggered a $1 billion cash termination fee paid to Figma [17]. At the time of the deal's collapse, Figma generated approximately $600 million in annual revenue with a 40% year-over-year growth rate [18]. The regulatory intervention signaled that antitrust authorities will actively prevent incumbent suites from buying dominant standalone platforms. This forces visual workspace vendors to plan for independent profitability. Founders can no longer seek quick acquisitions by legacy software conglomerates. With $333 million in prior funding, Figma received a capital injection that nearly tripled its historical investment total [18]. The company can sustain operations indefinitely without public market pressure. Market competitors must now face a fully capitalized Figma operating independently rather than getting absorbed into the Adobe pricing structure. This independence requires vendors to build complete software suites rather than relying on eventual corporate buyouts.

Eighty-three percent of surveyed employees prefer flexible arrangements. Yet executive leadership teams struggle to maintain consistent productivity across distributed teams [15]. McKinsey research from 2025 shows that 34% of on-site employees report consistent focus. This compares to only 29% of remote workers [19]. This engagement gap forces managers to deploy interactive software. Active cursor tracking and real-time voting mechanisms prevent meeting attendees from multitasking. During virtual meetings with two or more participants, 52% of workers report actively multitasking instead of paying attention to the presenter [20]. Visual canvases force active participation. They require users to drag elements or contribute text physically. Organizations that fail to implement these participation methods experience higher project failure rates. They also face increased employee turnover. The same McKinsey study revealed that 39% of employees intend to quit their current roles [19]. This matches figures seen during the peak of pandemic resignation waves. Leaders must implement engaging digital environments to retain key talent.

Technology departments face mounting pressure to secure unstructured data residing on infinite canvases. When teams use public cloud applications for product planning, they create compliance vulnerabilities. Sixty-eight percent of visual deployments rely on cloud infrastructure [1]. This raises persistent concerns regarding intellectual property protection. Security and data privacy worries currently restrict adoption in approximately 30% of target organizations [1]. Administrators demand granular access logs to comply with regional privacy laws. Without these enterprise-grade security features, procurement teams will block software purchases. They do this regardless of end-user preference. Vendors must offer localized data hosting to satisfy European customers subject to geographical storage requirements. Atlassian specifically expanded its cloud data residency options to India, Japan, South Korea, Switzerland, and the United Kingdom [7]. This expansion captures risk-averse international clients. Providers lacking localized hosting capabilities automatically lose consideration during enterprise software evaluations.

Ineffective meetings drain corporate profitability. Zoom reported $4.6 billion in 2024 revenue. This metric reflects sustained enterprise reliance on virtual communication channels [21]. However, the average meeting length increased by 10% over the past 15 years [20]. This increase compounds organizational fatigue. To combat this inefficiency, 68% of workers identify virtual tools as crucial for team progress [20]. They rely on shared visuals to align objectives quickly. The modern enterprise cannot function using audio-only remote calls. Complex problem-solving requires shared visual context. Participants comprehend architectural diagrams exponentially faster when manipulating them synchronously. Video platform providers expanded into the whiteboard category explicitly to capture this adjacent value. They recognize that pure video transmission possesses limited pricing power. Zoom had 192,600 enterprise customers in late 2024 [21]. This provides a massive distribution channel for native collaborative features. Competitors must counter this distribution advantage through specialized use cases.

Video integration represents the next functional layer for visual workspaces. Atlassian acquired Loom and immediately embedded asynchronous video recordings directly into Confluence pages [8]. Users enhanced 23 million videos via Loom artificial intelligence features. This intelligence layer boosted viewer engagement by 18% [8]. This asynchronous capability allows distributed teams to explain complex diagrams across different time zones. They accomplish this without scheduling live meetings. A product manager in San Francisco can record a brief walkthrough of a wireframe. Engineers in Berlin can review the file the following morning. This asynchronous workflow reduces meeting frequency. It also preserves the nuanced verbal context often lost in static text comments. The combination of visual frameworks and recorded video creates a persistent knowledge asset. Subsequent hires can reference these recordings during onboarding. This reduces the administrative burden on senior staff members assigned to train new employees.

Product development cycles have accelerated drastically. Visual vendors push new functionality on a weekly basis to maintain parity with aggressive startups. During this competitive phase, market incumbents use their vast distribution networks to copy and scale emerging features. Microsoft routinely observes third-party innovations before integrating identical capabilities into Microsoft 365. This follower strategy works perfectly for enterprise software because procurement departments prioritize vendor consolidation over feature novelty. Specialized design firms will always prefer standalone tools like Figma or Miro. However, general business units typically accept whatever application their IT department provisions by default. Consequently, the battle for the enterprise market is won through distribution agreements rather than incremental software improvements. Companies focus their engineering budgets on administration panels rather than user interfaces. Compliance tracking drives renewal rates higher than aesthetic design updates.

The rigid boundaries separating different software categories continue to dissolve. Project management platforms now feature native whiteboards. Whiteboard applications now feature tracking boards and resource allocation monitors. This convergence creates a highly confusing purchasing environment for technology executives. A single company might accidentally purchase three different applications that perform the exact same core functions. Software providers encourage this category blurring because it allows them to increase their total addressable market. A visual collaboration vendor can justify a higher valuation multiple if investors believe it competes in the broader work management sector. Productivity platforms transitioned from simple task lists into exhaustive work operating systems. Visual tools follow this exact developmental roadmap. They aim to serve as the primary interface for all digital work. Users prefer conducting their daily operations from a single browser tab to avoid login fatigue.

Venture capital firms no longer subsidize unprofitable growth in the software sector. Between 2020 and 2022, visual tool companies hired aggressively to capture pandemic-driven demand. Now, these same organizations focus entirely on expanding their operating margins. This financial mandate trickles down to product strategy. Vendors restrict access to their free tiers. They force casual users into paid subscriptions. They introduce usage limits on artificial intelligence queries to control server costs. The era of unlimited digital canvases provided at zero cost has permanently ended. Consumers must adapt to stricter paywalls and aggressive monetization tactics. For enterprise customers, this translates to complex licensing negotiations. Account executives face immense pressure to upsell premium security features to existing accounts. Discounting strategies have vanished from the sales playbook entirely. Procurement teams must prepare for annual price increases across their entire visual software portfolio.

Chief information officers will increasingly demand modular application designs. Organizations refuse to pay for features their teams do not actively use. Future visual platforms must integrate seamlessly into existing chat interfaces rather than forcing users into separate browser tabs. The $1.17 billion visual collaboration market remains highly fragmented [1]. Economic pressures will force weaker vendors out of the enterprise tier. Success requires balancing intuitive design with stringent security architecture. The market will reward platforms that facilitate rapid idea generation while enforcing strict data hygiene. Software developers must prioritize application programming interface connectivity. This ensures their canvases function as open hubs rather than closed data silos. The separation between planning and execution will disappear completely as visual tools become direct control panels for underlying databases.

The data presented tracks the explosive growth of the visual collaboration and digital whiteboard market over the past five years, highlighting both overall market valuation and user adoption rates for industry leaders. This trend is particularly interesting because it demonstrates that visual collaboration tools have transitioned from niche pandemic-era utilities into permanent, enterprise-grade

| Year | Miro Users (Millions) | Market Size (Billion USD) |

|---|---|---|

| 2021 | 15 | 2.1 |

| 2022 | 30 | 2.5 |

| 2023 | 50 | 2.9 |

| 2024 | 75 | 3.44 |

| 2025 | 100 | 3.86 |

The data illustrates a relentless, compounding growth trajectory in both the user base of leading platforms like Miro and the broader collaborative whiteboard software market from 2021 to 2025 [source]. Specifically, Miro's user base skyrocketed from 15 million to over 100 million, while the global market size nearly doubled to reach approximately $3.86 billion [source]. This quantifies a decisive shift in how organizations facilitate teamwork, moving from physical conference rooms to boundless, cloud-based digital canvases.

On a micro level, this trend signifies that daily workflows for product, design, and engineering teams have fundamentally changed, relying heavily on infinite canvases for synchronous and asynchronous alignment [source]. Individual contributors are now utilizing these platforms not just for brainstorming, but for end-to-end project management, prototyping, and technical diagramming. On a macro industry level, visual collaboration tools have achieved mainstream enterprise adoption, effectively becoming a core pillar of the digital workplace alongside mainstays like Slack and Microsoft Teams [source]. Major enterprises are standardizing their tech stacks around these platforms, leading to lucrative multi-year contracts and aggressive market consolidation [source]. Consequently, vendors that fail to provide enterprise-grade security, data residency controls, and zero-trust architectures are rapidly losing market share to incumbents [source].

This rapid expansion is critically important because it redefines the benchmark for corporate productivity and cross-functional alignment in distributed environments. As businesses continue to navigate hybrid work models, the ability to centralize context, decisions, and creative processes in a single visual layer prevents information silos and reduces project friction [source]. Furthermore, the massive user scale achieved by these platforms creates powerful network effects, meaning that proficiency in digital whiteboarding is now a mandatory competency for modern knowledge workers [source].

The initial catalyst for this surge was undoubtedly the global transition to remote work during the pandemic, which forced teams to find digital alternatives to physical whiteboards [source]. However, the sustained growth over the last 12 to 24 months has been driven by the aggressive integration of generative AI capabilities directly into these platforms. Features like automated diagram generation, sticky note clustering, and AI-driven content summarization have drastically reduced the manual labor associated with digital collaboration, increasing the return on investment for enterprise buyers [source]. Additionally, the strategic bundling of these tools with existing software ecosystems, such as deep integrations with Atlassian, Workspace, and Microsoft 365, has eliminated friction and made adoption seamless for thousands of large organizations [source].

The digital whiteboard category has successfully evolved from a temporary remote-work solution into an indispensable, AI-powered innovation workspace. As platforms continue to expand their capabilities with workflow automation and advanced integrations, their influence over enterprise productivity will only deepen. The prominent takeaway is that visual collaboration is no longer just a digital substitute for physical whiteboards; it is the definitive, AI-powered central hub for enterprise productivity and agile business operations.