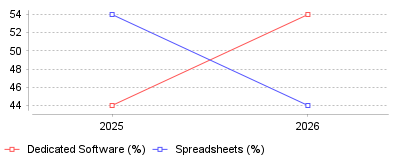

In 2026, the resource and capacity planning software market witnessed a pivotal turning point as dedicated management platforms finally overtook manual spreadsheets in adoption rates. Alongside this shift, the integration of artificial intelligence within these tools saw significant growth, with active utilization jumping over the last 12 months. This data is particularly insightful because it hig

| Year | Dedicated Software (%) | Spreadsheets (%) |

|---|---|---|

| 2025 | 44 | 54 |

| 2026 | 54 | 44 |

The data illustrates a historic crossover point in the resource and capacity planning software market occurring over the last 12 months. For the first time, the usage of dedicated resource management platforms (54%) has surpassed reliance on manual spreadsheets (44%), while active AI utilization within these tools grew from 11% to 17% between 2025 and 2026 [source].

On a micro level, this means that individual resource managers are spending less time reconciling conflicting data and more time acting on strategic insights. At the macro industry level, this transition indicates that professional services and IT firms are finally prioritizing unified delivery lifecycles, integrating capacity planning with financial management to protect project margins [source]. The shift also signifies that the capacity planning software market—projected to reach $6.47 billion by 2030—is maturing from basic scheduling into dynamic, execution-aware forecasting [source]. Furthermore, the rapidly rising consideration of AI functionalities suggests that the next competitive frontier will be predictive resource allocation, allowing businesses to make intelligent, autonomous capacity adjustments [source].

This technological evolution is critical because poor resource allocation continues to be a primary driver of project failure and eroded profit margins. With average industry utilization sitting at roughly 72%—well below the optimal 80% benchmark required for sustainable profitability—firms can no longer afford the critical blind spots inherent in spreadsheet planning [source]. Upgrading to dedicated capacity planning software prevents the over-provisioning of expensive cloud infrastructure and reduces unbudgeted last-minute hiring, directly translating into protected bottom lines and healthier work environments [source].

Several converging pressures have likely catalyzed this rapid abandonment of spreadsheets in favor of sophisticated capacity planning solutions. The increasing complexity of hybrid cloud environments, paired with remote, globally dispersed workforces, has simply outgrown the limited, two-dimensional capabilities of legacy manual tracking [source]. Additionally, strict mandates pushing for higher billable utilization rates and tighter cost controls have forced leadership to demand real-time visibility that spreadsheets inherently cannot provide [source]. It is also highly plausible that the recent democratization of machine learning features within these software suites has dramatically increased their perceived return on investment, making the switch an operational necessity rather than a luxury.

The resource and capacity planning category is currently experiencing a fundamental technological renaissance, shedding outdated manual constraints in favor of AI-augmented, predictive software. Organizations that fail to adopt these dedicated platforms risk severe competitive disadvantages, which are often characterized by persistent bench time, employee burnout, and chronic project delays. The most prominent takeaway is clear: in an era of tightening budgets and complex project demands, treating capacity planning as a manual administrative task is a recipe for failure, whereas leveraging dedicated, AI-driven software is the new baseline for organizational profitability.

The market for resource management software will expand from $6.2 billion in 2025 to $12.8 billion by 2035 [1]. Project portfolio management applications show a similar trajectory. That specific software segment will reach $16.87 billion by 2031 [2]. Organizations purchase these workload allocation platforms to solve a specific problem: balancing available human capital against incoming project demand. Managers can no longer rely on offline spreadsheets to track personnel availability across distributed teams.

Data reveals a severe gap between intent and execution. Eighty-six percent of business leaders regularly forecast employee capacity, yet only 6% consider their internal processes highly effective [3]. The utilization rate in professional services sits at 72% [3]. This figure falls well below the 80% benchmark required to maintain profitability. McKinsey found that companies using people analytics achieved a 25% productivity boost while reducing attrition rates by 50% [3]. Leaders integrate capacity algorithms directly into their broader tracking software suites to prevent employee burnout and track billable hours accurately.

Architecture choices define how quickly organizations can react to these capacity changes. The enterprise resource planning market reached $69.76 billion in 2023 and will grow to $175.87 billion by 2033 [4]. Cloud segments expand swiftly because organizations require immediate visibility for distributed teams [2]. Remote workers update their task progress via mobile applications, feeding live data back to the central engine.

Margin compression dominates executive discussions across the labor sector. Travel nurse revenue declined 37.1% in 2024 [5]. The travel nurse bill rate dropped to $89.78 that same year, representing a 16% annual decrease [5]. Agencies face a mathematical bind. They must maintain placement volume while capturing less revenue per worker.

Intermediation further reduces profitability. Eighty percent of travel nurse revenue now flows through managed service contracts, up from 73% in 2023 [6]. Industry aggregates show gross margins falling from 20.6% to 19.3% in a single reporting cycle [6]. Public companies feel identical pressure. AMN Healthcare reported a 250 basis point drop in gross margin during its latest fiscal year [6]. Agencies fight back by deploying shift-scheduling applications to organize their bench of available talent. They match credentialed workers to open orders before competing firms respond.

Hospital budgets offer no immediate relief to these staffing firms. Hospital median operating margins sat at just 2.1% in January 2026, restricting their ability to pay higher agency premiums [6]. Travel nurse weekly pay held at roughly $2,281 in early 2025 [6]. This rate remains essentially flat against late 2024 figures and trails the January 2020 baseline of $2,319 [6]. The average order fill rate for healthcare roles hovers around 47% [6]. Software that accelerates candidate compliance and credential verification directly increases that fill rate.

Contractors face severe personnel shortages despite an influx of public capital. The Associated General Contractors of America reported in 2025 that 92% of firms struggle to fill open positions [7]. Sixty-two percent of builders cite labor costs as their primary operational concern [8]. Public construction spending reached an annualized rate of $487.6 billion in May 2025 [9]. Agencies like the Department of Transportation and the Army Corps of Engineers continue releasing massive solicitations.

Physical infrastructure demands specialized tradespeople to execute complex blueprints. The Energy Information Administration reported developers planned to add 62.8 gigawatts of new power capacity in 2024, a 55% increase over 2023 [10]. Solar installations alone accounted for 58% of this new capacity [10]. Nearly half of surveyed construction firms reported zero supply-chain issues in 2024, a stark improvement from 9% in 2023 [8]. With materials arriving on time, labor availability becomes the sole bottleneck determining project timelines.

Builders cannot bid on these federal contracts without guaranteeing resource availability. Surety bond underwriters require proof of execution capability before issuing performance bonds. The Surety & Fidelity Association of America reported a loss ratio of 24.5% in late 2024, indicating slight upward pressure on claims [11]. Underwriters penalize contractors who take on projects without adequate personnel forecasting. Implementing workforce forecasting tools in construction allows estimators to prove personnel availability to bonding companies. General contractors conduct prequalification assessments before finalizing bids to mitigate subcontractor default risk.

Software companies measure their operational health using a strict mathematical benchmark. The Rule of 40 states that a software company's revenue growth rate plus its profit margin should equal or exceed 40% [12]. McKinsey research demonstrates that only 16% of software companies consistently exceed this threshold [13]. Top-quartile companies generate nearly three times the valuation multiples of those in the bottom tier [13]. The math is unforgiving.

Founders historically prioritized raw revenue expansion over profitability. Market conditions now punish inefficient scaling. A company growing revenue at 20% year-over-year must maintain a 20% EBITDA margin to hit the benchmark. When growth drops from 25% to 15%, boards mandate immediate cost reductions to maintain the ratio [14]. Layoffs occur when executives fail to map engineering capacity against product delivery timelines. Adopting software industry capacity tracking protects strategic initiatives. Managers visualize exactly how engineering hours translate to feature releases and recurring revenue.

Resource allocation platforms measure the exact cost of client onboarding. If an implementation specialist spends 40 hours configuring an account, the software calculates the drag on gross margins. Support teams log their service tickets against specific client accounts. If a large customer demands excessive support hours, the software flags the account as unprofitable. Leaders adjust pricing structures or automate onboarding steps based on these capacity reports.

Investment timelines require rapid margin expansion. Private equity buyers routinely implement resource planning systems within the first 100 days of acquiring a service business. A 5 to 8 percentage point improvement in EBITDA margin often follows capacity optimization initiatives [15]. Financial sponsors apply these exact tactics across consumer goods, manufacturing, and professional services portfolios.

Operating partners abandon legacy accounting systems that lack profitability metrics. General platforms report financial data at the company level, obscuring the actual cost of individual client engagements. Professional services firms using basic tools lose an average of 18% in gross margin annually due to invisible project overruns [16]. Dedicated resource deployment systems designed for financial sponsors capture billable time and calculate engagement margins instantly.

Call centers highlight the financial impact of capacity mapping. McKinsey observed a consumer business that staggered shift times over a two-hour window. This simple alignment raised service adherence to 90% and increased agent occupancy from 60% to 80% [17]. The company subsequently transferred 10% of its frontline staff to other critical duties. Directors enforce these exact scheduling optimizations to maximize the valuation multiple prior to an exit.

Work management platforms absorb scheduling capabilities to increase contract values. Asana reported $723.9 million in annual revenue for fiscal 2025, marking an 11% increase over the previous year [18]. The company achieved positive cash flow and reduced its operating loss to 6% of revenues [18]. During its earnings calls, Asana highlighted the introduction of native resource management features to drive seat growth and offset expansion pressure [19]. Buyers demand clarity.

Smartsheet mirrored this expansion strategy. The company crossed $1.03 billion in recurring revenue in Q4 2024, serving more than 14.3 million users [20]. Smartsheet recently released resource management tools to the broader market via a self-service motion, removing the need for customers to consult a sales representative prior to activation [20]. Enterprise customers adopt these software modules to consolidate their technology stacks. A media organization recently moved 14,000 projects into Smartsheet, pushing its contract value past $4 million while retiring several redundant applications [21].

ServiceNow approaches the market from the IT service management angle. The vendor integrated autonomous agents into its Strategic Portfolio Management platform to convert traditional project offices into value hubs [22]. Oracle, Atlassian, and Microsoft employ similar bundling strategies. Platform consolidation links daily task execution directly to high-level financial planning.

Job titles constrain resource allocation. Organizations abandon static titles in favor of skill taxonomies. Software vendors label this transition the skills-based model. Only 8% of organizations possess reliable data on their workforce, and 50% of HR leaders admit their companies fail to apply internal capabilities effectively [23]. Capacity software addresses this gap by cataloging thousands of individual competencies. It matches these competencies against specific project requirements. Data proves the value.

Contact centers pioneered routing algorithms to handle scale. Modern platforms allow supervisors to assign proficiency scores to individual agents across technical disciplines. The software intercepts an incoming customer request. It analyzes the required expertise and routes the ticket to the agent with the matching skill profile [24]. This precise allocation prevents employee exhaustion. It also reduces the number of times a customer requires a transfer.

Talent marketplaces bring this exact routing logic to the enterprise. Platforms like DevSkiller TalentBoost and SAP SuccessFactors Career and Talent Development ingest employee profiles to suggest mobility paths [25]. When a project manager requires a data scientist for a two-week sprint, the software scans the corporate roster. It identifies a qualified analyst in a different department with low current utilization. It then brokers the temporary assignment. This internal mobility reduces external hiring costs.

Artificial intelligence alters the execution of scheduling and workforce allocation. Gartner surveys indicate 82% of human resources leaders plan to deploy agentic AI by May 2026 [26]. Analysts project that autonomous agents will perform 50% of HR activities by 2030 [26]. Unlike early models that merely suggested schedule changes, these new agents execute decisions autonomously. They operate based on defined business rules.

Vendor consolidation accelerates this transition across all segments. Workday acquired Paradox for $1 billion in October 2025 [27]. This acquisition embeds scheduling logic directly into its core platform. Amazon launched Connect Talent in April 2026, enabling AI agents to conduct voice interviews and score candidates continuously [27]. Human capital systems no longer wait for manual inputs. They detect a project delay instantly. They identify an available engineer with the correct certification and reassign the task without manager intervention. The speed is unprecedented.

Corporate governance frameworks struggle to keep pace with algorithmic speed. Current software generates machine learning embeddings to match skills against project requirements. If an agentic system relies on flawed historical data, it propagates biased patterns. The European Union Artificial Intelligence Act requires human oversight of automated decisions [27]. New York City implemented Law 144 to force audits on employment algorithms [27]. Resource managers must audit capacity plans to ensure legal compliance and maintain workforce morale.

The resource management software sector moves rapidly toward automated execution. Vendors will continue to merge separate project tracking applications and financial ledgers into unified databases. Artificial intelligence agents will assume responsibility for daily scheduling adjustments, freeing human managers to focus on strategic initiatives. Organizations that fail to adopt these platforms will suffer lower margins and higher turnover.

Regulatory pressure will shape software development over the next five years. Governments demand transparency in how algorithms evaluate employee performance and assign work. Software providers must build audit trails into their scheduling engines to prove their routing logic does not discriminate against protected classes. Buyers will penalize vendors that obscure their mathematical criteria.

Efficiency defines the modern enterprise. Tracking software suites provide the only verifiable method for measuring worker output against operational costs. As labor expenses rise across staffing, construction, software, and private equity sectors, capacity planning tools shift from optional upgrades to mandatory infrastructure.

In 2026, the resource and capacity planning software market witnessed a pivotal turning point as dedicated management platforms finally overtook manual spreadsheets in adoption rates. Alongside this shift, the integration of artificial intelligence within these tools saw significant growth, with active utilization jumping over the last 12 months. This data is particularly insightful because it hig

| Year | Dedicated Software (%) | Spreadsheets (%) |

|---|---|---|

| 2025 | 44 | 54 |

| 2026 | 54 | 44 |

The data illustrates a historic crossover point in the resource and capacity planning software market occurring over the last 12 months. For the first time, the usage of dedicated resource management platforms (54%) has surpassed reliance on manual spreadsheets (44%), while active AI utilization within these tools grew from 11% to 17% between 2025 and 2026 [source].

On a micro level, this means that individual resource managers are spending less time reconciling conflicting data and more time acting on strategic insights. At the macro industry level, this transition indicates that professional services and IT firms are finally prioritizing unified delivery lifecycles, integrating capacity planning with financial management to protect project margins [source]. The shift also signifies that the capacity planning software market—projected to reach $6.47 billion by 2030—is maturing from basic scheduling into dynamic, execution-aware forecasting [source]. Furthermore, the rapidly rising consideration of AI functionalities suggests that the next competitive frontier will be predictive resource allocation, allowing businesses to make intelligent, autonomous capacity adjustments [source].

This technological evolution is critical because poor resource allocation continues to be a primary driver of project failure and eroded profit margins. With average industry utilization sitting at roughly 72%—well below the optimal 80% benchmark required for sustainable profitability—firms can no longer afford the critical blind spots inherent in spreadsheet planning [source]. Upgrading to dedicated capacity planning software prevents the over-provisioning of expensive cloud infrastructure and reduces unbudgeted last-minute hiring, directly translating into protected bottom lines and healthier work environments [source].

Several converging pressures have likely catalyzed this rapid abandonment of spreadsheets in favor of sophisticated capacity planning solutions. The increasing complexity of hybrid cloud environments, paired with remote, globally dispersed workforces, has simply outgrown the limited, two-dimensional capabilities of legacy manual tracking [source]. Additionally, strict mandates pushing for higher billable utilization rates and tighter cost controls have forced leadership to demand real-time visibility that spreadsheets inherently cannot provide [source]. It is also highly plausible that the recent democratization of machine learning features within these software suites has dramatically increased their perceived return on investment, making the switch an operational necessity rather than a luxury.

The resource and capacity planning category is currently experiencing a fundamental technological renaissance, shedding outdated manual constraints in favor of AI-augmented, predictive software. Organizations that fail to adopt these dedicated platforms risk severe competitive disadvantages, which are often characterized by persistent bench time, employee burnout, and chronic project delays. The most prominent takeaway is clear: in an era of tightening budgets and complex project demands, treating capacity planning as a manual administrative task is a recipe for failure, whereas leveraging dedicated, AI-driven software is the new baseline for organizational profitability.