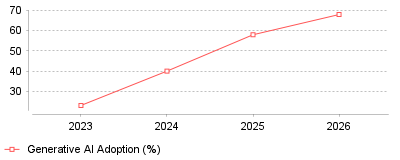

The data reveals a dramatic acceleration in artificial intelligence adoption within the small business and accounting software sectors over the last three years. Specifically, it highlights how generative AI usage among small businesses has surged from 23% in 2023 to 68% in 2026, alongside a parallel spike in accountants using AI daily. This trend is highly interesting because it signals a definit

| Year | Generative AI Adoption (%) |

|---|---|

| 2023 | 23 |

| 2024 | 40 |

| 2025 | 58 |

| 2026 | 68 |

This trend illustrates a massive, rapid integration of artificial intelligence into the daily financial and operational workflows of small and medium-sized businesses. Between 2023 and 2026, general AI adoption among small businesses nearly tripled, while daily usage of AI tools by accounting professionals skyrocketed from 18 percent to nearly 50 percent [source].

On a micro level, this means that individual accounting practices and small businesses are spending significantly less time on manual data entry, bank reconciliation, and routine bookkeeping. Tools equipped with generative and agentic AI are now automating up to 80 percent of these traditional, time-consuming tasks [source]. On a macro industry level, the accounting software market is undergoing a structural paradigm shift from basic cloud storage to proactive financial intelligence [source]. Consequently, the traditional gap in technology adoption between large enterprises and micro-businesses is closing at an unprecedented rate, dropping from a 1.8x difference to nearly parity in just a few years [source].

This rapid evolution is important because it changes the fundamental value proposition of accounting professionals and the software platforms they utilize. Instead of billing clients for routine compliance work, accountants are leveraging AI-driven time savings to offer high-value strategic advisory services [source]. Furthermore, it empowers small businesses to achieve enterprise-grade financial forecasting, fraud detection, and cash flow management without needing to hire extensive in-house finance teams [source].

The primary catalyst for this surge is the democratization and cost-reduction of generative AI capabilities, largely driven by native integrations into already familiar platforms like QuickBooks and Xero [source]. Additionally, the accounting industry is facing a severe talent shortage, with a projected deficit of 340,000 certified public accountants by 2030, forcing firms to adopt automation out of sheer necessity [source]. It is also highly likely that post-pandemic remote work normalized cloud accounting, laying the perfect digital foundation for AI tools to ingest and analyze financial data seamlessly. Finally, the introduction of autonomous agentic AI—which can plan and execute multi-step workflows rather than just answering text prompts—has moved the technology from a novelty to a measurable driver of return on investment [source].

The trajectory of small business accounting software is unmistakably heading toward autonomous, AI-driven financial management. As adoption rates continue to climb past 68 percent in 2026, businesses that fail to integrate these tools risk severe competitive disadvantages in both efficiency and strategic insight. Ultimately, the prominent takeaway is that AI in accounting is no longer an experimental feature; it is a mandatory core operational layer that separates growing businesses from stagnant ones.

Intuit generated $16.3 billion in revenue during its fiscal year ending July 31, 2024. [1] The company recorded 19% growth within its small business division. Operating revenue for Xero rose 22% to NZ$1.71 billion during the same period. [2] These specific metrics illustrate a sector actively forcing paper ledgers into digital databases. The bookkeeping tools for small operators must process transaction workflows under intense regulatory scrutiny.

Market Research Future projects the software sector will reach $42.29 billion by 2035. [3] Buyers no longer treat bookkeeping tools as optional overhead. Finance managers treat these applications as critical operational infrastructure. North America represents the largest revenue geography due to high cloud adoption rates. The Asia-Pacific region functions as the fastest-growing market territory. [3]

Vendors charge higher subscription fees to fund specialized feature developments. Average revenue per user for Xero expanded by 14% to NZ$39.29 in 2024. [2] Xero removed 160,000 idle subscriptions during its 2025 half-year reporting period. [4] This exact database purge allowed the company to focus server capacity on active users. Product executives design financial management platforms to lock business owners into long-term retention cycles.

Intuit specifically rebranded its division to the Global Business Solutions Group. [5] This name change reflects a strategy targeting mid-market clients. Companies moving away from basic ledger entry require applications that automatically categorize expense streams. Macroeconomic pressures accelerate this transition. Average real monthly revenue for US small businesses was $51,700 in September 2024, representing a 0.58% decrease. [6] Tighter operating margins force companies to monitor their cash reserves continuously.

Human capital shortages dictate software engineering priorities. The United States lost 340,000 accountants between 2019 and 2024. [7]

Firms cannot hire enough staff to close monthly books manually. The American Institute of Certified Public Accountants tracked a 22.5% drop in CPA candidates from 2017 to 2024. [7] Demographic data shows 75% of active professionals are approaching retirement age. [8] Total university accounting graduates decreased 20% since 2010. [8]

Corporate controllers compensate for empty desks by purchasing software. Automation transitions from a luxury feature to a survival mechanism. Operations teams report severe compliance errors when overworked staff rush data entry tasks. UK accounting practices report saving 19 hours per week using artificial intelligence workflows. [9] The global market for these specialized AI tools will reach $37.6 billion by 2030. [9]

Sage introduced an AI-powered Close Assistant to its Intacct platform. The vendor claims this tool shortens financial close cycles by 70%. [10] Algorithms detect duplicate invoice entries before they post to the general ledger. Machine learning models actively replace data clerks. Approximately 25% of CPA firms currently outsource at least part of their bookkeeping work to offshore providers to bridge this talent gap. [11] Automated systems offer a cheaper alternative to overseas labor contracts.

The European Union approved the VAT in the Digital Age directive on November 5, 2024. [12]

This legislation permanently alters international billing mechanics. All member states must enforce electronic invoicing for cross-border transactions by July 2030. [13] Standard PDF invoices will lose their legal validity. Software providers must update their codebases to output machine-readable formats that comply with the EN 16931 technical standard. [14] The Dutch Ministry of Finance recommended mandatory use of the Peppol network for interoperability. [13]

Compliance requires major architectural overhauls for North American software vendors. The directive mandates transaction data transmission to national tax authorities within 10 days of a chargeable event. [15] Near-real-time reporting prevents carousel tax fraud. It also creates extreme server load requirements. Batch processing at the end of the month violates the new legal frameworks.

Spain and France already maintain strict domestic billing timelines. France requires mid-sized enterprises to issue compliant digital invoices by September 2026. [16] Software that fails to generate certified tamper-proof records will render business clients non-compliant. Non-compliant platforms face fines of €15 per incorrect invoice in France. [16]

Vendors must build specific integrations with national tax portals. This technical burden forces market consolidation. Smaller software developers lack the engineering budgets to maintain compliance across 27 distinct regulatory environments. The Single VAT Registration pillar allows businesses to register for VAT in a single member state to manage multi-jurisdiction compliance. [17] Platforms facilitating passenger transport or short-term accommodation must collect VAT if the underlying provider does not. [15]

Generic databases fail when applied to specialized industries.

A standard chart of accounts works perfectly for a freelance designer. However, tracking project costs for builders requires complex job costing. Construction firms must calculate percentage-of-completion revenue recognition. They track union labor rates and material price fluctuations. These specific inputs break basic expense templates.

Retail environments face distinct operational hurdles. Store managers syncing daily register receipts need software that handles thousands of micro-transactions. High-frequency data transfers often trigger API rate limits. Food and beverage operators encounter identical constraints. Systems monitoring perishable inventory expenses must integrate seamlessly with terminal hardware. Restaurant margins depend on daily ingredient cost calculations rather than monthly summaries.

Non-governmental organizations operate under restrictive funding rules. Platforms featuring managing restricted grant funds must separate specific revenue streams from general operating assets. Comingling these assets violates strict compliance standards. Auditors penalize charities that fail to trace grant dollars to specific program expenses.

Digital service providers navigate entirely different structural challenges. Firms handling deferred revenue schedules deal with delayed cash recognition. They collect annual cash payments upfront but must recognize the revenue incrementally over twelve months. Traditional cash-basis software cannot process these accrual schedules without manual intervention. Professional firms billing hourly rates require distinct time-tracking modules. The billing for legal retainers must link individual timesheets directly to specific client ledger codes. Independent contractors need flexible invoicing for independent consultants that handle irregular payment milestones.

SoftLedger built its architecture on an API-first framework. [18]

Most legacy accounting systems treat external connections as secondary features. Finance teams struggle to extract raw data from isolated software silos. Connecting external customer management tools to a general ledger frequently causes synchronization failures. Traditional products rely on batch processing, while modern sales tools expect real-time data flow.

Intuit QuickBooks Online limits API calls to 500 requests per minute per realm ID. [19] Exceeding this traffic threshold causes immediate data sync rejections. Xero imposes stricter limits, restricting API traffic to 60 calls per minute and 5,000 calls daily. [19] A busy retail operator processing weekend sales volume will hit these thresholds rapidly. When the server rejects the payload, financial controllers must spend hours mapping missing transactions manually.

Developers must build offset pagination scripts to prevent data loss during transmission. [19] The software industry lacks a universal schema for financial records. Differing field definitions cause mapping errors when two platforms attempt to communicate. A field labeled "Total Price" in a sales application might import as "Subtotal" in the accounting ledger. These mapping failures corrupt final financial statements.

The ACH network processed 35.2 billion payments in 2025. [20]

Paper checks now account for only 25% of commercial payment volume. This figure dropped from 81% in 2004. [20] Organizations planning to eliminate check use cite manual processing inefficiency as the primary driver. [20] Modern platforms embed payment execution directly into the invoice approval screen. Users do not need to log into separate banking portals to authorize vendor disbursements.

Sage integrated Vendor Payments into its Intacct platform to route ACH transfers natively. [21] Fyle incorporated direct ACH reimbursements into its expense management module, allowing one-click deposits to employee bank accounts. [22] This architectural shift reduces processing costs. It also eliminates manual reconciliation tasks because the software marks the invoice as paid the exact moment the digital transfer initiates.

Automated receivables management accelerates cash inflows. Software models calculate the probability of late payments based on historical client behavior. A customer displaying a 70% risk of delayed settlement triggers an automated payment reminder. [23] Firms using these automated invoice sequences report a 20% to 40% reduction in overdue balance values. [23] Integrating payment rails directly into the general ledger creates a closed-loop system.

Bookkeeping processes merge directly with financial planning. The global market for specialized small business software will hit $10.15 billion by 2032. [24]

Data entry tasks no longer require human operators. Optical character recognition extracts line items from vendor receipts instantly. Cloud adoption reached 54% among US companies for basic finance operations in 2025. [25] The financial planning software market ranged from $4.3 to $5.1 billion in 2023, with AI segments showing a 34% compound annual growth rate. [24]

Software engineering now focuses on predictive modeling. Algorithms analyze historical payroll runs, upcoming rent liabilities, and average invoice settlement times to project bank balances. Vendors that fail to provide these predictive tools will lose market share rapidly. Businesses demand actionable intelligence rather than historical reports. The integration of capital forecasting into daily ledger management represents the next mandatory product feature.

Firms refusing to adopt cloud infrastructure will face higher labor costs and severe compliance penalties in markets mandating digital reporting. The separation between historical accounting and future financial planning will disappear entirely over the next five years.

The data reveals a dramatic acceleration in artificial intelligence adoption within the small business and accounting software sectors over the last three years. Specifically, it highlights how generative AI usage among small businesses has surged from 23% in 2023 to 68% in 2026, alongside a parallel spike in accountants using AI daily. This trend is highly interesting because it signals a definit

| Year | Generative AI Adoption (%) |

|---|---|

| 2023 | 23 |

| 2024 | 40 |

| 2025 | 58 |

| 2026 | 68 |

This trend illustrates a massive, rapid integration of artificial intelligence into the daily financial and operational workflows of small and medium-sized businesses. Between 2023 and 2026, general AI adoption among small businesses nearly tripled, while daily usage of AI tools by accounting professionals skyrocketed from 18 percent to nearly 50 percent [source].

On a micro level, this means that individual accounting practices and small businesses are spending significantly less time on manual data entry, bank reconciliation, and routine bookkeeping. Tools equipped with generative and agentic AI are now automating up to 80 percent of these traditional, time-consuming tasks [source]. On a macro industry level, the accounting software market is undergoing a structural paradigm shift from basic cloud storage to proactive financial intelligence [source]. Consequently, the traditional gap in technology adoption between large enterprises and micro-businesses is closing at an unprecedented rate, dropping from a 1.8x difference to nearly parity in just a few years [source].

This rapid evolution is important because it changes the fundamental value proposition of accounting professionals and the software platforms they utilize. Instead of billing clients for routine compliance work, accountants are leveraging AI-driven time savings to offer high-value strategic advisory services [source]. Furthermore, it empowers small businesses to achieve enterprise-grade financial forecasting, fraud detection, and cash flow management without needing to hire extensive in-house finance teams [source].

The primary catalyst for this surge is the democratization and cost-reduction of generative AI capabilities, largely driven by native integrations into already familiar platforms like QuickBooks and Xero [source]. Additionally, the accounting industry is facing a severe talent shortage, with a projected deficit of 340,000 certified public accountants by 2030, forcing firms to adopt automation out of sheer necessity [source]. It is also highly likely that post-pandemic remote work normalized cloud accounting, laying the perfect digital foundation for AI tools to ingest and analyze financial data seamlessly. Finally, the introduction of autonomous agentic AI—which can plan and execute multi-step workflows rather than just answering text prompts—has moved the technology from a novelty to a measurable driver of return on investment [source].

The trajectory of small business accounting software is unmistakably heading toward autonomous, AI-driven financial management. As adoption rates continue to climb past 68 percent in 2026, businesses that fail to integrate these tools risk severe competitive disadvantages in both efficiency and strategic insight. Ultimately, the prominent takeaway is that AI in accounting is no longer an experimental feature; it is a mandatory core operational layer that separates growing businesses from stagnant ones.