| Year | Cloud WMS (%) | On-Premise WMS (%) |

|---|---|---|

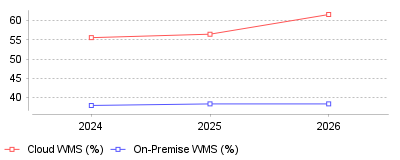

| 2024 | 55.6 | 38 |

| 2025 | 56.5 | 38.4 |

| 2026 | 61.6 | 38.4 |

This trend illustrates a continuous, year-over-year expansion in the adoption of cloud-based Warehouse Management Systems (WMS) and Third-Party Logistics (3PL) software, rapidly displacing traditional on-premise infrastructure [source]. By 2026, cloud deployments are projected to secure over 61% of the global market share, solidifying software-as-a-service (SaaS) as the dominant deployment model in the global logistics sector [source].

On a micro level, individual warehouses and 3PL providers are shifting from a capital expenditure model, which requires heavy upfront investments in hardware and software licenses, to a highly flexible operational expenditure approach [source]. This shift allows smaller and mid-sized businesses to leverage enterprise-grade logistics tools without prohibitive costs, democratizing access to advanced automated features and real-time analytics [source]. On a macro level, the global supply chain is becoming vastly more interconnected and agile, breaking down rigid data silos that previously hindered cross-border and multi-location fulfillment operations [source]. Furthermore, this transition means vendors are focusing their resources more heavily on delivering continuous software updates, embedding artificial intelligence, and offering robust API integrations to maintain their competitive edge in a crowded market [source].

As consumer expectations for ultra-fast, omnichannel delivery continue to rise, legacy on-premise systems frequently struggle to provide the necessary flexibility and real-time visibility [source]. Cloud-based WMS solutions empower retailers and 3PLs to scale their operations rapidly during seasonal demand peaks, seamlessly synchronize inventory across multiple geographic nodes, and quickly deploy robotic automation [source]. Ultimately, this technological shift protects profit margins by significantly reducing IT maintenance overhead, improving overall order picking accuracy, and drastically accelerating the time-to-value for newly established fulfillment centers [source].

The foundational catalyst for this trend was the explosive growth of e-commerce, which exponentially increased the volume and complexity of warehouse workflows over recent years [source]. Additionally, persistent global labor shortages in the logistics sector have forced operators to adopt robotics and AI-driven predictive analytics, features that are most efficiently deployed, integrated, and updated via cloud environments [source]. There is also reason to speculate that the normalization of remote work and the necessity for off-site management during recent global supply chain disruptions highlighted the fatal inflexibility of localized, on-premise servers [source]. Finally, the rise of affordable, highly secure cloud infrastructure from major tech conglomerates has alleviated historical concerns regarding data security, removing the last major barrier to widespread industry adoption [source].

The decisive shift toward cloud-based shipping and fulfillment software marks a permanent evolution in supply chain management rather than a temporary trend. By trading rigid infrastructure for scalable, subscription-based innovation, logistics providers are equipping themselves to handle the future complexities of global e-commerce seamlessly. A prominent takeaway is that 3PLs and retailers clinging to traditional on-premise systems risk falling permanently behind in both operational efficiency and customer satisfaction, as the industry standard now demands the agility that only cloud environments can provide.

Global software investments reflect shifting corporate priorities as physical distribution networks digitize. Gartner projects that supply chain management software featuring automated agents will expand from under $2 billion in 2025 to $53 billion by 2030 [1]. Transportation management system deployments drive a significant portion of this growth. Global Market Insights values the total transportation management software market at $15 billion in 2025. Analysts forecast expansion to $40.3 billion by 2035 [2].

Regional data supports this aggressive growth trajectory. The North American supply chain management software market reached $7.17 billion in 2024. Projections show this regional segment growing to $16.9 billion by 2033 [3]. Retail operations account for 33.8% of this market share. Cloud applications dominate deployment models, capturing 56.3% of the total market volume. Corporate executives treat software tools for retail commerce as critical infrastructure. Automated systems prevent margin erosion during freight pricing fluctuations.

Consequently, spending on platforms that handle logistics and order fulfillment continues to outpace general enterprise software categories. Dataintelo values the global transportation and logistics software market at $23.4 billion in 2025 [4]. Researchers anticipate a 10.8% compound annual growth rate through 2034. The solutions segment accounted for 67% of the transportation management system market in 2025. Oracle led the vendor pack with over 19% market share, while competitors including SAP and WiseTech Global fight for the remaining enterprise installations.

The United States warehousing sector faces severe workforce limitations. The Bureau of Labor Statistics reported 1.86 million workers employed in the warehousing and storage industry in 2024 [5]. When including hand laborers and material movers, that figure reaches 7 million workers [6]. The broader transportation sector employs 6.6 million workers, accounting for 5% of all private-sector jobs. Median wages for logisticians reached $80,880 in May 2024 [7].

Companies cannot hire their way out of volume spikes. E-commerce transaction volume forces facilities to process more units with fewer personnel. Bureau of Labor Statistics projections show warehousing employment growth slowing to 1.41% over the next decade [8]. Firms must replace human labor with automated machinery. The transportation sector added 198,800 new jobs between 2024 and 2034, making it the seventh-largest growth sector in the national economy. A McKinsey study shows that almost 70% of warehouse operators in the Asia-Pacific region experienced trouble hiring and retaining workers in 2024 [9].

This labor shortage dictates software purchasing decisions. When evaluating logistics software suitable for direct-to-consumer brands, operations directors prioritize features that minimize physical movement. Slotting algorithms reduce picker transit time by predicting ideal inventory placement. Software must orchestrate automated vehicles alongside human pickers. International Data Corporation predicts that 40% of major global companies will implement robotics to improve order fulfillment speed by 2025 [10]. These deployments aim to increase pick speed by 10% and reduce errors by up to 2%. System architecture lacking interfaces for hardware integration faces immediate obsolescence.

Flexport acquired the logistics assets of Shopify, including Deliverr, in 2023. This transaction exchanged physical fulfillment assets for a 13% equity interest in Flexport [11]. Shopify previously invested $260 million into Flexport to solidify this partnership [12]. The deal transforms Flexport from a pure freight forwarder into an end-to-end fulfillment provider. Flexport previously reached an $8 billion valuation after raising $935 million in a funding round led by Shopify and SoftBank [13].

Operational changes ripple through the merchant base. Starting June 2025, Shopify alters its routing logic for external fulfillment applications. Unassigned order lines default to zero fulfillable quantity if not explicitly mapped to approved locations [14]. This protocol forces merchants to overhaul their inventory routing settings. Third-party logistics providers must update their application integrations to prevent order failures.

System architecture changes create friction for smaller merchants. Implementing routing systems for online sellers requires technical resources that independent operators lack. Flexport responded to integration hesitations by offering financial incentives. The company offered 10% discounts on shipping fees to merchants upgrading to specific expedited service tiers [15]. The expedited service enables shipping in three days or less on 70% of network shipments. This compares to 25% for standard service levels. Sendcloud research indicates 64.3% of shoppers in the United Kingdom refuse to reorder following a failed delivery [16].

Manhattan Associates reported $270.4 million in revenue for the fourth quarter of 2025 [17]. Cloud subscription revenue reached $108.6 million during this period. License revenue fell to just $2.6 million. Full-year 2025 revenue hit $1.08 billion. Adjusted operating income was $91.4 million for the quarter. Management noted a 20% year-over-year increase in cloud revenue, demonstrating market preference for hosted software instances [18].

Descartes Systems Group announced $187.7 million in revenue for its fiscal 2026 third quarter [19]. This represents an 11% year-over-year increase. Descartes maintains its growth through aggressive acquisition strategies. The company purchased inventory provider Finale Inc. for $39.2 million in August 2025. Earlier in the year, Descartes acquired 3GTMS for $112.7 million to expand its domestic transportation capabilities [20]. Services revenues account for 93% of total revenue.

C.H. Robinson posted $16.2 billion in total revenues for 2025. This marked an 8.4% decrease from the previous year. Divestiture of its European surface transportation division and lower ocean pricing drove this decline [21]. Despite revenue drops, the company increased its 2026 operating income target to $1.04 billion. Executives cited $336 million in anticipated savings from artificial intelligence implementation [22]. First quarter 2026 net income totaled $147.2 million [23]. Software vendors target distinct buyer profiles. Tools marketed as fulfillment solutions for physical shop owners emphasize store-level pickup protocols. Enterprise systems focus instead on multimodal freight orchestration.

Artificial intelligence integration causes severe workplace friction. A February 2025 Gartner survey of 265 supply chain respondents found that 72% of organizations deployed artificial intelligence tools [24]. These deployments yield middling financial results. Productivity gains remain isolated to desk-based workers. Frontline warehouse personnel experience increased anxiety from new software requirements.

Chief supply chain officers focus excessively on short-term returns. A June 2025 survey showed only 23% of supply chain leaders maintain a formal artificial intelligence strategy [25]. Leaders measure success through bottom-line metrics rather than revenue generation. They view text models as cost-saving tools rather than operational differentiators. This approach risks creating fragile technical infrastructure. Implementing isolated scripts rather than cohesive data models prevents scaling.

International Data Corporation projects that 55% of major manufacturers will redesign service supply chains around predictive models by 2026 [26]. Success depends on data integration capabilities rather than algorithm selection. McKinsey research shows artificial intelligence implementation mitigates forecasting errors by up to 50% [27]. Technology leaders must transition from efficiency mandates to capability expansion. Gartner analysts note that organizations must shift toward use-cases promoting creativity. Relying solely on automation to cut headcount creates brittle operations. When artificial intelligence directs warehouse pickers without context, employee morale plummets.

Corporate supply chains remain critically blind past their primary suppliers. McKinsey's 2025 survey of 100 supply chain leaders revealed that awareness of tier-two risks declined throughout 2023 and 2024 [28]. Companies compensate for poor visibility by holding excess inventory. This tactic consumes working capital and diverts funds from facility upgrades. Dual sourcing and increased inventory levels serve as primary defense mechanisms for 97% of surveyed companies [29].

Risk management software attempts to solve this visibility gap. The supply chain risk management market reached $5.12 billion in 2025 [30]. Cloud-hosted platforms capture 72.4% of this revenue due to their ability to process external data streams. Software buyers select cloud infrastructure primarily to accelerate installation timelines. Cybersecurity represents the fastest-growing risk domain. A supplier breach provides attackers with direct entry into buyer networks. This segment expands at a 14.1% compound annual growth rate.

Global volatility forces network redesigns. Only 6% of businesses achieved full supply chain visibility according to Geodis survey data [31]. Data remains siloed across partner networks. Application programming interfaces must bridge these disparate systems. A unified data schema prevents shipping delays when regional ports close. Digital twin capabilities allow planners to simulate disruptions before they occur.

Third-party logistics providers lose contracts due to software installation delays. Traditional warehouse management systems require six months to implement. This timeline prevents logistics companies from accepting immediate contract opportunities. Speed defines competitive advantage in the outsourced fulfillment sector. Logistics firms cannot defer billing while waiting for technical configurations.

Software provider Logiwa reported that reducing client onboarding from months to 15 days allows logistics providers to capture millions in previously abandoned revenue [32]. Standardized configurations eliminate custom coding delays. System architectures must support rapid tenant provisioning. Legacy software platforms require extensive professional services for basic integrations. Agencies managing promotional merchandise face similar hurdles. When selecting inventory tools for promotional campaign distribution, implementation speed ranks above feature depth. Account directors cannot wait quarters for software configuration. Campaigns launch on fixed dates regardless of warehouse readiness.

Multi-client environments demand strict data partitioning. Software must isolate inventory counts while sharing physical racking space. Billing modules calculate storage fees automatically based on daily pallet positions. Manual invoice generation destroys margins for high-volume logistics providers. E-commerce fulfillment pushes parcel and less-than-truckload complexities onto third-party warehouses. Platforms failing to automate freight auditing lose market share rapidly.

Consumer delivery expectations force retailers to push inventory closer to population centers. Large centralized distribution centers cannot support same-day delivery mandates. Micro-fulfillment centers reduce fulfillment costs by 75% compared to traditional warehouse operations [33]. These smaller facilities operate within existing retail footprints or urban zones. Space constraints in urban centers demand vertical automation. Systems utilize dense storage grids accessed by robotic shuttles.

Warehouse management software must translate incoming orders into optimal shuttle paths. Space constraints force software to prioritize volume utilization over visual accessibility. Last-mile delivery represents the most expensive segment of the supply chain. International Data Corporation anticipates that fulfillment optimization will improve last-mile profitability by 15% by 2027 [34]. Algorithms calculate delivery routes based on traffic patterns and vehicle capacity.

Inventory fragmentation complicates stock balancing. Retailers splitting 10,000 units across 50 micro-fulfillment centers face higher stockout risks than when holding identical volume in two facilities. Software must predict local demand variations using historical transaction data. Machine learning models reallocate inventory between nodes before regional shortages occur. Software integrates directly with gig-worker platforms to source delivery drivers during peak demand periods.

Environmental compliance dictates future software architecture. The European Union requires importers to calculate embedded emissions through border adjustment mechanisms. Transportation software must document fuel consumption across transit routes. Reporting shifts from marketing departments to procurement operations. Cloud platforms offer modules for reducing energy use and waste [35]. Hardware integration becomes mandatory for monitoring environmental conditions.

Gartner data indicates only 29% of supply chains possess the key strengths needed for future challenges [36]. Researchers identified agility and regionalization as critical traits. Leaders share a commitment to preparation through deliberate strategies. Non-leaders focus on short-term priorities and reactive fixes. Intelligent automation will orchestrate multi-step workflows. Gartner forecasts that 60% of enterprises using supply chain software will adopt agentic features by 2030 [37]. Current enterprise deployments lag behind software availability due to data readiness gaps. Organizations must clean their historical transaction records before training proprietary models.

The software market faces inevitable consolidation. Point solutions handling single tasks merge into unified commerce platforms. Buyers demand single interfaces for inventory tracking and freight procurement. Vendors failing to acquire complementary technologies lose market share to suite providers. Real-time data access dictates survival in modern logistics.

| Year | Cloud WMS (%) | On-Premise WMS (%) |

|---|---|---|

| 2024 | 55.6 | 38 |

| 2025 | 56.5 | 38.4 |

| 2026 | 61.6 | 38.4 |

This trend illustrates a continuous, year-over-year expansion in the adoption of cloud-based Warehouse Management Systems (WMS) and Third-Party Logistics (3PL) software, rapidly displacing traditional on-premise infrastructure [source]. By 2026, cloud deployments are projected to secure over 61% of the global market share, solidifying software-as-a-service (SaaS) as the dominant deployment model in the global logistics sector [source].

On a micro level, individual warehouses and 3PL providers are shifting from a capital expenditure model, which requires heavy upfront investments in hardware and software licenses, to a highly flexible operational expenditure approach [source]. This shift allows smaller and mid-sized businesses to leverage enterprise-grade logistics tools without prohibitive costs, democratizing access to advanced automated features and real-time analytics [source]. On a macro level, the global supply chain is becoming vastly more interconnected and agile, breaking down rigid data silos that previously hindered cross-border and multi-location fulfillment operations [source]. Furthermore, this transition means vendors are focusing their resources more heavily on delivering continuous software updates, embedding artificial intelligence, and offering robust API integrations to maintain their competitive edge in a crowded market [source].

As consumer expectations for ultra-fast, omnichannel delivery continue to rise, legacy on-premise systems frequently struggle to provide the necessary flexibility and real-time visibility [source]. Cloud-based WMS solutions empower retailers and 3PLs to scale their operations rapidly during seasonal demand peaks, seamlessly synchronize inventory across multiple geographic nodes, and quickly deploy robotic automation [source]. Ultimately, this technological shift protects profit margins by significantly reducing IT maintenance overhead, improving overall order picking accuracy, and drastically accelerating the time-to-value for newly established fulfillment centers [source].

The foundational catalyst for this trend was the explosive growth of e-commerce, which exponentially increased the volume and complexity of warehouse workflows over recent years [source]. Additionally, persistent global labor shortages in the logistics sector have forced operators to adopt robotics and AI-driven predictive analytics, features that are most efficiently deployed, integrated, and updated via cloud environments [source]. There is also reason to speculate that the normalization of remote work and the necessity for off-site management during recent global supply chain disruptions highlighted the fatal inflexibility of localized, on-premise servers [source]. Finally, the rise of affordable, highly secure cloud infrastructure from major tech conglomerates has alleviated historical concerns regarding data security, removing the last major barrier to widespread industry adoption [source].

The decisive shift toward cloud-based shipping and fulfillment software marks a permanent evolution in supply chain management rather than a temporary trend. By trading rigid infrastructure for scalable, subscription-based innovation, logistics providers are equipping themselves to handle the future complexities of global e-commerce seamlessly. A prominent takeaway is that 3PLs and retailers clinging to traditional on-premise systems risk falling permanently behind in both operational efficiency and customer satisfaction, as the industry standard now demands the agility that only cloud environments can provide.