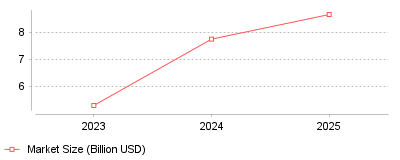

| Year | Market Size (Billion USD) |

|---|---|

| 2023 | 5.3 |

| 2024 | 7.75 |

| 2025 | 8.66 |

The gathered data illustrates a robust acceleration in the global Project Portfolio Management (PPM) software market, scaling from 5.3 billion USD in 2023 to an estimated 8.66 billion USD by 2025 [source]. Alongside this monetary growth is a decisive shift toward cloud deployments, which captured 52.5 percent of the market in 2023 and is projected to account for over 69.4 percent of total revenue in 2025 [source].

On a micro level, this indicates that individual organizations are abandoning rigid, on-premises legacy systems and manual spreadsheet tracking in favor of agile, cloud-native platforms. Project managers are increasingly empowered by remote accessibility, real-time analytics, and seamless integrations with broader enterprise resource planning ecosystems. On a macro industry level, the PPM software category is consolidating as a mission-critical strategic function rather than a mere administrative tool. Enterprise tech budgets are prioritizing these systems to ensure multi-regional alignment, mitigate complex risks, and drive return on investment across massive digital transformation initiatives.

This trend is vital because it redefines how large-scale enterprise capital is allocated and monitored across thousands of simultaneous initiatives. Cloud-based PPM software serves as the foundational infrastructure for emerging artificial intelligence capabilities, with recent surveys indicating that 45 percent of project professionals are already using AI tools in their workflows [source]. Without scalable cloud architecture, businesses cannot leverage the generative AI and predictive analytics required to automate resource allocation, flag portfolio anomalies, and maintain a competitive edge.

A primary catalyst for this shift is the lasting impact of remote and hybrid work models, which fundamentally broke traditional, siloed project management approaches. Furthermore, the sheer complexity and speed of modern digital transformation efforts make it impossible for human analysts to manually spot resource bottlenecks or strategic misalignment in real-time. We can also speculate that the sudden mainstream accessibility of generative AI and machine learning algorithms created an urgent mandate for companies to migrate to the cloud, as on-premises systems generally lack the elastic compute power required for these advanced AI features. Consequently, software vendors have heavily incentivized software-as-a-service subscriptions over perpetual licenses, effectively accelerating the cloud adoption curve across all geographic regions.

The trajectory of the PPM software category proves that effective project execution is now inextricably linked to cloud agility and AI-driven insights. As organizations continue to face intense macroeconomic pressures, they will increasingly rely on these dynamic platforms to prioritize high-value work and automate routine governance. Ultimately, the prominent takeaway is that strategic portfolio management has moved from a back-office reporting function to a centralized, predictive engine that dictates overall corporate success.

During the fourth quarter of fiscal 2024, Smartsheet crossed $1 billion in annualized recurring revenue [1]. Total revenue for the company reached $286.9 million by October 2024, reflecting a 17% increase year over year [2]. Gross profit hit $233.1 million, maintaining an 81% gross margin [2]. These financial benchmarks signal maturity across the broader project management and productivity tools sector. Software vendors continue to post strong growth despite difficult macroeconomic conditions. Procore generated $1.15 billion in 2024 revenue, representing a 21% annual growth rate [3].

The global market for portfolio tracking software reached $5.3 billion in 2023 [4]. Analysts project total market spend will hit $10.2 billion by 2032, advancing at a 7.3% compound annual growth rate [4]. North America accounts for 37% of this global revenue [5]. Large enterprises make up 25% of the total user base [4]. Gartner data shows typical enterprise IT departments operate 150 to 300 concurrent technology projects [6]. Budgets for these concurrent initiatives range from $100 million to $500 million [6].

This scale creates severe administrative pressure. Eighty-two percent of companies exceeding $1 billion in revenue plan to adopt strategic planning software by 2026 [6]. Cloud deployments hold over 40% of the market share [7]. The transition from legacy on-premise systems to cloud architecture drives service revenues. MarketsandMarkets notes that consulting and implementation services capture the largest segment share during enterprise software transitions [8]. Organizations use these platforms to enforce data compliance and manage dispersed remote teams.

Sixty percent of project management offices close within three years of launch [9]. Unclear roles and misaligned priorities destroy organizational mandates. Forrester data places this failure rate even higher, tracking office closures between 50% and 75% for newly established groups [9]. One in five Australian organizations disbanded their project teams entirely between 2019 and 2021 [9]. When market conditions shift, traditional project offices fail to adapt their rigid procedural frameworks.

Without strategic alignment, technology deployments fail. Seventy percent of digital investments fail to deliver expected outcomes without strategic portfolio oversight [10]. Enterprise executives report poor returns from recent software purchases. KPMG found that 51% of technology executives saw zero profitability increases from their digital investments between 2021 and 2023 [11]. Capital is wasted on low-impact initiatives while critical deliverables miss deadlines.

Managing a portfolio requires overcoming five specific operational obstacles. Administrators struggle with limited visibility, misaligned priorities, resource bottlenecks, governance overload, and unclear metrics [11]. High-priority tasks often suffer from understaffing, while low-impact projects consume excess capital [11]. Forty-four percent of project managers identify resource shortages as their primary challenge [12]. The Resource Management Institute found that proper allocation improves success rates by 15% and reduces costs by 10% [11]. When executives delay decisions by five hours or more, agile project failure rates rise to 22% [12].

Software implementation generates measurable financial returns. Forrester Research published an economic impact report detailing these benefits. Tracking tools decrease project failure rates by 15% [13]. They reduce budget overruns by 10% and cut administrative time by 25% [13]. Despite these financial advantages, nearly half of project offices still rely on spreadsheets as their primary tracking tool [13]. Buyers evaluating portfolio and program management software must prioritize platforms that enforce governance without creating bureaucratic bottlenecks. Organizations employing modern management software complete 89% of their projects successfully [14].

Construction software digitizes physical job sites. Procore ended 2024 serving 2,333 customers generating over $100,000 in annual recurring revenue [15]. This customer segment grew 16% year over year [15]. The vendor achieved a net revenue retention rate of 106% in 2024, with 48% of its total recurring revenue coming from clients using six or more product modules [15]. The physical construction process requires strict coordination among highly specialized contracting groups [3].

Specific features address these physical constraints. Deploying management software tailored for contractors allows site supervisors to view digital plans offline. Autodesk Construction Cloud replaced physical blueprints with mobile applications that work without internet connections [16]. Wrike introduced artificial intelligence risk mitigation for infrastructure jobs in 2025 [16]. This software categorizes tasks into risk tiers based on historical data to predict delays before they disrupt budgets [16]. Orangescrum provides an open-source alternative featuring Kanban and Gantt views for timeline planning [16].

Margin expansion remains a priority across the construction software sector. Procore achieved a 9% operating margin in the third quarter of 2024 [17]. Following this performance, management initiated a $300 million stock repurchase program to deploy excess capital [17]. The company expanded its regional data storage options into the United Kingdom and Australia to meet strict regulatory compliance requirements [17]. Tracking physical materials and earthworks reduces total carbon emissions during property development [18].

Financial analysts spend up to 60% of their working hours transcribing data from PDFs into formal systems [19]. Despite purchasing expensive accounting ledgers, private equity firms maintain their primary operational records in spreadsheets. Capital call notices and quarterly tax forms arrive in unstructured formats. This workflow creates a severe ingestion gap between raw data delivery and portfolio analysis [19].

Alternative asset operations cost five to ten times more than public market operations [20]. Pension funds in Europe pay 2.7% of their total assets annually in management costs [20]. BlackRock acquired eFront in 2019 to handle these complex fund structures [19]. Competitors like Allvue and Addepar fight for market share among mid-sized investment firms [19]. Implementing oversight systems built for private equity firms requires distinct capital allocation features. Limited partners demand extreme look-through transparency. Investors expect exposure data on specific underlying companies rather than surface fund metrics [19].

Automation tools reclaim 80% of staff hours lost to document handling [20]. Companies deploy artificial intelligence software to read scanned tax forms and unstructured emails. Platforms like V7 Go act as an intelligence layer in front of the accounting ledger [19]. The system extracts call amounts and entity names automatically. Manual ingestion creates a 30-day reporting lag, forcing investment committees to make decisions based on outdated quarterly numbers [19]. Covenant monitoring in private credit also requires direct software intervention. Ninety-three percent of private equity firms expect intelligence benefits within five years [21]. Legacy platforms fail to handle real-time diversification tracking for modern digital assets [22].

The enterprise market for autonomous agents reached $2.58 billion in 2024 [23]. Analysts project this market segment will hit $24.50 billion by 2030, growing at a 46.2% compound annual rate [23]. Agentic software operates independently across business workflows. Traditional platforms wait for user input before executing actions. Autonomous systems identify infrastructure problems and execute solutions without human oversight [23]. Thirty-three percent of enterprise software applications will include agentic capabilities by 2028 [23]. Organizations report 30% engagement increases after deploying these workflows [23].

Software development requires tight continuous delivery tracking. Adopting internal tools developed for SaaS companies enables managers to monitor deployment bottlenecks. Planview surpassed $400 million in annual recurring revenue during 2023 [24]. The vendor purchased Plutora in late 2024 to add value stream management functions directly into its platform [25]. OpenAI updated its developer software specifically to support multi-step enterprise workflows [26]. Developers use these kits to build agents that write code and run server commands [26].

Agentic loops allow software to reason, act, observe results, and decide on subsequent actions [27]. The ReAct pattern handles tasks involving external information retrieval [27]. Short-term and long-term memory systems separate true autonomous agents from standard conversational bots [27]. Multi-agent networks optimize resources and execute application programming interface actions without human intervention. Partner ecosystems also rely on these algorithms. Artificial intelligence facilitates predictive matching and automated sales enablement for vendor channel networks [28]. Traditional volume-based incentives shift toward outcome-based compensation models driven by software tracking [28].

High interest rates strain leveraged technology vendors. S&P Global Ratings downgraded Planview's debt outlook following its 2024 acquisition [29]. Planview financed the purchase with a $175 million first-lien term loan and a $90 million second-lien term loan [29]. This debt pushed the company's leverage multiple past 10x [29]. S&P affirmed a B- issuer credit rating due to weak cash flow generation [29]. Cautious customer spending caused Planview's revenue growth to slow to 2.3% during early 2024 [29]. The company expects flat revenue growth through the end of 2025 [29].

Other software providers face similar macroeconomic obstacles. Vendors rated B or below carry debt loads exceeding general corporate averages [30]. Applied Systems and

| Year | Market Size (Billion USD) |

|---|---|

| 2023 | 5.3 |

| 2024 | 7.75 |

| 2025 | 8.66 |

The gathered data illustrates a robust acceleration in the global Project Portfolio Management (PPM) software market, scaling from 5.3 billion USD in 2023 to an estimated 8.66 billion USD by 2025 [source]. Alongside this monetary growth is a decisive shift toward cloud deployments, which captured 52.5 percent of the market in 2023 and is projected to account for over 69.4 percent of total revenue in 2025 [source].

On a micro level, this indicates that individual organizations are abandoning rigid, on-premises legacy systems and manual spreadsheet tracking in favor of agile, cloud-native platforms. Project managers are increasingly empowered by remote accessibility, real-time analytics, and seamless integrations with broader enterprise resource planning ecosystems. On a macro industry level, the PPM software category is consolidating as a mission-critical strategic function rather than a mere administrative tool. Enterprise tech budgets are prioritizing these systems to ensure multi-regional alignment, mitigate complex risks, and drive return on investment across massive digital transformation initiatives.

This trend is vital because it redefines how large-scale enterprise capital is allocated and monitored across thousands of simultaneous initiatives. Cloud-based PPM software serves as the foundational infrastructure for emerging artificial intelligence capabilities, with recent surveys indicating that 45 percent of project professionals are already using AI tools in their workflows [source]. Without scalable cloud architecture, businesses cannot leverage the generative AI and predictive analytics required to automate resource allocation, flag portfolio anomalies, and maintain a competitive edge.

A primary catalyst for this shift is the lasting impact of remote and hybrid work models, which fundamentally broke traditional, siloed project management approaches. Furthermore, the sheer complexity and speed of modern digital transformation efforts make it impossible for human analysts to manually spot resource bottlenecks or strategic misalignment in real-time. We can also speculate that the sudden mainstream accessibility of generative AI and machine learning algorithms created an urgent mandate for companies to migrate to the cloud, as on-premises systems generally lack the elastic compute power required for these advanced AI features. Consequently, software vendors have heavily incentivized software-as-a-service subscriptions over perpetual licenses, effectively accelerating the cloud adoption curve across all geographic regions.

The trajectory of the PPM software category proves that effective project execution is now inextricably linked to cloud agility and AI-driven insights. As organizations continue to face intense macroeconomic pressures, they will increasingly rely on these dynamic platforms to prioritize high-value work and automate routine governance. Ultimately, the prominent takeaway is that strategic portfolio management has moved from a back-office reporting function to a centralized, predictive engine that dictates overall corporate success.