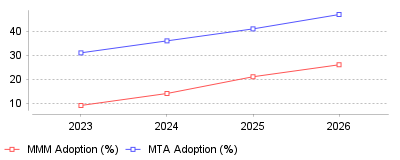

| Year | MMM Adoption (%) | MTA Adoption (%) |

|---|---|---|

| 2023 | 9 | 31 |

| 2024 | 14 | 36 |

| 2025 | 21 | 41 |

| 2026 | 26 | 47 |

This data illustrates a dramatic shift in how marketing analytics and attribution are conducted, specifically highlighting the rapid acceleration of Marketing Mix Modeling (MMM) adoption from just 9% in 2023 to 26% in 2026 [1]. While Multi-Touch Attribution (MTA) continues to grow, serving primarily for tactical day-to-day decisions, organizations are increasingly running hybrid measurement ecosystems where MMM provides strategic, top-down validation [2].

For the macro industry, this represents a fundamental pivot away from deterministic, user-level tracking paradigms that dominated the last decade toward probabilistic, aggregated data models [3]. On a micro level, digital marketing teams are being forced to restructure their analytics workflows, integrating historical spend data, macroeconomic variables, and holdout testing into their daily operations [4]. This dual-model approach means single-touch and strictly client-side attribution systems are no longer viable for enterprise scalability [5]. Consequently, the role of marketing analysts is evolving to require deeper statistical modeling expertise, as organizations rely on Bayesian logic and machine learning to estimate incremental channel contributions rather than simply counting digital footprints [6].

Understanding this trend is crucial because an estimated $10 billion is currently at risk in the United States alone due to advertising signal loss, rendering legacy measurement tools highly inaccurate [7]. As platforms face increasing blind spots from cookie deprecation and tracking prevention frameworks, organizations that fail to adopt modern aggregated models will systemically underfund long-term brand building while over-investing in short-term bottom-funnel tactics [8]. Furthermore, mastering these methodologies protects advertising budgets from being cannibalized by platform self-reporting biases, ensuring that marketing leadership can confidently defend their pipeline numbers to finance committees using resilient, privacy-safe analytics [9].

The primary catalyst for this shift is the systemic signal loss caused by stricter data privacy regulations, such as the GDPR and CCPA, combined with the deprecation of third-party cookies and the introduction of Apple's App Tracking Transparency framework [10]. As these changes obscured up to 40% of previously trackable conversions, the deterministic MTA models began heavily over-crediting natural search and retargeting channels, while leaving up to 38% of business-to-business pipelines entirely unattributable [1]. Additionally, tech giants have actively accelerated this transition; for instance, 's release of its open-source MMM tool, Meridian, significantly lowered the implementation cost and time barriers that historically kept mid-market firms away from econometric modeling [11]. It is highly likely that as consumer adoption of privacy-preserving technologies like Global Privacy Control mechanisms continues to expand, brands had no choice but to resurrect and modernize MMM as the only truly privacy-proof measurement methodology [12].

The analytics landscape is decisively moving toward a dual-measurement standard where Marketing Mix Modeling and Multi-Touch Attribution operate synchronously to reconcile tactical granularity with strategic validity. As privacy guardrails permanently alter digital tracking, marketers can no longer rely exclusively on user-level data to understand their customer journeys or prove return on investment. The most prominent takeaway is that adopting AI-powered, privacy-safe aggregated modeling is no longer a discretionary upgrade, but a mandatory capital expenditure for organizations aiming to sustain profitable growth in a cookieless future [13].

Average marketing budgets fell to 7.7% of overall company revenue in 2024, down from 9.1% the previous year [1]. Chief marketing officers operate under severe financial constraints. 64% of marketing leaders report lacking sufficient funds to execute their annual strategy [1]. Inflationary pressures forced 48.7% of organizations to actively decrease their spending levels in late 2024 [2]. Product manufacturers enacted the steepest cuts, with 52.4% of consumer goods companies slashing promotional expenditures [2].

This financial contraction forces marketing departments to justify every dollar spent through exact measurement. Paradoxically, while promotional budgets shrink, technology investment accelerates. The global marketing analytics market reached $6.15 billion in 2024 [3]. Analysts project this sector will expand at a 17.0% annual growth rate, hitting $29.56 billion by 2034 [3]. Large enterprises capture 68.2% of this software adoption, driven by high data volumes and complex corporate operations [3].

Vendor proliferation compounds this operational complexity. The marketing technology sector contains 15,384 distinct software solutions in 2025, representing a massive expansion from just 150 available tools in 2011 [4]. To rationalize this software sprawl, finance departments demand stricter alignment between advertising performance and corporate revenue. Operations teams increasingly merge departmental data with broader enterprise intelligence infrastructure to validate return on investment across the organization.

Meta lost an estimated $10 billion in advertising revenue during 2022 after Apple introduced the App Tracking Transparency framework in iOS 14.5 [5]. This policy change crippled third-party cookies. iOS required applications to request explicit user permission before tracking activity across external websites. Industry estimates indicate a majority of users declined consent. Advertisers subsequently lost their primary mechanism for tracking cross-app consumer behavior.

Signal loss creates immediate operational blindness. When user conversions fail to register in advertising platforms, machine learning algorithms stop optimizing campaign delivery. Customer acquisition costs inflate artificially. 54% of connected television ad buyers increased their 2024 spending specifically to bypass these signal loss issues [6]. Budgets migrated rapidly toward search channels and walled content environments where first-party data remains intact.

Meta adapted by deploying probabilistic modeling to replace deterministic tracking. By processing available aggregate signals through proprietary artificial intelligence, the company recovered its financial momentum. Meta achieved a global average revenue per user of $56.73 in 2024, a complete recovery from its post-privacy policy slump [5]. Despite platform recoveries, individual advertisers still suffer significant visibility gaps between ad dashboard metrics and actual bank deposits.

A typical enterprise software deal requires 266 distinct touchpoints and 2,879 ad impressions before an organization signs a contract [7]. First-touch and last-touch attribution models fail completely in this environment. Assigning 100% of revenue credit to a single Google Search ad ignores the preceding months of email nurturing, social media engagement, and offline event interactions. Consequently, 78% of B2B marketers struggle with cross-channel data integration [7].

To capture these extended interactions, revenue operations teams deploy specialized tracking applications designed for long sales cycles. Single-model attribution died with cookie deprecation. Multi-touch attribution adoption reached 47% in 2026, becoming the most common tactical model [8]. Concurrently, marketing mix modeling usage jumped from 9% in 2023 to 26% in 2026 [8]. Marketing mix modeling uses statistical analysis on aggregate historical data rather than individual user tracking, making it immune to browser privacy blocks.

Even with advanced modeling, a dark funnel persists. Analysts report that 38% of B2B sales pipeline remains entirely unattributable to any specific marketing activity [8]. Buyers conduct independent research on external forums, Slack communities, and dark social channels that tracking pixels cannot monitor. This measurement gap forces marketing leaders to supplement software data with qualitative customer interviews.

The California Privacy Rights Act and European data restrictions forced a redesign of audience targeting mechanics. Brands can no longer share unencrypted customer lists with external media buyers. They require neutral server environments to match audience profiles safely. Data clean rooms fulfill this requirement by hashing personally identifiable information. Two companies can cross-reference their databases to identify overlapping customers without either party viewing the underlying raw data.

Gartner predicts 80% of advertisers with media budgets exceeding $10 million will integrate data clean rooms by the end of 2025 [9]. The global clean-room technology market will reach $7.85 billion by 2034, expanding at a 6.01% annual rate [10]. Major cloud providers and data aggregators recognize this infrastructure shift. Snowflake acquired Samooha in 2023 to simplify clean room deployment for its clients [10]. LiveRamp purchased Habu the same year to enhance its identity resolution capabilities [10].

These secure environments act as the foundation for modern attribution measurement frameworks. Retailers match their loyalty program databases against publisher subscriber lists to measure exact campaign impact on in-store purchases. PepsiCo uses this method to track offline sales generated by digital media buys without compromising consumer privacy [9]. Despite aggressive investment plans, operational friction persists. Only 2% of businesses actively used data clean rooms in early 2025 due to technical implementation hurdles [11].

Browser-based tracking pixels fail against modern privacy controls. Meta loses 30% to 40% of conversion data when relying exclusively on traditional client-side tracking [12]. Apple Safari and Mozilla Firefox block third-party cookies by default. Ad blockers strip tracking parameters from web addresses. Traditional pixels rely on the user's browser sending data back to the advertising platform. When the browser blocks the script, the platform records zero activity.

Server-side tracking represents the technical response to browser restrictions. Meta's Conversions API and Google's server-side tagging route data differently. Information flows from the user to the company's private server. The company server then sends a direct, secure transmission to the advertising network. This bypasses browser-level privacy controls entirely. It provides a sub-second feedback loop that allows advertising algorithms to optimize delivery in real time [12].

Restoring broken data pipelines yields immediate financial returns. Engineering teams that recover just 20% of lost signals lower their customer acquisition costs dramatically. The platform algorithms function properly again. Small businesses stop pausing their advertising campaigns because their return on ad spend stabilizes. Server-side identity resolution gives platforms a critical advantage over browser-bound measurement tools.

Platform efficiency metrics routinely deceive finance executives. Advertising dashboards often display a healthy 3.5-to-1 return on ad spend while the corporate profit-and-loss statement shows flat revenue growth [13]. This discrepancy stems from attribution windows and algorithmic bias. Platforms claim credit for users who viewed an ad but would have purchased the product anyway. They measure platform efficiency rather than business impact.

Algorithms aggressively favor retargeting audiences with existing purchase intent to deliver the lowest cost per acquisition [14]. Bidding on branded search terms produces the highest theoretical return. However, these tactics contribute minimal incremental value to the business. Judged purely on platform metrics, acquiring net-new customers appears inefficient. Judged on corporate growth, prospecting is essential.

To correct this bias, finance teams implement retention measurement systems to calculate true customer lifetime value. Cost per acquisition means little if the acquired user cancels their recurring contract after one month. Advanced performance teams prioritize incrementality over basic attribution. They require tools that measure downstream revenue margin rather than initial transaction cost.

Retail media network spending will reach $100 billion by 2026 [15]. Platforms like Walmart Connect and Kroger Precision Marketing exploded in popularity by offering closed-loop advertising. Consumer brands buy ads directly on the grocer's website and measure the exact sales resulting from those placements. First-party retailer data eliminates the need for third-party cookies. 68% of marketers state retail media is more important to their strategy than a year ago [15].

Independent retail platforms create severe data fragmentation. Each network operates as an isolated silo with unique data formats, proprietary standards, and differing measurement windows. According to the Association of National Advertisers, 55% of advertisers cite a lack of standardization as their primary retail media challenge [15]. Media buyers cannot easily compare campaign performance across Target, Walmart, and Amazon.

Agencies rely on unified performance interfaces to ingest data from multiple disparate networks. Normalizing this data allows analysts to allocate budgets efficiently across competing retail sites. Concurrently, consumer brands employ digital storefront reporting software to merge their Shopify sales data with Meta advertising costs. Centralized reporting prevents duplicate conversion counting across overlapping media channels.

Machine learning alters attribution mechanics permanently. 73% of marketers currently use or pilot generative artificial intelligence tools [16]. Furthermore, AI agents and autonomous workflows rank as the top expected impact area across the marketing technology sector [4]. When privacy rules block direct user tracking, predictive algorithms analyze historical trends to estimate missing conversion data.

Artificial intelligence attribution lifts holdout test accuracy by 22 points compared to older deterministic models [8]. Platforms automate previously manual tasks. Meta automated campaign management through its Advantage+ suite, shifting budget dynamically across audiences and placements without human intervention. The annual revenue run rate for Meta's AI-powered ad solutions surpassed $60 billion in Q3 2024 [17].

This automation carries severe operational risk. Algorithms optimize delivery aggressively based entirely on the signals they receive. If the tracking infrastructure sends incomplete data due to privacy blocks, the automated system will optimize toward the wrong audience. Ensuring signal integrity becomes the primary responsibility of marketing operations teams. AI represents 9% of total marketing budgets in 2025, up from 7% in 2024 [16].

By 2026, 75% of the global population will fall under modern privacy regulations [18]. Passive data collection is completely obsolete. Companies must audit their data dependencies immediately to identify where third-party information plays a critical role. First-party data infrastructure becomes the most valuable corporate asset. Brands that collect direct consumer preferences through surveys and account registrations will maintain a distinct advantage over competitors relying on external platforms.

Tool consolidation is inevitable. 44% of U.S. marketing teams operate four or more analytical tools simultaneously [19]. Managing multiple tracking pixels slows website performance and creates conflicting data reports. Organizations will reduce their vendor count, favoring platforms that integrate server-side tracking, artificial intelligence modeling, and data clean room compatibility into a single interface.

Marketing analysts must shift from reporting historical metrics to designing strategic signal architecture. They will conduct monthly audits of conversion events. They will compare platform-reported figures against customer relationship management revenue data. The era of cheap, easily tracked digital acquisition has ended. Measurement clarity provides the definitive competitive advantage in a privacy-restricted market.

| Year | MMM Adoption (%) | MTA Adoption (%) |

|---|---|---|

| 2023 | 9 | 31 |

| 2024 | 14 | 36 |

| 2025 | 21 | 41 |

| 2026 | 26 | 47 |

This data illustrates a dramatic shift in how marketing analytics and attribution are conducted, specifically highlighting the rapid acceleration of Marketing Mix Modeling (MMM) adoption from just 9% in 2023 to 26% in 2026 [1]. While Multi-Touch Attribution (MTA) continues to grow, serving primarily for tactical day-to-day decisions, organizations are increasingly running hybrid measurement ecosystems where MMM provides strategic, top-down validation [2].

For the macro industry, this represents a fundamental pivot away from deterministic, user-level tracking paradigms that dominated the last decade toward probabilistic, aggregated data models [3]. On a micro level, digital marketing teams are being forced to restructure their analytics workflows, integrating historical spend data, macroeconomic variables, and holdout testing into their daily operations [4]. This dual-model approach means single-touch and strictly client-side attribution systems are no longer viable for enterprise scalability [5]. Consequently, the role of marketing analysts is evolving to require deeper statistical modeling expertise, as organizations rely on Bayesian logic and machine learning to estimate incremental channel contributions rather than simply counting digital footprints [6].

Understanding this trend is crucial because an estimated $10 billion is currently at risk in the United States alone due to advertising signal loss, rendering legacy measurement tools highly inaccurate [7]. As platforms face increasing blind spots from cookie deprecation and tracking prevention frameworks, organizations that fail to adopt modern aggregated models will systemically underfund long-term brand building while over-investing in short-term bottom-funnel tactics [8]. Furthermore, mastering these methodologies protects advertising budgets from being cannibalized by platform self-reporting biases, ensuring that marketing leadership can confidently defend their pipeline numbers to finance committees using resilient, privacy-safe analytics [9].

The primary catalyst for this shift is the systemic signal loss caused by stricter data privacy regulations, such as the GDPR and CCPA, combined with the deprecation of third-party cookies and the introduction of Apple's App Tracking Transparency framework [10]. As these changes obscured up to 40% of previously trackable conversions, the deterministic MTA models began heavily over-crediting natural search and retargeting channels, while leaving up to 38% of business-to-business pipelines entirely unattributable [1]. Additionally, tech giants have actively accelerated this transition; for instance, 's release of its open-source MMM tool, Meridian, significantly lowered the implementation cost and time barriers that historically kept mid-market firms away from econometric modeling [11]. It is highly likely that as consumer adoption of privacy-preserving technologies like Global Privacy Control mechanisms continues to expand, brands had no choice but to resurrect and modernize MMM as the only truly privacy-proof measurement methodology [12].

The analytics landscape is decisively moving toward a dual-measurement standard where Marketing Mix Modeling and Multi-Touch Attribution operate synchronously to reconcile tactical granularity with strategic validity. As privacy guardrails permanently alter digital tracking, marketers can no longer rely exclusively on user-level data to understand their customer journeys or prove return on investment. The most prominent takeaway is that adopting AI-powered, privacy-safe aggregated modeling is no longer a discretionary upgrade, but a mandatory capital expenditure for organizations aiming to sustain profitable growth in a cookieless future [13].