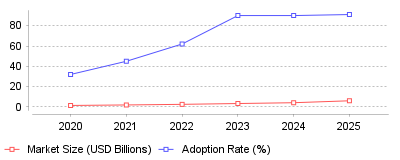

| Year | Market Size (USD Billions) | Adoption Rate (%) |

|---|---|---|

| 2020 | 1.5 | 32 |

| 2021 | 2 | 45 |

| 2022 | 2.6 | 62 |

| 2023 | 3.4 | 90 |

| 2024 | 4.2 | 90 |

| 2025 | 6.1 | 91 |

This trend reveals a massive surge in both the financial valuation of the sales enablement market—scaling from roughly $1.5 billion in 2020 to an estimated $6.13 billion in 2025 [source]—and a corresponding spike in organizational adoption rates. While the percentage of enterprises with dedicated enablement functions skyrocketed from 32% to plateau around 90% over the last five years [source][source], total software spending continues to accelerate exponentially due to deeper tech stack integrations and premium AI feature rollouts.

On a macro-industry level, B2B sales has permanently transitioned from an intuition-based practice to a data-backed, digital-first operational science. Microeconomically, this means individual sales representatives are spending significantly less time doing administrative work or hunting for content—a historical bottleneck where up to 65% of marketing materials went completely unused [source]. The modern platformization of sales enablement allows organizations to consolidate disjointed point solutions into unified suites like Highspot, Showpad, and Seismic that manage the entire buyer lifecycle [source]. Consequently, the massive increase in corporate spending reflects a realization that these platforms are no longer just file-hosting systems, but active, revenue-generating engines.

This explosive growth is crucial because it directly correlates with measurable financial outcomes, effectively turning enablement into a competitive requirement rather than a luxury. Organizations employing formal enablement strategies supported by these platforms report achieving up to 49% higher win rates on forecasted deals compared to those without structured programs [source]. Furthermore, as 90% of companies report implementing or planning to implement AI within their enablement workflows this year, businesses that fail to adopt these advanced digital sales environments risk falling irrevocably behind in buyer engagement and quota attainment [source].

The initial surge in platform adoption was heavily catalyzed by the COVID-19 pandemic, which shattered traditional face-to-face selling and necessitated immediate virtual solutions. Following this shift, the increasing complexity and independence of B2B buying behavior further forced sellers' hands, as modern buyers now heavily prefer self-educating via digital channels before ever speaking to a representative [source]. More recently, the explosive integration of Generative AI has acted as a massive value multiplier, enabling tools to automatically customize pitch decks, provide real-time conversation coaching, and analyze buyer intent without manual human intervention. This ability to definitively prove ROI through reclaimed selling time and hyper-personalized engagement has justified the sustained influx of multi-billion-dollar market investments.

The sales enablement content platform category has rapidly matured from a secondary support repository into the primary technological backbone of modern B2B revenue operations. As embedded AI features and collaborative Digital Sales Rooms become the industry standard, the market's focus has successfully shifted from driving basic adoption to ensuring strategic utilization and hyper-personalization at scale. The prominent takeaway is clear: sales enablement is no longer merely about supplying sellers with static content, but about algorithmically orchestrating the entire buyer-seller interaction to predictably accelerate revenue.

Financial maneuvering defined the sector in early 2026. In February, Seismic acquired Highspot for $6 billion [1]. This transaction united two competitors under a single entity. Vector Capital executed a similar strategy months earlier. The investment firm merged Showpad with Bigtincan to capture mid-market customers [1]. These transactions drastically reduced the number of independent vendors. Procurement teams face fewer choices during contract negotiations. The market for content platforms for enablement reached $6.91 billion in 2026 [2]. Analysts project this figure will hit $20.02 billion by 2033. The sector expands at a 16.4% annual rate [2]. Software vendors initially positioned these products alongside customer relationship and sales software to store collateral. Modern platforms now operate as command centers for revenue teams. North America holds 44.5% of the global market, while the Asia-Pacific region demonstrates the fastest trajectory [2]. Switching costs complicate the vendor evaluation process. Organizations invest months tagging documents and building training modules. Directors hesitate to migrate systems unless the incumbent platform fails completely. This inertia provides consolidated vendors with significant pricing power.

Sixty-one percent of B2B buyers prefer a rep-free experience [3]. Seventy-three percent actively avoid suppliers who send irrelevant outreach [3]. Buyers conduct independent research through digital channels before contacting vendors. This behavior forces sellers to provide specific value during every interaction. Win rates dropped to 20% across business sectors [4]. Quota attainment sits at 42.69% [5]. Deal cycles expanded to 6.5 months [4]. The average purchase involves eight stakeholders [4]. Representatives struggle to navigate these long cycles without proper documentation. Sixty-nine percent of buyers report inconsistencies between website information and seller claims [3]. Organizations address this discrepancy by centralizing content inside the CRM. Representatives access approved sheets directly from the customer record. This integration eliminates version errors.

Marketing departments spend millions producing collateral. According to Forrester, 60% of this material goes unused [6]. Representatives cannot find specific documents during active deals. They default to saving outdated presentations on their local drives. G2 estimates this inefficiency costs enterprise organizations $2.3 million annually [6]. The root problem involves poor taxonomy. Folders fail to organize files effectively. Sellers forget the exact name of a product brief. Modern systems replace folder hierarchies with tagging frameworks. Administrators tag assets by industry, buyer persona, and deal stage. Tracking asset performance drives the adoption of platforms offering playbooks and usage analytics. Marketing directors see exactly which brochures generate revenue. They stop funding ignored formats. Some systems notify sellers when a prospect opens a shared file. This engagement data indicates buyer intent.

Tagging frameworks determine the usability of any repository. Legacy systems relied on nested folders to organize files. This architecture fails when a document belongs in multiple categories. A slide deck might target the healthcare vertical while addressing security protocols. Putting a copy in two folders creates version errors. Modern platforms eliminate folders entirely. Administrators upload a single file and attach multiple tags. Sellers execute Boolean searches to find exact matches. They filter results by industry, persona, and product line. This metadata strategy requires intense discipline from operations teams. Without strict conventions, the database quickly becomes unmanageable. Marketing directors must audit the tag library quarterly. They delete redundant tags to prevent seller confusion. Artificial intelligence simplifies this maintenance burden. Algorithms scan uploaded documents and apply relevant tags automatically. This auto-classification saves hours of administrative work.

Enablement historically focused on quota-carrying representatives. Chief Sales Officers now recognize the limitations of this siloed approach. Fifty percent of executives expect enablement to support marketing and customer success roles [7]. Buyers demand consistent messaging throughout the entire lifecycle. Post-sale teams need access to onboarding guides and renewal documentation. Seventy-three percent of executives prioritize customer growth over new logos [8]. This mandate requires content solutions for broader revenue organizations. Account managers use these portals to identify cross-sell opportunities. Partner networks access localized materials. Organizations consolidate their vendor contracts by purchasing unified platforms. Operations teams reduce administrative overhead. Sellers and support agents operate from a single repository. This alignment prevents disjointed experiences.

Public companies detail their technology investments in federal filings. For fiscal 2026, Salesforce reported $41.5 billion in revenue [9]. The company generated $1.4 billion in recurring revenue from Agentforce and Data 360 [10]. These figures validate the commercial demand for automated workflows. McKinsey notes that artificial intelligence yields 15% productivity increases [4]. Representatives save two hours daily on administrative tasks [4]. Algorithms analyze meeting transcripts to suggest follow-up actions. Software vendors integrate language models directly into their core products. Gong launched Mission Andromeda to provide automated coaching [11]. The system grades calls against custom methodologies. Sellers receive immediate feedback without managerial intervention. Organizations deploy systems that deliver battlecards and talk tracks during live calls. Audio software listens to the buyer. It surfaces relevant scripts instantly. This technology prevents representatives from stumbling when competitors are mentioned.

Chief Financial Officers scrutinize software expenditures heavily. Enablement directors struggle to justify their operating budgets. CSO Insights found only 29% of teams can directly tie their programs to revenue [12]. Forrester notes 67% of leaders cite return measurement as their top challenge [12]. Most departments track completion rates and quiz scores. These activity metrics fail to demonstrate financial value. Business impact requires measuring correlation between training and pipeline generation. Organizations with formal enablement achieve 49% win rates [6]. Teams without dedicated support hover near 42% [6]. The measurement framework must span three distinct tiers. Administrators first track login frequency. They evaluate capability improvements through simulation scores. Finally, operations analysts correlate these scores with quota attainment. Pre-call preparation requires playbook tools built for recurring revenue teams. If representatives who complete a specific certification close larger deals, the software proves its worth. Companies quickly discard platforms that only provide storage capabilities.

Buyers increasingly prefer self-directed research. Forrester survey data reveals 92% of prospects start evaluations with one vendor in mind [13]. Forty-one percent have a single preference before formal evaluation begins [13]. This reality shifts the balance of power. Representatives no longer control the flow of information. Economic pressures shortened buying cycles [13]. Buyers arrive at meetings armed with competitor pricing and feature matrices. Sellers cannot rely on basic questions. They must provide unique insights. Marketing teams build secure portals to facilitate asynchronous deals. These digital rooms house customized videos and legal agreements. Stakeholders review materials on their own schedules. Analytics engines track which executives open specific documents. This behavioral data guides the representative's next action. If a legal director spends ten minutes reading security protocols, the seller anticipates compliance objections.

Product portfolios grow increasingly complex. A single vendor might sell fifty distinct modules. Representatives cannot memorize every technical specification. They rely entirely on digital systems. Allego research indicates 100% of enablement leaders use generative tools to drive performance [14]. Buyers expect representatives to understand their vertical constraints. A pitch delivered to a hospital administrator must differ from one delivered to a factory manager. Platforms assemble dynamic presentations based on CRM data. If an opportunity involves the healthcare sector, the software automatically inserts compliance slides. This automation prevents embarrassing errors. Sellers spend their energy building relationships rather than formatting slide decks. Management teams use call recordings to identify knowledge gaps. They assign micro-learning modules to correct deficiencies immediately. The era of the generalist seller has ended. Market conditions demand specialized expertise.

Heavily regulated industries face massive fines for communication errors. Financial companies must strictly control seller statements. These organizations mandate rigid workflows before publication. Compliance officers review every external document. Enablement platforms lock approved messaging to prevent unauthorized edits. If a regulation changes, administrators instantly recall the outdated asset across all global teams. Local drives present an unacceptable risk. Sellers cannot be trusted to delete old PDFs manually. Centralized distribution guarantees version control. Salesforce noted the risks of artificial intelligence in its federal filings [15]. The company warned that language models might generate inaccurate content [15]. This liability forces software vendors to implement strict protocols. Administrators restrict which data sources the algorithms can access. Furthermore, access controls restrict file visibility. A representative in marketing cannot view confidential contracts meant for legal teams. Administrators establish permission groups during the initial deployment. These security measures protect corporate property.

Deploying an enterprise platform requires intense alignment. Procurement signs the contract, but the real work begins during implementation. Companies frequently underestimate the effort required to audit existing collateral. Marketing teams must delete redundant files before migration. Uploading garbage data into a new system guarantees user rejection. Administrators spend months building integration pipelines. The platform must synchronize with the primary database, email servers, and learning systems. Active Directory integration ensures departing employees lose access immediately. Single sign-on functionality removes friction for daily users. Without these technical bridges, adoption rates plummet. Sellers refuse to log into a separate application just to find a brochure. The software must live where the representatives work. Most vendors offer browser extensions and email plugins to solve this problem. Representatives surface relevant studies without leaving their inbox.

Software providers aggressively shift toward annual licenses. Pricing models vary widely across the sector. Entry-level tools cost ninety dollars per user monthly [6]. Enterprise platforms command significantly higher premiums based on feature access. Vendors charge extra for advanced analytics and coaching modules. This tiering strategy forces organizations to upgrade constantly. Migration costs effectively lock buyers into their chosen platforms. Extracting thousands of tagged assets and historical data requires massive effort. Incumbent vendors understand this leverage during renewal negotiations. They institute annual price escalations of five to seven percent [13]. Procurement directors possess little negotiating power once the sales team relies entirely on the system. The recent wave of mergers exacerbates this issue. Buyers face fewer alternative options when seeking competitive bids. Startups attempt to disrupt the market with specialized tools, but large enterprises prefer purchasing a unified suite.

Sales organizations historically relied on kickoff events for training. Executives flew global teams to centralized locations for three days of presentations. This model completely fails modern retention metrics. Representatives forget the majority of material within weeks. Enablement directors now prioritize continuous learning. They break product updates into brief modules. Sellers consume this content during their daily commutes. Managers track completion rates through dashboard interfaces. They identify which team members skip mandatory modules. Artificial intelligence accelerates this shift. Software analyzes live conversations to detect specific weaknesses. If a seller struggles to explain a pricing change, the system automatically assigns a remediation course. This targeted intervention yields superior results compared to generic sessions. Companies reduce their travel budgets and redirect funds toward software licenses. The modern representative learns constantly rather than occasionally.

The software market will experience severe turbulence through 2027. Acquired companies must integrate their backend systems. Seismic and Highspot face years of database consolidation [1]. Customers typically suffer during these transitional periods. Features break, and support tickets languish in queues. Technology leaders must evaluate their vendor stability. Organizations should document their critical workflows immediately. They must understand exactly which features drive revenue. If a tool only functions as an expensive folder, finance directors will cancel the contract. Operations teams should prepare contingency plans for sudden hikes. The integration of generative algorithms will define the next generation of winners. Vendors failing to deploy functional agents will lose market share. Enablement is no longer a localized function. It operates as the central framework for commercial success. Data accuracy determines pipeline velocity.

| Year | Market Size (USD Billions) | Adoption Rate (%) |

|---|---|---|

| 2020 | 1.5 | 32 |

| 2021 | 2 | 45 |

| 2022 | 2.6 | 62 |

| 2023 | 3.4 | 90 |

| 2024 | 4.2 | 90 |

| 2025 | 6.1 | 91 |

This trend reveals a massive surge in both the financial valuation of the sales enablement market—scaling from roughly $1.5 billion in 2020 to an estimated $6.13 billion in 2025 [source]—and a corresponding spike in organizational adoption rates. While the percentage of enterprises with dedicated enablement functions skyrocketed from 32% to plateau around 90% over the last five years [source][source], total software spending continues to accelerate exponentially due to deeper tech stack integrations and premium AI feature rollouts.

On a macro-industry level, B2B sales has permanently transitioned from an intuition-based practice to a data-backed, digital-first operational science. Microeconomically, this means individual sales representatives are spending significantly less time doing administrative work or hunting for content—a historical bottleneck where up to 65% of marketing materials went completely unused [source]. The modern platformization of sales enablement allows organizations to consolidate disjointed point solutions into unified suites like Highspot, Showpad, and Seismic that manage the entire buyer lifecycle [source]. Consequently, the massive increase in corporate spending reflects a realization that these platforms are no longer just file-hosting systems, but active, revenue-generating engines.

This explosive growth is crucial because it directly correlates with measurable financial outcomes, effectively turning enablement into a competitive requirement rather than a luxury. Organizations employing formal enablement strategies supported by these platforms report achieving up to 49% higher win rates on forecasted deals compared to those without structured programs [source]. Furthermore, as 90% of companies report implementing or planning to implement AI within their enablement workflows this year, businesses that fail to adopt these advanced digital sales environments risk falling irrevocably behind in buyer engagement and quota attainment [source].

The initial surge in platform adoption was heavily catalyzed by the COVID-19 pandemic, which shattered traditional face-to-face selling and necessitated immediate virtual solutions. Following this shift, the increasing complexity and independence of B2B buying behavior further forced sellers' hands, as modern buyers now heavily prefer self-educating via digital channels before ever speaking to a representative [source]. More recently, the explosive integration of Generative AI has acted as a massive value multiplier, enabling tools to automatically customize pitch decks, provide real-time conversation coaching, and analyze buyer intent without manual human intervention. This ability to definitively prove ROI through reclaimed selling time and hyper-personalized engagement has justified the sustained influx of multi-billion-dollar market investments.

The sales enablement content platform category has rapidly matured from a secondary support repository into the primary technological backbone of modern B2B revenue operations. As embedded AI features and collaborative Digital Sales Rooms become the industry standard, the market's focus has successfully shifted from driving basic adoption to ensuring strategic utilization and hyper-personalization at scale. The prominent takeaway is clear: sales enablement is no longer merely about supplying sellers with static content, but about algorithmically orchestrating the entire buyer-seller interaction to predictably accelerate revenue.