ELG Index jumped 180% from 2023 to 2026 as PRM adoption hits 62%

PRM Platform Adoption & Ecosystem-Led Growth

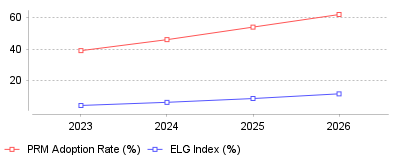

Trend Analysis: Ecosystem-Led Growth in PRM Platforms The data reveals a massive acceleration in the adoption of Partner Relationship Management (PRM) platforms, fueled by a fundamental shift toward Ecosystem-Led Growth (ELG). As direct customer acquisition costs soar, companies are increasingly relying on partner-sourced pipelines to drive efficient revenue. This trend is highly interesting bec

| Year | PRM Adoption Rate (%) | ELG Index (%) |

|---|

| 2023 | 39 | 4.1 |

| 2024 | 46 | 6.1 |

| 2025 | 54 | 8.5 |

| 2026 | 62 | 11.5 |

The Transition to Ecosystem-Led Growth (ELG)

What is this showing

This trend highlights a rapid shift from direct, isolated sales strategies to collaborative ecosystems where companies leverage partner overlaps to source and close deals [1]. PRM platform adoption among mid-market companies has crossed the chasm, jumping from 39% in 2023 to an estimated 62% by 2026, while the Ecosystem-Led Growth Index has grown by a staggering 50% year-over-year [2].

What this means

For the macro industry, this signifies that traditional product-led and sales-led growth models are hitting severe diminishing returns, forcing businesses to scale through collaborative network density [3]. As a result, PRM systems are no longer optional portals but are now mandatory revenue-driving engines. On a micro level, individual sales teams must adapt to nearbound selling, utilizing shared ecosystem data to find warm introductions rather than relying on cold outreach. Companies prioritizing these partner ecosystems are consistently outperforming their peers, with partner-influenced deals closing up to 28 days faster and exhibiting 3.6 times higher win rates [2].

Why is this important

This evolution is critical because the median B2B SaaS company now spends roughly $2.00 to acquire every single dollar of new annual recurring revenue, rendering paid channels heavily saturated and inefficient [1]. Harnessing an ecosystem allows businesses to access pre-qualified, warm pipeline, effectively reducing customer acquisition costs by 30% to 50% [1]. Furthermore, active integration users sourced through PRMs are up to 58% less likely to churn, fundamentally improving a company's long-term net revenue retention [4].

What might have caused this

The primary catalyst for this shift is the skyrocketing cost of direct customer acquisition combined with plunging sub-2% response rates for cold outbound marketing [1]. Buyers are experiencing extreme tool fatigue, utilizing an average of 155 software applications, which makes them far more likely to purchase through trusted integrations rather than standalone vendors [1]. Additionally, major technological strides in PRM platforms, such as the integration of AI for predictive account mapping and automated lead scoring, have made it exponentially easier to track and monetize partner relationships [5]. It is highly probable that as artificial intelligence further streamlines data sharing across networks, managing complex partner ecosystems will become fully automated, leaving companies without a PRM at a severe structural disadvantage.

Conclusion

The explosive adoption of PRM platforms and the mainstreaming of Ecosystem-Led Growth confirm that the future of B2B sales is deeply collaborative. Organizations that continue relying solely on brute-force direct sales will increasingly lose market share to competitors deploying highly connected, data-driven partner networks. The most prominent takeaway is that investing in a robust PRM infrastructure is no longer a luxury, but a fundamental requirement for sustainable, efficient revenue generation in modern software markets.

The Multi-Trillion Dollar Indirect Sales Market

Partner-delivered IT services reached $3.4 trillion in global transaction volume during 2023. Canalys reports this figure accounts for 70% of total technology spending

[1]. Indirect channels dominate modern software distribution. McKinsey researchers project that cross-sector business networks will generate $80 trillion annually by 2030

[2]. Managing these external sales teams requires dedicated infrastructure.

Software tools supporting these indirect sales operations represent a distinct product category. The global market for these coordination tools reached $3.09 billion in 2023. Analysts at SNS Insider project this sector will grow to $4.87 billion by 2032

[3]. Market Research Future offers a slightly higher 2035 forecast of $5.69 billion

[4]. Expanding affiliate networks force vendors to abandon manual spreadsheets in favor of automated management platforms.

The Unspent Funds Crisis

Vendors routinely lose billions of dollars by failing to distribute their own marketing budgets. Sixty percent of market development funds go unused every quarter

[5]. This underutilization leaves between $25 billion and $35 billion untouched annually

[5]. Hardware manufacturers and software developers allocate these funds to help local distributors generate demand.

Fund management programs create intentional friction. Ansira data shows 71% of affiliates struggle to navigate fund approval portals

[6]. Corporate headquarters demands strict proof of execution before reimbursing local marketing expenses. Regional resellers lack dedicated marketing personnel to complete these complex administrative tasks. Small agencies cannot front campaign costs while waiting 90 days for corporate reimbursement.

This operational bottleneck prevents local demand generation. Nearly nine in ten respondents to a 2025 Channel Marketing Association survey stated their ability to measure marketing effectiveness requires improvement

[7]. When marketers cannot prove financial returns, finance departments restrict future budget allocations. Fixing this administrative failure requires modern

partner relationship management software that automates claim approvals. Connected platforms link initial fund requests directly to closed sales opportunities.

Market Consolidation Creates Unified Giants

Financial mergers redefined the software vendor roster throughout 2024 and 2025. Private equity firms recognize that fragmented systems fail enterprise users. Mid-market organizations previously purchased standalone tools for onboarding, deal registration, and incentive compensation. Acquirers now bundle these discrete functions into unified product suites.

Invictus Growth Partners merged Allbound and Channel Mechanics in May 2025 to create Channelscaler

[8]. The combined entity manages 1.1 million registered opportunities valued at $140 billion. Channelscaler CEO Kenneth Fox stated the platform combinations allow vendors to reduce the cost of channel sales through data-driven automation.

AppDirect purchased PartnerStack in April 2026

[9]. PartnerStack controls an active network of 138,000 technology affiliates. AppDirect integrated this network into its core subscription commerce infrastructure. Investcorp led a $70 million funding round for Zift Solutions in January 2023 to accelerate international product expansion

[10]. Capital injections allow these software developers to acquire smaller competitors and build broader operational footprints.

Hyperscaler Marketplaces Rewrite Distribution Rules

Impartner placed its management software on the Microsoft Azure Marketplace in December 2024

[11]. Cloud marketplaces currently operate as dominant procurement channels for enterprise technology. Global spending on cloud infrastructure reached $82 billion in the third quarter of 2024

[12]. Corporate buyers prefer to purchase software through existing Amazon Web Services or Google Cloud contracts to consume committed cloud budgets.

AppDirect acquired Tackle.io in December 2025 to capture transaction volume crossing these specific cloud platforms

[13]. Tackle.io supports $20 billion in total cloud transactions

[13]. B2B software vendors must list their products on these digital marketplaces to remain competitive. Managing external partners who co-sell these digital products requires new operational workflows.

Co-selling alongside cloud providers requires automated pipeline synchronization. Independent software vendors must route leads accurately between external cloud representatives and internal account executives. This coordination relies on secure connections with core

customer relationship management systems. Gartner reported the broader sales software sector grew to $107 billion in 2023

[14]. Without clean data flowing from internal sales databases to external partner portals, accurate deal attribution fails completely.

Artificial Intelligence in Channel Operations

Automation replaces manual account management. Zift Solutions launched the ZiftONE AI Assistant in February 2024

[15]. This generative tool functions as a virtual concierge for local affiliates. It recommends specific marketing materials based on active sales cycles and automatically sequences next steps. Machine learning models reduce the administrative burden on corporate channel managers.

Marketing distribution remains a primary operational hurdle for global brands. Corporate headquarters produces expensive collateral that field representatives ignore. Through-channel marketing automation software solves this exact disconnect. Forrester Research estimated the market for through-channel marketing software reached $1.18 billion in 2023

[16].

Artificial intelligence accelerates content localization. Regional distributors request collateral in multiple languages with co-branded logos. Generative models translate text and format these graphical assets instantly. Partners maintain local brand relevance while adhering to strict corporate messaging guidelines.

Performance tracking improves alongside artificial intelligence deployment. Trackier notes that modern platforms filter attribution data in near real-time

[17]. Predictive algorithms detect fraudulent lead submissions before vendors pay affiliate commissions. Automated software reviews IP addresses and conversion patterns to protect corporate margins from malicious affiliate traffic.

The Onboarding Bottleneck

First impressions dictate affiliate productivity. Most vendor programs suffer from prolonged activation periods. A new regional distributor often waits weeks for portal credentials and technical product training. Complex certification requirements frustrate external sales teams who carry quotas for multiple competing brands.

Effective software compresses this initial timeline. Automated workflows sequence training modules based on the specific partner persona. A technical integration specialist receives API documentation immediately upon registration. A field sales representative receives competitive battle cards and pricing calculators. Personalization keeps external users engaged during their first critical month.

Trackier emphasizes the operational importance of tracking time to activation

[17]. Speeding up the first closed deal secures long-term affiliate loyalty. Vendors measure portal logins, asset downloads, and training completion rates to identify engaged partners. Account managers intervene when analytical dashboards flag inactive distributors.

Niche Applications Expose Legacy Platform Limits

Generic channel software fails specific operational models. Technology vendors prioritize deal registration and cloud consumption metrics. Physical service franchisors measure success through completely different operational indicators. Routing physical assets requires distinct architectural software choices.

Commercial property networks deploy

specialized contractor management applications to distribute work orders to regional franchisees. These systems manage territory exclusivity and equipment financing agreements. A generic lead distribution tool cannot handle the geographic routing rules required by fleet operators. Shift scheduling and local tax compliance require deep vertical specialization.

Financial services demand strict regulatory compliance. Brokers selling insurance products or private equities operate under severe legal scrutiny. Financial groups managing investment syndicates rely on

secure deal flow networks to manage external capital commitments. Portals serving limited partners must integrate identity verification and automated tax document generation. A standard retail affiliate tracker lacks the security controls necessary for financial wealth management.

Data Security and Global Compliance

Distributed networks increase organizational risk. Opening internal corporate databases to external users invites data breaches. Role-based access control restricts visibility to authorized users only. A regional distributor should not access global pipeline forecasts or competitor pricing discounts. Software platforms mitigate this risk by segmenting user permissions strictly by organizational tier.

Compliance requirements force vendors to audit partner communications actively. The European Union General Data Protection Regulation dictates strict rules for international lead sharing. Financial regulators mandate clear audit trails for external commission payments. Software must enforce consent tracking across the entire global distribution network.

Vendors face liability when external partners violate digital marketing regulations. Through-channel marketing platforms lock brand assets to prevent unauthorized edits. Corporate compliance officers monitor social media syndication tools to ensure local agents do not publish deceptive advertising claims. Centralized software allows brands to retract outdated marketing materials simultaneously across thousands of global affiliate portals.

Incentive Compensation and Deal Conflict

Channel conflict destroys partner trust. When an internal sales representative and an external distributor target the same enterprise account, friction follows. Deal registration systems establish clear rules of engagement. The first party to log a qualified opportunity claims the margin discount. PRM software timestamps these entries to prevent commission disputes.

Usage-based billing complicates external partner compensation. Traditional hardware resellers collected upfront retail margins. Modern subscription services require ongoing commission calculations based on monthly customer retention. Vendors must issue recurring micro-payments to affiliates for the entire duration of a client contract.

Software providers adapt their billing engines to support multi-tier compensation architectures. A single software transaction might trigger payments to a digital referral agent, a technology integration partner, and a regional value-added distributor. Legacy financial software cannot process these complex revenue splits. Modern channel platforms integrate directly with corporate enterprise resource planning software to automate monthly payout reconciliations.

Future Outlook

Forrester survey data indicates 67% of B2B leaders expect their indirect revenue to grow faster than direct sales

[18]. Corporate executives view external partnerships as critical efficiency multipliers. Rising digital customer acquisition costs force marketing departments to borrow credibility from established industry voices. Indirect sales channels offer a lower cost of entry into new geographic markets.

Firms that deploy dedicated portal infrastructure will retain top performers. Affiliates naturally gravitate toward vendors offering transparent reporting and rapid commission payouts. The days of managing national distribution networks on standalone spreadsheets ended. Digital platform adoption separates market leaders from stagnant competitors.

Vendors will continue upgrading their channel operations to integrate artificial intelligence. Predictive analytics will guide corporate channel managers toward the most profitable distributor relationships. The software platforms orchestrating these global connections will define the next decade of enterprise revenue growth.