| Year | Abandonment Rate (%) |

|---|---|

| 2020 | 69.82 |

| 2021 | 69.99 |

| 2022 | 69.8 |

| 2023 | 70 |

| 2024 | 70.19 |

Data indicates that across all e-commerce sites, the global average shopping cart abandonment rate has steadily increased, reaching 70.19% in 2024 and projected to remain high [1] [1]. The trend reveals that despite continuous advancements in checkout technology, more than seven out of every ten online shoppers leave their carts without completing a purchase [2] [2].

On a micro level, this trend means individual merchants are losing significant potential revenue at the very bottom of the conversion funnel, effectively wasting the marketing dollars spent acquiring those shoppers. From a macro industry perspective, it signals a major shift in consumer behavior where online shopping carts are increasingly being used as wish lists or comparison tools rather than definitive purchase intents [3] [3]. It also underscores a growing technological divide between merchants who have optimized their checkouts with alternative payment methods and those who still rely on lengthy, traditional account-creation forms [4] [4]. Consequently, e-commerce platforms must continuously evolve their user interfaces to address these abandonment triggers, or they risk falling behind competitors who offer frictionless experiences.

This metric is critically important because cart abandonment accounts for an estimated $18 billion in lost sales revenue annually across the global e-commerce sector [1] [1]. Understanding the specific drivers behind this abandonment empowers businesses to implement targeted recovery strategies, such as retargeting emails and optimized checkout flows, which can successfully recover up to 20% of these lost sales [5] [5]. Furthermore, accurately tracking this data allows retailers to evaluate the return on investment of integrating modern checkout platforms, such as Buy Now, Pay Later (BNPL) or digital wallets, to plug the leaks in their digital sales funnels.

The primary catalyst for this elevated abandonment rate is unexpected costs; approximately 48% of consumers abandon their carts when confronted with surprise shipping fees, taxes, or handling charges at checkout [6] [6]. Additionally, the massive shift toward mobile commerce has exacerbated the issue, as mobile users experience a significantly higher abandonment rate of over 80% due to the friction of navigating complex forms on smaller screens [7] [7]. Another contributing factor is the lack of preferred payment methods, forcing users to manually enter credit card details rather than using seamless digital wallets like Apple Pay or Pay [8] [8]. Finally, it is highly likely that modern economic headwinds have made consumers increasingly price-sensitive, prompting them to routinely abandon carts mid-checkout to search for discount codes or cheaper alternatives on competitor sites.

The data clearly demonstrates that high shopping cart abandonment is an enduring challenge, with the global average cementing itself above the 70% threshold for the foreseeable future. While consumers will always use carts for casual browsing and price comparison, merchants can actively mitigate their losses by adopting transparent pricing, guest checkout options, and modern digital wallet integrations [9] [9]. The most prominent takeaway for e-commerce brands is that checkout friction is a multi-billion-dollar problem, but optimizing the mobile payment experience and eliminating surprise fees can immediately unlock hidden revenue.

Software revenue in the digital commerce market grew 13.4% to reach $11.1 billion in 2023 [1]. Enterprise spending is moving rapidly away from monolithic systems. Gartner projects that 70% of medium and large enterprises will demand modular application planning by 2024 [2]. Organizations evaluating digital retail infrastructure now prioritize platforms that allow them to swap individual components like payment gateways or inventory trackers.

Vendors are responding directly to this enterprise demand. Companies including Shopify, Salesforce, and BigCommerce offer microservices architectures. Composable commerce lets developers use application programming interfaces (APIs) to assemble distinct business functions. Transitioning to this API-first model reduces severe vendor lock-in. A business can change its cart provider without replacing its entire content management system. By 2023, 50% of new commerce capabilities were incorporated as API-centric services [3].

The financial incentive to adopt these flexible frameworks is massive. Analysts project the broader platform sector will swell to $44.46 billion by 2032, expanding at an 18.1% compound annual growth rate [4]. Retailers recognize that rigid software stifles growth. Organizations employing modular architectures outpace their competitors by 80% regarding feature implementation speed [3]. Headless commerce separates the presentation layer from the transaction engine. Marketers design unique interfaces for mobile apps or social media shops while the core engine processes the order seamlessly.

Cloud infrastructure ensures these decoupled systems perform reliably under heavy loads. A brief outage during a peak shopping event destroys revenue instantly. Gartner calculates the cost of enterprise network downtime at $5,600 per minute [5]. Speed dictates success in digital retail. Every second of delay on a payment page increases the likelihood a buyer will abandon the session. Modern cart solutions prioritize low-latency API calls to confirm inventory and process funds.

Target lost mobile checkout conversions when it enforced strict password rules. Customers trying to create an account abandoned the flow rather than invent a complex sequence of characters. Baymard Institute observed an abandonment rate of up to 19% among existing users who struggled with password reset flows during checkout [6]. This specific friction point exemplifies a systemic failure in retail operations.

Abandonment remains an expensive operational failure. Online merchants lose $260 billion in recoverable sales across the United States and the European Union annually [7]. The global cart abandonment rate sits at an alarming 70.22% [8]. Mobile shoppers desert digital carts at a much higher frequency. Transactions fail on smartphones 80.02% of the time, compared to 66.41% on desktop computers [8]. The problem persists despite years of interface updates and usability testing.

Consumers report specific reasons for leaving items behind. Unexpected fees, including taxes and shipping, deter 48% of buyers [9]. Forced account creation stops 26% of potential customers from completing a transaction [9]. Complex forms account for another 18% of lost sales [10]. Site speed and perceived security also disrupt the buying process. Twenty-five percent of customers abandon carts due to security concerns [11]. Retailers upgrading storefront technology must identify tools that offer a guest checkout option. Removing required registration lowers transaction barriers immediately.

Industry verticals experience varying degrees of completion failure. The finance, travel, and non-profit sectors struggle with average abandonment rates exceeding 80% [12]. Retail clothing and consumer goods fare slightly better, recording an average abandonment rate of 72.8% [12]. The grocery sector captures sales more successfully, maintaining a much lower abandonment rate of 50.03% due to purchase necessity [13]. Solving this issue requires targeted interventions rather than generalized redesigns.

Shopify introduced Shop Pay to store customer payment details across its merchant network. Customers bypass manual data entry entirely on subsequent purchases. The average Shopify store converts 1.4% of its visitors into buyers [14]. Elite stores push that baseline figure to 4.7% [15]. Accelerated payment rails separate these high performers from the rest of the market pack.

Shop Pay achieves a conversion rate 1.72 times higher than a standard checkout process [16]. That conversion advantage expands rapidly on mobile devices. Smartphone buyers convert 1.91 times faster using this identity-based path [16]. Digital wallets reduce friction by eliminating form fields. A retail business with $100,000 in monthly revenue and a 2% baseline conversion rate can add up to $50,000 in annual revenue simply by activating these payment tools [16].

Alternative payment rails offer similar performance boosts. Apple Pay and Google Pay provide biometric checks that remove the need for physical cards. Consumers in certain markets rely heavily on local payment methods. Businesses managing high-volume transactions require native support for an array of digital wallets. Displaying a buyer's preferred payment method directly on the product page skips the traditional cart sequence entirely.

Installment providers also drive significant transaction completion. Affirm, Klarna, and Afterpay allow consumers to split large purchases into manageable payments. Missing an installment option at checkout causes 40% of active users to abandon their carts [17]. Thirty-seven percent of US consumers relied on installment services for major shopping events in 2022 [18]. Modern checkout systems handle the risk assessment and funding instantly, removing the merchant from the debt collection process.

Completing a web form does not guarantee a successful sale. Issuing banks frequently decline legitimate purchases due to fraud suspicion. The authorization rate for internet transactions trails physical retail approvals by roughly 10% [19]. When a high-value buyer experiences a false decline, they often switch to a competitor permanently. Repeated false declines degrade the overall profitability of an advertising campaign.

Payment processors rely heavily on machine learning models to format authorization requests. Stripe processed $1.4 trillion in payment volume during 2024 [20]. The processor uses this transaction data to adjust transaction routing dynamically. Hertz gained a 4% authorization rate increase after moving its acquiring operations to Stripe [20]. Small gains yield massive financial returns for enterprise merchants. A firm processing €1 billion annually recovers €10 million in revenue for every percentage point increase in its approval rate [20].

Tokenization replaces card numbers with digital tokens. Visa issued 12.6 billion tokens by early 2025 [21]. Passing a token instead of a raw card number fundamentally changes the issuer risk calculation. Visa recorded a 6% approval rate increase for online merchants submitting tokenized payments [21]. This credential shift lowered fraud rates by 30% simultaneously [21]. Network tokens update automatically when a consumer receives a new physical card. This automatic refresh prevents recurring subscriptions from failing due to expired cards.

Routing also influences approval success. International transactions suffer a 5% to 13% approval penalty compared to domestic sales [20]. Issuing banks apply stricter rules to foreign banks. Merchants implementing payment processing components integrate directly with local acquirers in target countries. A marketplace operating in Brazil improved its authorization rate from 71% to 84% simply by switching from cross-border processing to a local acquiring bank [22]. The buyer behavior remained identical.

Ninety-three percent of procurement managers use digital paths for purchasing [23]. These transaction values dwarf consumer orders. McKinsey tracking shows that 70% of corporate buyers are comfortable making online purchases exceeding $50,000 [24]. Another 27% will spend more than $500,000 in a single digital transaction [24]. Yet business-to-business merchants struggle to process these large orders efficiently.

Friction destroys wholesale metrics. Almost all corporate buyers—98%—experience problems during online payment [23]. Fifty-five percent report speed issues [23]. Credit cards are too expensive for wholesale orders, and buyers expect invoice options. If a merchant fails to offer payment terms, 83% of corporate buyers will abandon the purchase entirely [23]. Legacy systems fail to handle negotiated pricing or shipment invoicing.

Developers configuring platforms for industrial clients must prioritize specialized rails. A team of digital agencies building client sites needs to verify native support for financing and approval workflows. Consumer software lacks the permission structures required by procurement departments. Buyers often need to build a cart and send it to a manager for approval before the order executes.

Self-serve tools dominate corporate buying. Nearly two-thirds of B2B buyers prefer digital or remote engagement over sales meetings [25]. These professionals expect the same seamless experience they enjoy on consumer sites. Wholesalers implementing credit tools reduce underwriting delays. Financing plugins assess buyer creditworthiness instantly. The platform approves net-30 or net-60 terms at the moment of checkout, allowing the transaction to proceed without manual intervention.

Regulators retired version 3.2.1 of the payment security standard in early 2024. The deadline for full compliance with the updated v4.0.1 standard arrives on March 31, 2025 [26]. Regulators designed this mandate to counter threat vectors. Non-compliance invites fines that reach $100,000 per month and the potential revocation of processing abilities [27]. IBM calculates the average cost of a data breach at $6.08 million [20].

Authorities drafted the new rules specifically to stop skimming operations. Cybercriminals routinely inject JavaScript code into trackers loaded during payment flows. The attacker intercepts card data before it reaches a merchant server. Two mandates target this vulnerability. Requirement 6.4.3 forces merchants to maintain an inventory of all scripts executing on a payment page [20]. Administrators must verify the integrity of each script and provide a business justification for its presence.

Requirement 11.6.1 adds monitoring duties. Organizations must deploy detection systems that issue alerts when changes alter HTTP headers or payment page code [28]. Engineering teams now use integrity validation and security policies to block code execution at the browser level. These security layers prevent an infected marketing pixel from reading form fields.

Retailers unable to build compliance tools use redirected pages hosted by processors. Redirects ensure the merchant systems never touch card data directly. However, redirecting a buyer away from the store often increases abandonment. Merchants must balance regulatory compliance with the need for a branded checkout. Payment elements loaded via iframes offer a compromise, keeping the buyer on the domain while outsourcing the compliance burden to the gateway.

Email tools recover only 3.33% of abandoned carts [8]. The delay between a buyer leaving the site and receiving an email renders most recovery attempts useless. Marketers are deploying artificial intelligence to predict intent in real time. Pre-abandonment tools recover between 30% and 38% of transactions [8]. These systems analyze mouse movement, scroll speed, and hesitation to trigger interventions.

Email campaigns fail because they rely on capturing information early in the flow. If a shopper leaves before entering an email address, the merchant has no way to contact them. Fifty to sixty percent of visitors who add an item to their cart never actually start the checkout [29]. Intercepting these buyers requires action. Algorithms display discount codes or shipping thresholds precisely when the user demonstrates exit behavior.

Machine learning also personalizes recommendations during the cart sequence. Stores analyzing visitor data and purchase history optimize content dynamically. Product recommendations increase conversion rates by automatically presenting cross-sells without requiring configuration by a team [30]. A store losing $10,000 monthly to abandonment can recover $2,000 by capturing just 20% of those exiting users with prompts [31]. The return on investment for recovery often ranges from 800% to 1200% [31].

Designing a visual interface does not guarantee a functional one. Over 63% of home screens in shopping apps received a poor or failing grade for compliance [32]. When a checkout lacks text labels or screen reader support, users with disabilities cannot complete their purchases. This demographic controls trillions of dollars in disposable income globally [32]. Excluding them creates a preventable revenue leak.

Mobile ecommerce generated $2.07 trillion in sales during 2024 [32]. Forecasts suggest this number will jump to $3.02 trillion by 2027 [32]. Screen real estate dictates design choices on these small devices. Retailers often rely on icons without supporting text to save space. However, missing ARIA labels break the navigation experience for impaired shoppers. A customer cannot enter their credit card number if their assistive device cannot identify the input field.

Regulators enforce accessibility standards. The Web Content Accessibility Guidelines define the technical requirements for inclusive design. Merchants face legal actions and brand damage. Engineering teams must build checkouts that support keyboard navigation and offer contrast modes. Simplifying the interface to meet these standards simultaneously improves the experience for all users, reducing cognitive load and accelerating the path to purchase.

Merchants face pressure to simplify buying. Consumers refuse to tolerate delays, and declines erode profit margins. The shift toward credentials will accelerate dramatically over the next two years. Visa plans to process 100% of its digital transactions via network tokens by 2030 [33]. This infrastructure upgrade will passively increase win rates without requiring design changes.

Checkout technology will consolidate around identity networks. Shoppers will rely on wallets rather than typing credentials into merchant sites. Stores that force account creation will lose market share rapidly to competitors offering guest paths. Focus will shift entirely from design tweaks to authorization routing, where percentage improvements generate financial value.

Artificial intelligence will automate recovery. Processors currently deploy machine learning to optimize retry timing. A retry system delays a billing attempt until the hour a consumer usually receives their paycheck. These predictive models recover 20% of false declines automatically [34]. Retailers will increasingly treat payments as an optimization channel rather than a cost center.

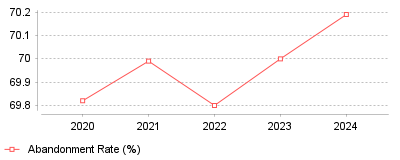

| Year | Abandonment Rate (%) |

|---|---|

| 2020 | 69.82 |

| 2021 | 69.99 |

| 2022 | 69.8 |

| 2023 | 70 |

| 2024 | 70.19 |

Data indicates that across all e-commerce sites, the global average shopping cart abandonment rate has steadily increased, reaching 70.19% in 2024 and projected to remain high [1] [1]. The trend reveals that despite continuous advancements in checkout technology, more than seven out of every ten online shoppers leave their carts without completing a purchase [2] [2].

On a micro level, this trend means individual merchants are losing significant potential revenue at the very bottom of the conversion funnel, effectively wasting the marketing dollars spent acquiring those shoppers. From a macro industry perspective, it signals a major shift in consumer behavior where online shopping carts are increasingly being used as wish lists or comparison tools rather than definitive purchase intents [3] [3]. It also underscores a growing technological divide between merchants who have optimized their checkouts with alternative payment methods and those who still rely on lengthy, traditional account-creation forms [4] [4]. Consequently, e-commerce platforms must continuously evolve their user interfaces to address these abandonment triggers, or they risk falling behind competitors who offer frictionless experiences.

This metric is critically important because cart abandonment accounts for an estimated $18 billion in lost sales revenue annually across the global e-commerce sector [1] [1]. Understanding the specific drivers behind this abandonment empowers businesses to implement targeted recovery strategies, such as retargeting emails and optimized checkout flows, which can successfully recover up to 20% of these lost sales [5] [5]. Furthermore, accurately tracking this data allows retailers to evaluate the return on investment of integrating modern checkout platforms, such as Buy Now, Pay Later (BNPL) or digital wallets, to plug the leaks in their digital sales funnels.

The primary catalyst for this elevated abandonment rate is unexpected costs; approximately 48% of consumers abandon their carts when confronted with surprise shipping fees, taxes, or handling charges at checkout [6] [6]. Additionally, the massive shift toward mobile commerce has exacerbated the issue, as mobile users experience a significantly higher abandonment rate of over 80% due to the friction of navigating complex forms on smaller screens [7] [7]. Another contributing factor is the lack of preferred payment methods, forcing users to manually enter credit card details rather than using seamless digital wallets like Apple Pay or Pay [8] [8]. Finally, it is highly likely that modern economic headwinds have made consumers increasingly price-sensitive, prompting them to routinely abandon carts mid-checkout to search for discount codes or cheaper alternatives on competitor sites.

The data clearly demonstrates that high shopping cart abandonment is an enduring challenge, with the global average cementing itself above the 70% threshold for the foreseeable future. While consumers will always use carts for casual browsing and price comparison, merchants can actively mitigate their losses by adopting transparent pricing, guest checkout options, and modern digital wallet integrations [9] [9]. The most prominent takeaway for e-commerce brands is that checkout friction is a multi-billion-dollar problem, but optimizing the mobile payment experience and eliminating surprise fees can immediately unlock hidden revenue.