| Year | monday.com Revenue (USD Millions) | Asana Revenue (USD Millions) |

|---|---|---|

| 2021 | 308 | 227 |

| 2022 | 519 | 378 |

| 2023 | 730 | 547 |

| 2024 | 972 | 652 |

| 2025 | 1232 | 724 |

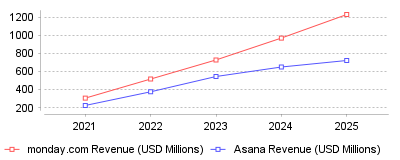

This trend illustrates the financial trajectories of monday.com and Asana, two dominant players in the project and work management software category. Over the past five years, monday.com has drastically accelerated its revenue growth, reaching $1.23 billion in 2025, while Asana's growth has decelerated, logging $724 million in its comparable fiscal year [source].

On a micro level, this data means that monday.com is successfully executing a land-and-expand playbook, particularly among larger enterprise clients. By achieving a 112% net dollar retention rate among customers spending over $50,000 annually, monday.com is extracting significantly more value from its existing user base [source]. Conversely, Asana's net retention rate for large customers has slipped to 95%, indicating a struggle to upsell or retain premium enterprise accounts [source]. On a macro level, the broader project management software market is experiencing rapid expansion, projected to reach over $16.8 billion by 2030 [source]. However, this growth is disproportionately rewarding platforms that consolidate multiple business functions into a single ecosystem rather than pure-play project management tools.

This divergence is crucial for SaaS operators and investors because it demonstrates the limits of a workflow-only product strategy in a consolidating technology market. It underscores that as organizations scale, they prefer comprehensive work operating systems that bridge inter-departmental silos over isolated task management applications [source]. Furthermore, it highlights the importance of product-led efficiency, as monday.com paired its aggressive top-line growth with a robust free cash flow margin, whereas Asana has struggled historically with profitability [source].

A major catalyst for this trend is the differing product philosophies between the two companies. Monday.com aggressively expanded its offerings by releasing dedicated products like CRM and developer tools, allowing it to embed itself deeper into various business units and capture larger software budgets [source]. Asana, meanwhile, played it safe by focusing primarily on core project alignment and AI-driven goal tracking, which lacks the immediate horizontal scalability of a multi-product suite [source]. Additionally, early investments by monday.com in visual customization and diverse dashboard views likely made it more adaptable for non-technical teams compared to Asana's more rigid, text-heavy interface [source]. Finally, executive instability at Asana, including the recent resignation announcement of its founder and CEO, may have hampered strategic execution during a critical market consolidation phase [source].

The project and work management software category is shifting from simple task coordination to full-scale business operations management. Monday.com's decisive financial victory over Asana over the last five years proves that enterprise buyers are prioritizing highly customizable, multi-functional platforms that can replace several disparate tools at once. The prominent takeaway is that in the modern work management landscape, all-in-one workflow adaptability is winning the enterprise revenue race.

Capital disappears at a rate of $48,000 per minute globally due to poor execution [1]. This financial drain reveals a failure within corporate operations. Executives frequently treat task tracking as an administrative function rather than a financial defense. The market for coordination software reached $9.76 billion in 2025 [2]. Mordor Intelligence projects this sector will expand to $23.09 billion by 2031 [2].

Software alone cannot resolve operational inefficiencies. Organizations continue to experience budget overruns despite deploying modern interfaces. Technology vendors attempt to centralize scattered communications. They sell workspaces that converge chat protocols, documentation, and task assignments. Buyers navigating the category of project management and productivity tools face a fragmented market. Understanding these challenges requires examining financial impacts and shifting enterprise demands.

Data from the Standish Group shows 70% of organizational projects fail to meet their original goals [1]. Technology deployments carry a high risk profile. These rollouts run 45% over budget and 7% over time on average [3]. Requirements gathering and scope creep act as the primary culprits. Only 48% of tracked campaigns achieve success against time, budget, and scope criteria [4].

This execution gap leaves vast sums of money on the table. Organizations waste 11.4 cents for every dollar spent due to poor performance [1]. Cost overruns for IT initiatives average 27% above original estimates [1]. High-performing companies waste 28 times less capital than their low-performing peers [1]. Finding suitable project planning tools for agencies and creative teams often centers on billing accuracy to prevent margin erosion. Inefficiencies compound rapidly across active campaigns.

Stakeholder misalignment causes 37% of outright failures [1]. Resolving this disconnect requires strict discipline alongside software deployment. Lack of clear goals ruins 39% of technology initiatives [1]. Changes in corporate priorities kill another 38% of active workstreams [1]. Managers must address these human elements before purchasing new licenses. Software merely accelerates existing processes, whether those processes are functional or broken. A digital interface cannot fix a dysfunctional culture.

Software overload directly harms worker productivity. Marketing departments currently deploy more than a dozen applications on average but activate just 42% of their features [5]. This fragmented setup creates constant context switching. Forrester research indicates 69% of enterprise leaders report that moving between core workspaces and peripheral applications interrupts workflows [6]. Application sprawl generates hidden costs through duplicate licensing and wasted administration hours.

Adding more applications increases network attack surfaces. Security analysts face cognitive overload when tracking alerts across disconnected dashboards [7]. One organization achieved $19.2 million in direct savings over three years simply by consolidating redundant monitoring technologies [8]. Delayed responses occur when security teams must cross-reference data manually. Hackers actively target this complexity.

Service firms face similar visibility issues. Appropriate project management tools for consultants and client projects must centralize client communication securely to prevent data leaks. Disjointed applications force employees to move sensitive files across unprotected channels. IT leaders actively try to halt this software sprawl. They encounter stiff resistance from department heads accustomed to point solutions. Integration difficulties remain severe across the broader market.

Large enterprises run approximately 976 applications, yet only 28% feature database connections [2]. Without standard data structures, automated reporting fails completely. Manual reconciliation tasks consume hours of engineering time. The cost of maintaining proprietary data structures creates migration barriers. Switching costs cause 68% of businesses to hesitate when evaluating new platforms [9].

Blackstone and Vista Equity Partners formalized their $8.4 billion cash acquisition of Smartsheet in late 2024 [10]. This transaction removed an independent vendor from the public markets. Smartsheet shareholders received $56.50 per share, representing a 41% premium over the 90-day average closing price [10]. Private equity firms actively target this software sector for its predictable recurring revenue. Smartsheet reported $286.9 million in third-quarter fiscal 2025 revenue, showing 17% year-over-year growth [11].

Competitors pursue similar growth trajectories. Monday.com posted 2025 fiscal year revenue of $1.23 billion [12]. Their strategic focus centers heavily on corporate accounts. Customers spending over $100,000 annually increased 45% to reach 1,756 accounts by the end of 2024 [12]. The company maintains a 110% net dollar retention rate overall [12]. This figure jumps to 116% for cohorts spending above $50,000 annually [12]. Enterprise customers offer more stable revenue streams because complex software deployments create high switching costs. Organizations embed these tracking tools into their daily operations, making extraction difficult.

Asana demonstrates comparable revenue expansion alongside profitability struggles. The company generated $790.8 million in fiscal 2026 revenue [13]. GAAP net losses reached $189 million during that same twelve-month period [13]. Operating margins remain pressured by intense sales expenditures. Scaling project and work management software requires aggressive acquisition spending. Asana continues to expand its footprint, targeting organizations that require thousands of user licenses. The firm recorded an operating loss of $34 million in the fourth quarter alone [13]. This cash burn highlights the cost of competing against Microsoft and Atlassian.

Consolidation creates a challenging environment for smaller vendors. Scale provides distinct advantages in cloud hosting negotiations and marketing budgets. Startups attempting to enter this space must target specific industry niches. ClickUp reached a $4 billion valuation by betting on workspaces that eliminate the need for separate document editors [2]. Differentiation requires specialized features rather than generic task lists.

Generative models alter standard workflows. Independent analysis indicates 82% of executives plan to insert artificial intelligence into their tracking platforms by 2029 [4]. Vendors are rushing to satisfy this executive demand. Atlassian launched Rovo to connect knowledge bases with execution algorithms [14]. Wrike embedded automated risk forecasting into its interface [15].

Execution remains flawed despite vendor enthusiasm. A recent survey revealed 33% of technology directors believe artificial intelligence actively contributes to fragmentation [6]. Deploying standalone generation utilities isolates data from execution timelines. Implementing project management tools with roadmapping functions requires tight synchronization between predictive algorithms and allocation charts. When forecasting algorithms live in separate browser tabs, managers ignore them. Forrester found that 39% of leaders say implementing AI for solo use cases limits returns [6].

Human capabilities trail software advancements significantly. Only 20% of active project managers possess practical artificial intelligence skills [16]. Teams struggle to format training data properly. Software cannot predict delays if employees input false estimates. Gartner notes mandatory capabilities for work platforms now include intelligent assistance alongside in-context collaboration [17]. Automated meeting summaries represent the most successful initial use case [16].

Machine learning also addresses capacity constraints. Advanced systems assign workload requirements by matching employee availability against specialized skill tags. This automated allocation prevents worker burnout while maximizing billable hours. AI-enhanced platforms could seize 60% of the premium segment by 2025 [9]. Buyers willingly pay premium subscription fees for algorithms that actively prevent deadline failures.

Demographic shifts mandate flexible software architecture. The Project Management Institute tracks 40 million professionals worldwide currently [18]. They project this workforce will expand to 70 million practitioners by 2035 [18]. Remote work arrangements remain dominant within this profession. Post-pandemic data shows 61% of these professionals work remotely at least part-time [16].

Distributed teams require asynchronous communication features. FlexJobs recorded an 11% spike in remote job postings during late 2025 [18]. Organizations cannot rely on physical whiteboards or impromptu desk meetings to verify status updates. Software must serve as the primary coordination layer. This dependency elevates platform uptime from a convenience to a critical operational requirement.

Individual competence still outweighs software features. Only 18% of project professionals demonstrate high business acumen [16]. These exceptional managers achieve remarkable results. Projects led by high-acumen managers experience 27% lower failure rates [16]. Their initiatives meet business objectives 83% of the time, compared to 78% for their low-acumen peers [16]. Training programs must prioritize financial literacy over software certification.

Agile methodologies continue to replace traditional planning frameworks. Teams embrace hybrid styles that blend flexible execution with strict corporate governance. Agile applications allow workers to run sprint cycles and continuous integration pipelines simultaneously. Automatic reporting algorithms cut delivery time by 30% [9]. Software architecture must support multiple execution philosophies within a single corporate account.

Cloud architecture dictates future deployments. Hosted services controlled 74.2% of the market share in 2025 [2]. Hybrid environments post the fastest growth rates as regulated industries modernize their infrastructure [2]. Total IT spending will hit $5.43 trillion in 2025 [3]. Software development and cloud migration initiatives dominate this spending surge.

Annual subscription contracts remain the preferred purchasing model. Yearly billing plans captured 52.7% of category revenue in 2025 [2]. Vendors incentivize these long-term commitments with steep pricing discounts. Enterprise buyers appreciate the predictable expenditure. This dynamic provides software companies with the stable cash flow necessary to fund expensive development operations.

Market fragmentation will eventually decrease. Customers refuse to pay distinct licensing fees for separate chat, document, and task applications indefinitely. Vendors must transition into unified integration hubs connecting finance, customer relations, and human resources databases. The SaaS integration segment is projected to exceed $15 billion [2]. Firms deploying unified integration strategies report 30% productivity lifts [2]. Cloud-native vendors gain significant advantages by offering open API architecture. These pre-built connectors eliminate expensive custom coding for enterprise IT departments.

Financial penalties for inefficient execution are simply too severe to ignore. Only 23% of organizations currently use specialized management software across their entire operation [1]. This low penetration rate indicates massive untapped potential for established vendors and new market entrants. Execution tools will transition from optional productivity boosters to mandatory compliance systems over the next decade.

| Year | monday.com Revenue (USD Millions) | Asana Revenue (USD Millions) |

|---|---|---|

| 2021 | 308 | 227 |

| 2022 | 519 | 378 |

| 2023 | 730 | 547 |

| 2024 | 972 | 652 |

| 2025 | 1232 | 724 |

This trend illustrates the financial trajectories of monday.com and Asana, two dominant players in the project and work management software category. Over the past five years, monday.com has drastically accelerated its revenue growth, reaching $1.23 billion in 2025, while Asana's growth has decelerated, logging $724 million in its comparable fiscal year [source].

On a micro level, this data means that monday.com is successfully executing a land-and-expand playbook, particularly among larger enterprise clients. By achieving a 112% net dollar retention rate among customers spending over $50,000 annually, monday.com is extracting significantly more value from its existing user base [source]. Conversely, Asana's net retention rate for large customers has slipped to 95%, indicating a struggle to upsell or retain premium enterprise accounts [source]. On a macro level, the broader project management software market is experiencing rapid expansion, projected to reach over $16.8 billion by 2030 [source]. However, this growth is disproportionately rewarding platforms that consolidate multiple business functions into a single ecosystem rather than pure-play project management tools.

This divergence is crucial for SaaS operators and investors because it demonstrates the limits of a workflow-only product strategy in a consolidating technology market. It underscores that as organizations scale, they prefer comprehensive work operating systems that bridge inter-departmental silos over isolated task management applications [source]. Furthermore, it highlights the importance of product-led efficiency, as monday.com paired its aggressive top-line growth with a robust free cash flow margin, whereas Asana has struggled historically with profitability [source].

A major catalyst for this trend is the differing product philosophies between the two companies. Monday.com aggressively expanded its offerings by releasing dedicated products like CRM and developer tools, allowing it to embed itself deeper into various business units and capture larger software budgets [source]. Asana, meanwhile, played it safe by focusing primarily on core project alignment and AI-driven goal tracking, which lacks the immediate horizontal scalability of a multi-product suite [source]. Additionally, early investments by monday.com in visual customization and diverse dashboard views likely made it more adaptable for non-technical teams compared to Asana's more rigid, text-heavy interface [source]. Finally, executive instability at Asana, including the recent resignation announcement of its founder and CEO, may have hampered strategic execution during a critical market consolidation phase [source].

The project and work management software category is shifting from simple task coordination to full-scale business operations management. Monday.com's decisive financial victory over Asana over the last five years proves that enterprise buyers are prioritizing highly customizable, multi-functional platforms that can replace several disparate tools at once. The prominent takeaway is that in the modern work management landscape, all-in-one workflow adaptability is winning the enterprise revenue race.