| Year | Market Size (Millions USD) |

|---|---|

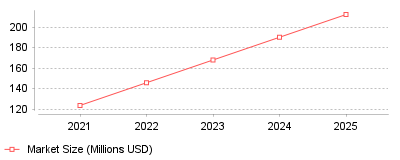

| 2021 | 123.5 |

| 2022 | 145.7 |

| 2023 | 167.9 |

| 2024 | 190.1 |

| 2025 | 212.3 |

The data illustrates a consistent and rapid increase in the onboarding software market size, growing steadily from $123.5 million in 2021 to a projected $212.3 million by 2025 [source]. This upward trajectory highlights the widespread global adoption of digital onboarding solutions aimed at streamlining HR processes, automating administrative tasks, and drastically improving the new hire experience [source].

On a micro level, this means that individual human resources departments are moving away from manual, paper-based orientations and increasingly relying on centralized, digital platforms to manage talent [source]. Organizations are utilizing automation and artificial intelligence to personalize learning paths, track progress, and manage legal compliance far more efficiently [source]. On a macro level, the software industry is experiencing a boom in HR tech investments, with companies prioritizing tools that directly impact employee retention, engagement, and long-term satisfaction [source]. This overarching shift signifies a fundamental transformation in how businesses approach talent integration, viewing it as a critical, data-driven component of overall corporate strategy rather than a simple, one-off administrative task [source].

Implementing robust onboarding software is critical because workplace statistics show that up to 20% of new hires leave within their first 45 days if the integration process is disorganized or ineffective [source]. Conversely, a strong, structured onboarding experience has been proven to boost new hire retention by 82% and improve overall worker productivity by over 70% [source]. Consequently, organizations that invest in these advanced platforms significantly reduce the substantial financial losses associated with high employee turnover, which can cost up to 200% of a departing employee's salary [source].

The primary catalyst for this trend was the global shift toward remote and hybrid work models spurred by the COVID-19 pandemic, which made traditional, in-person onboarding practically impossible for many distributed teams [source]. As a result, companies were forced to adopt remote-friendly digital tools to ensure off-site workers could seamlessly integrate into the company culture and access necessary resources from afar [source]. Additionally, the rising expectations of younger generations, particularly Gen Z and Millennials, who demand intuitive, consumer-grade digital experiences in the workplace, have pressured employers to aggressively modernize their legacy HR tech stacks [source]. Finally, the rapid advancements in artificial intelligence have made these platforms far more intelligent and capable of delivering hyper-personalized training modules, making them a highly attractive and justifiable investment for enterprise buyers [source].

The continuous financial growth of the employee onboarding software market underscores a permanent paradigm shift in modern workforce management and talent acquisition. Companies are no longer viewing onboarding as a short-term administrative hurdle, but rather as a strategic, long-term investment that dictates employee retention and operational productivity. The prominent takeaway is that organizations failing to adopt structured, technology-driven onboarding processes risk losing top talent to forward-thinking competitors who offer a more engaging, personalized, and supportive digital welcome [source].

Global spending on orientation systems reached $2 billion in 2024 [1]. Driving this 13.3% annual increase are cloud deployments across enterprise organizations [1]. ServiceNow controls 13.5% of the sector, followed closely by Workday, SAP, and UKG [1]. By 2029, analysts project software revenues will hit $2.9 billion [1]. Top vendors currently capture more than half of all category spend. Organizations direct capital toward platforms that automate tasks and compliance checks. When building an initial stack, young companies often adopt software for their new hires to digitize paperwork before purchasing secondary tracking modules.

Growth extends rapidly into international regions. The human resources technology market in India is projected to reach $38.36 billion by 2030, growing at a 5.7% compound annual rate [2]. Emerging markets increasingly adopt cloud systems to replace manual documentation. Within the software category, learning management systems generated $18.5 billion globally in 2023 [3]. The gig economy software segment grew 22% to $1.8 billion [3]. Small enterprises expect an 11.8% growth rate through 2031 due to affordable pricing models [3]. Vendors target these smaller businesses with pre-configured templates.

Vendor feature releases reflect an intense focus on automation. Workday released its Spring 2025 updates to include artificial intelligence for talent rediscovery [4]. SAP SuccessFactors matched this pace with its 1H 2025 rollout [5]. This SAP update allows administrators to initiate orientation workflows directly from the recruiting module [5]. Software providers are stripping manual data entry out of the human resources workflow. Administrators no longer need to cancel a workflow if a candidate changes their start date [6].

On March 11, 2024, the U.S. Department of Labor enacted a final rule altering worker classification [7]. The regulation replaces a 2021 standard with a six-factor reality test [8]. This shift impacts companies employing any of the 65 million independent workers in the United States [9]. Human resource departments must immediately update their compliance tools. Misclassifying employees exposes firms to wage theft penalties and tax liabilities. To mitigate compliance risk, firms must deploy software that validates contractor status through automated workflows. The government places particular scrutiny on the degree of control an employer exercises over a worker [7]. Organizations integrating compliance checks into their initial software sequences prevent legal exposure.

State legislatures enact aggressive transparency laws alongside federal changes. California requires job postings to display a compensation estimate [10]. Fines reach $10,000 per violation [10]. Over 50 new workplace laws took effect across half the states recently [10]. Software platforms mitigate this risk by forcing recruiters to populate mandatory fields before publishing a job. Automation engines update wage disclosures based on the candidate's geographic location. Compliance features serve as the primary defense against state auditors.

Rulemaking remains fluid. In February 2026, the Wage and Hour Division proposed another rule to rescind the 2024 standard [11]. This upcoming framework aligns federal enforcement with historical court decisions [11]. Software vendors are scrambling to release updates. System architects must design flexible portals. Hardcoding a legal test into a platform renders it obsolete quickly. Consequently, buyers demand modular architectures that accommodate sudden statutory changes.

Technology rollouts frequently create administrative friction for middle managers. According to Perceptyx data, 81% of supervisors report their workload increased following artificial intelligence deployments [12]. Fifty-one percent of managers carry more responsibilities than they can handle [13]. Meanwhile, 77% of employees place high importance on manager support during early employment [14]. This dynamic traps leaders between software mandates and staff needs. Managers must learn new application interfaces while training their teams. Gartner surveys reveal 40% of managers with two years of experience struggle to guide their departments [14].

Training programs fail to close this capability gap. Only 25% of human resource leaders believe their training investments are working [15]. Supervisors spend less than 30% of their time on leadership duties [15]. The rest is consumed by execution tasks [15]. Burnout cascades through the organization when leaders fail. To combat this fatigue, acquiring companies often force integration sequences onto acquired teams. A human resources platform tailored for portfolio businesses allows directors to standardize supervisor training across separate entities.

Thirty-one percent of workers quit within six months of hire [16]. Up to 17% of new employees depart within the first 90 days [16]. These departures trigger severe financial penalties. The Society for Human Resource Management calculates turnover costs at 90% to 200% of an annual salary [16]. Replacing staff strains departmental budgets. Furthermore, median worker tenure dropped to 3.9 years in January 2024 [17]. This figure falls to 3.5 years for private sector employees [17]. Younger demographics display even shorter retention spans. Workers aged 25 to 34 record a median tenure of 2.7 years [18].

Generational differences influence tenure expectations. Workers aged 55 to 64 display a median tenure of 9.6 years [18]. This older cohort values stability over rapid advancement. However, economic conditions drive turnover more than generational attitudes [18]. Quit rates rise during economic expansions and fall during recessions [18]. Public sector benefits also promote retention. State and local government employees record lower quit rates due to pension access [18]. Software vendors study these demographic patterns to customize their orientation content. A manufacturing employee requires a different software experience than a public school teacher.

Application design directly influences these retention outcomes. Vendors now construct platforms that map the initial months of employment. Using sentiment analysis, applications collect feedback data to predict flight risks. Employees who complete a structured orientation are 69% more likely to remain for three years [19]. Consequently, human resource departments extend software workflows beyond the first week. Effective tools schedule meetings at 30, 60, and 90 days. Supervisors receive automated prompts to discuss career progression. This continuous engagement prevents isolation among recent hires.

The United States staffing market generated $183.3 billion in 2026 [20]. Agencies place over 3 million temporary workers into assignments daily [21]. Looking ahead, 71% of employers plan to use more temporary workers [21]. This volume strains legacy human resources software. Fast-growing agencies dedicate 21.5% of their budget to technology upgrades [22]. Speed dictates financial success in this sector. Implementing a digital portal for temporary workers reduces time-to-fill metrics by 35% to 45% [21]. Agencies adopting automation improve recruiter productivity by up to 40% [21].

Economic uncertainty forces companies to delay permanent hiring. Robert Half reports 45% of employers plan cautious hiring schedules in 2026 [10]. Organizations focus on critical roles and delay less urgent positions [10]. Consequently, 64% of employers use staffing agencies to maintain flexibility [21]. Demand for temporary healthcare workers increased 12% between 2023 and 2024 [21]. Wages for these clinical roles rose 10% to 18% during the same period [21]. Staffing software must process these fluctuating pay rates without generating payroll errors. Days sales outstanding for staffing agencies average 34 to 47 days [21]. Slow client payments increase cash flow pressure. Agencies rely on automated invoicing modules to accelerate collections.

Client expectations force staffing firms to abandon manual processes. Employers evaluate agencies against digital platforms that offer automated credentialing. To compete, traditional firms must use automation to deliver faster placements. Fifty-three percent of staffing executives cite technology costs as a major growth barrier [10]. However, failing to modernize guarantees lost market share. Candidates demand pay transparency and rapid communication. Agencies using mobile applications see 18% to 25% higher assignment retention [21]. Modern software connects candidates directly to payroll systems. This integration prevents delayed payments.

Vendors inject artificial intelligence into every software module. Eighty-four percent of hiring processes use algorithmic screening [23]. Autonomous agents now source, screen, and schedule candidates with minimal human oversight [23]. Fifty-two percent of talent acquisition leaders deploy these autonomous programs [23]. Algorithms summarize resumes and match skills against job descriptions. This speed creates a significant competitive advantage. In vendor management systems, candidates submitted first often win the placement. Software that screens applicants instantly prevents lost revenue.

Workday recently added an intelligent job recommendation engine [4]. The system suggests internal moves based on an employee's experience and interests [4]. SAP integrated AI-assisted writing for messaging within its onboarding tasks [5]. Supervisors use these tools to draft welcome emails and assign training modules. However, algorithm reliance creates new operational risks. Unchecked models replicate historical biases in candidate selection. Organizations must audit their software configurations regularly. Regulators increasingly demand documentation explaining how algorithmic decisions are made.

Software tools cannot solve underlying cultural decay. The United States faces a prolonged workplace mental health crisis. Nearly 90% of employees faced at least one mental health challenge recently [24]. Half of these workers discussed their well-being at work, usually with a direct manager [24]. Supervisors serve as the primary support mechanism for distressed employees. Yet, these same leaders suffer from extreme exhaustion. Two-thirds of supervisors feel their role became more difficult since the pandemic [24]. One in three managers actively plans to change employers [24].

A severe disconnect exists between executive perception and managerial reality. Seventy percent of benefits leaders claim their organizations increased support resources [24]. Conversely, only half of managers agree their company provided additional help [24]. Software platforms must bri

| Year | Market Size (Millions USD) |

|---|---|

| 2021 | 123.5 |

| 2022 | 145.7 |

| 2023 | 167.9 |

| 2024 | 190.1 |

| 2025 | 212.3 |

The data illustrates a consistent and rapid increase in the onboarding software market size, growing steadily from $123.5 million in 2021 to a projected $212.3 million by 2025 [source]. This upward trajectory highlights the widespread global adoption of digital onboarding solutions aimed at streamlining HR processes, automating administrative tasks, and drastically improving the new hire experience [source].

On a micro level, this means that individual human resources departments are moving away from manual, paper-based orientations and increasingly relying on centralized, digital platforms to manage talent [source]. Organizations are utilizing automation and artificial intelligence to personalize learning paths, track progress, and manage legal compliance far more efficiently [source]. On a macro level, the software industry is experiencing a boom in HR tech investments, with companies prioritizing tools that directly impact employee retention, engagement, and long-term satisfaction [source]. This overarching shift signifies a fundamental transformation in how businesses approach talent integration, viewing it as a critical, data-driven component of overall corporate strategy rather than a simple, one-off administrative task [source].

Implementing robust onboarding software is critical because workplace statistics show that up to 20% of new hires leave within their first 45 days if the integration process is disorganized or ineffective [source]. Conversely, a strong, structured onboarding experience has been proven to boost new hire retention by 82% and improve overall worker productivity by over 70% [source]. Consequently, organizations that invest in these advanced platforms significantly reduce the substantial financial losses associated with high employee turnover, which can cost up to 200% of a departing employee's salary [source].

The primary catalyst for this trend was the global shift toward remote and hybrid work models spurred by the COVID-19 pandemic, which made traditional, in-person onboarding practically impossible for many distributed teams [source]. As a result, companies were forced to adopt remote-friendly digital tools to ensure off-site workers could seamlessly integrate into the company culture and access necessary resources from afar [source]. Additionally, the rising expectations of younger generations, particularly Gen Z and Millennials, who demand intuitive, consumer-grade digital experiences in the workplace, have pressured employers to aggressively modernize their legacy HR tech stacks [source]. Finally, the rapid advancements in artificial intelligence have made these platforms far more intelligent and capable of delivering hyper-personalized training modules, making them a highly attractive and justifiable investment for enterprise buyers [source].

The continuous financial growth of the employee onboarding software market underscores a permanent paradigm shift in modern workforce management and talent acquisition. Companies are no longer viewing onboarding as a short-term administrative hurdle, but rather as a strategic, long-term investment that dictates employee retention and operational productivity. The prominent takeaway is that organizations failing to adopt structured, technology-driven onboarding processes risk losing top talent to forward-thinking competitors who offer a more engaging, personalized, and supportive digital welcome [source].