| Year | Employee Adoption Rate (%) | Office Implementation Rate (%) |

|---|---|---|

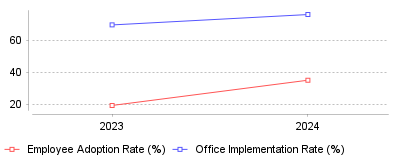

| 2023 | 19.1 | 69.5 |

| 2024 | 34.9 | 76 |

The latest research from late 2024 and early 2025 indicates a massive acceleration in how deeply AI is embedding itself into virtual collaboration. Data tracked through December 2024 reveals that individual employee adoption of tools like ChatGPT nearly doubled in a single year, jumping from 19.1% to 34.9% [1]. Even more telling is the intensity of this usage; recent workforce indices report a staggering 233% increase in daily AI usage between late 2024 and mid-2025, signaling that workers are moving beyond casual queries to relying on AI agents for core operational tasks [2].

We are witnessing the end of the "Shadow AI" era—where employees secretly used tools to cut corners—and the beginning of the "Frontier Firm" era, where AI is an acknowledged member of the team. While 76% of offices now officially incorporate these tools, the metric that matters is the 50% increase in time spent using them [1]. In the micro view, this means the average knowledge worker is offloading repetitive "drudgery" (summarizing threads, drafting emails, data extraction) to focus on complex problem solving. On a macro industry level, this represents a fundamental change in virtual workspace architecture; collaboration platforms are evolving from places where humans talk to each other into command centers where humans direct AI agents to execute work.

This trend is critical because the modern virtual workspace has reached a breaking point regarding human capacity. With meetings occurring after 8 PM rising by 16% year-over-year and digital interruptions occurring every two minutes, the "infinite workday" is leading to widespread burnout [3]. The aggressive uptake of AI is not just about innovation; it is a survival mechanism. Companies that fail to integrate AI as a "digital teammate" risk drowning their human workforce in administrative debt, while "Frontier Firms" utilizing these agents report employees who are 81% more satisfied and significantly more productive [4].

The primary driver is likely the maturation of AI from "chatbots" to "agents" capable of complex reasoning and task execution within collaboration platforms like Slack and Teams. Furthermore, the sheer volume of virtual collaboration—where time in meetings has tripled since 2020—has necessitated a solution to manage the noise [5]. Employees are exhausted by the "digital debt" of hybrid work, and as AI tools became embedded directly into the software they already use (rather than requiring a separate login), the friction to adopt them vanished, leading to the explosive 233% growth in daily use.

The data confirms that 2024-2025 marks the transition point where AI became a non-negotiable layer of the virtual workspace stack. The trend line suggests that the most successful teams are no longer just those with the best human talent, but those who effectively "hire" and manage AI agents to handle the overflow of digital collaboration. Leaders must now focus on "human-agent" team structures, as the adoption gap between AI-native employees and resisters is widening into a definitive productivity divide [6].

Gartner forecasts worldwide IT spending will reach $5.43 trillion in 2025, marking a 7.9% increase from the previous year [1]. While software spending is expected to grow by 10.5% to 14% depending on the specific segment forecasts, the most aggressive growth appears in data center systems, projected to surge over 40% as organizations build the infrastructure necessary for generative AI [1] [2]. This capital allocation signals a transition in the virtual collaboration and team workspace market. Buyers are moving beyond basic connectivity tools adopted during the pandemic and prioritizing intelligent platforms that automate workflows.

Forrester projects global technology spend will touch $4.9 trillion in 2025, with software and IT services combined accounting for two-thirds of that total [2]. This investment is not distributed evenly. North America and Asia Pacific are leading the acceleration, while organizations in EMEA face stricter regulatory environments that may temper adoption rates [3]. For industry veterans, these numbers confirm that the "digital transformation" budget has effectively morphed into an "AI infrastructure" budget, forcing vendors in the broader project management and productivity software sector to re-architect their backends or risk irrelevance.

Gartner predicts that by 2026, 40% of enterprise applications will incorporate embedded "agentic AI"—up from less than 5% in 2025 [4]. Unlike passive assistants that wait for prompts, agentic AI systems operate autonomously to complete multistep workflows. This distinction is critical for buyers. A chatbot summarizes a meeting; an agent detects a decision in that meeting, updates the Jira ticket, and schedules the follow-up review without human intervention.

Atlassian aggressively targeted this shift with the 2024 announcement and subsequent rollout of Rovo, a tool that integrates data across its "Teamwork Graph" to enable these autonomous actions. In its Fiscal Year 2025 Q4 earnings, Atlassian reported that Rovo and related AI features reached 2.3 million monthly active users [5]. This adoption curve suggests that specialized hubs for engineering and product units are moving faster than general administrative functions in deploying autonomous agents.

Microsoft reported similar momentum in its Fiscal Year 2025 Q2 results, citing a 60% increase in usage intensity for Microsoft 365 Copilot [6]. The company's Productivity and Business Processes segment revenue grew 14% to $29.4 billion, driven partly by a 15% increase in commercial cloud revenue as enterprises layered AI subscriptions onto existing seats [7]. For IT directors, the operational challenge has shifted from "how do we deploy video conferencing" to "how do we govern agents that write code and send emails."

Fifty-three percent of shadow AI usage in enterprises now flows through OpenAI, creating a massive single point of failure and risk [8]. A 2025 report from Reco reveals that 27% of employees at small organizations (11-50 employees) use unsanctioned AI tools [9]. This is not merely an IT annoyance; it is a compliance breach waiting to trigger regulatory fines. The report found that some unsanctioned tools remain in use for an average of 400 days, allowing them to become deeply embedded in business processes without security vetting [8].

Menlo Security observed a 50% spike in web traffic to generative AI sites between February 2024 and January 2025, recording 10.53 billion visits [3]. More alarmingly, their telemetry data indicates that 57% of employees using these tools via personal accounts are pasting sensitive company data into them [3]. The operational friction here is palpable: employees are bypassing approved workspaces heavily focused on third-party integrations because they perceive consumer-grade tools as faster or more capable.

IBM's 2024 Cost of a Data Breach Report quantifies this risk. Breaches involving shadow data carried a cost 16% higher than the average, contributing to a global average breach cost of $4.88 million—a 10% jump from the prior year [10] [11]. For financial institutions, the average cost climbed even higher to $6.08 million [12]. Security leaders are now forced to deploy browser-level controls and CASB (Cloud Access Security Broker) solutions specifically to intercept data exfiltration to unauthorized AI endpoints.

Unproductive meetings cost U.S. enterprises an estimated $259 billion annually, according to 2024 research from the London School of Economics [13]. The study highlights that 35% of meetings deliver no value, a figure that drops only slightly when generational diversity is introduced. This inefficiency tax is driving a migration toward asynchronous platforms designed for distributed remote teams that prioritize documentation over live calls.

Zoom's pivot illustrates the market response to this fatigue. In its Fiscal Year 2026 Q3 earnings (reported November 2025), Zoom highlighted that its "Online" business churn had dropped to 2.7%, a historic low, while Enterprise revenue grew 6.1% [14]. The growth driver was not video minutes but the expansion into adjacent asynchronous tools. Zoom Contact Center customers grew 82% year-over-year, and Workvivo (employee experience platform) customers increased 72% [14]. Organizations are consolidating spend with vendors that offer both synchronous video and asynchronous communication layers to reduce context switching.

CIOs are actively culling their SaaS portfolios. While the average enterprise maintained 112+ SaaS applications in previous years, 2024 saw 53% of organizations consolidate redundant applications [15]. The average number of apps per company dropped to 106 in 2024 from 112 in 2023 [16]. This contraction favors platform incumbents like Microsoft and Atlassian while putting pressure on point solutions.

Microsoft's dominance in this consolidation wave is evident in its "More Personal Computing" and "Productivity" segment results. By bundling Copilot, Teams, and Office, they capture wallet share that might otherwise go to niche AI writing tools or standalone project management apps. However, this bundling strategy attracts regulatory scrutiny. The Irish Data Protection Commission fined LinkedIn €310 million in October 2024 for GDPR violations related to tracking and behavioral analysis, signaling that European regulators are watching how these massive platforms process user data [17].

Privacy enforcement has moved from theoretical warnings to balance-sheet impacts. The LinkedIn fine specifically targeted the legal basis for processing data for targeted advertising, ruling that "consent" was not freely given [17]. For collaboration tools, this precedent implies that using employee data to train productivity models requires strict, transparent governance. Vendors can no longer hide data usage policies in fine print.

IBM's analysis found that non-compliance with regulations increased breach costs by an average of $258,000 [10]. Operational teams must now treat compliance not just as a legal hurdle but as a direct component of their workspace architecture. If a collaboration tool cannot guarantee data residency or explainable AI usage, it creates a quantifiable financial liability.

Gartner projects that by 2028, 33% of enterprise software applications will include agentic AI, up from less than 1% in 2024 [18]. This trajectory suggests the next 18 to 24 months will be defined by the "agency gap"—the difference between organizations that successfully deploy autonomous agents to handle routine operations and those stuck managing manual workflows.

Hardware spending will precede software realization. The projected 40%+ growth in data center systems in 2025 indicates that enterprises are racking servers now to support the heavy compute loads of 2026's agents [1]. We expect a bifurcation in the market: premium "agent-enabled" workspaces that command high per-seat prices (e.g., Microsoft 365 Copilot, Atlassian Premium/Enterprise) and legacy "static" workspaces that compete solely on price.

For buyers, the immediate priority is auditing the "shadow AI" footprint. With nearly 27% of employees in small firms actively bypassing IT to use AI tools [9], the operational perimeter has already collapsed. Regaining control requires a strategy that acknowledges the utility of these tools while forcing them behind a managed governance layer.

| Year | Employee Adoption Rate (%) | Office Implementation Rate (%) |

|---|---|---|

| 2023 | 19.1 | 69.5 |

| 2024 | 34.9 | 76 |

The latest research from late 2024 and early 2025 indicates a massive acceleration in how deeply AI is embedding itself into virtual collaboration. Data tracked through December 2024 reveals that individual employee adoption of tools like ChatGPT nearly doubled in a single year, jumping from 19.1% to 34.9% [1]. Even more telling is the intensity of this usage; recent workforce indices report a staggering 233% increase in daily AI usage between late 2024 and mid-2025, signaling that workers are moving beyond casual queries to relying on AI agents for core operational tasks [2].

We are witnessing the end of the "Shadow AI" era—where employees secretly used tools to cut corners—and the beginning of the "Frontier Firm" era, where AI is an acknowledged member of the team. While 76% of offices now officially incorporate these tools, the metric that matters is the 50% increase in time spent using them [1]. In the micro view, this means the average knowledge worker is offloading repetitive "drudgery" (summarizing threads, drafting emails, data extraction) to focus on complex problem solving. On a macro industry level, this represents a fundamental change in virtual workspace architecture; collaboration platforms are evolving from places where humans talk to each other into command centers where humans direct AI agents to execute work.

This trend is critical because the modern virtual workspace has reached a breaking point regarding human capacity. With meetings occurring after 8 PM rising by 16% year-over-year and digital interruptions occurring every two minutes, the "infinite workday" is leading to widespread burnout [3]. The aggressive uptake of AI is not just about innovation; it is a survival mechanism. Companies that fail to integrate AI as a "digital teammate" risk drowning their human workforce in administrative debt, while "Frontier Firms" utilizing these agents report employees who are 81% more satisfied and significantly more productive [4].

The primary driver is likely the maturation of AI from "chatbots" to "agents" capable of complex reasoning and task execution within collaboration platforms like Slack and Teams. Furthermore, the sheer volume of virtual collaboration—where time in meetings has tripled since 2020—has necessitated a solution to manage the noise [5]. Employees are exhausted by the "digital debt" of hybrid work, and as AI tools became embedded directly into the software they already use (rather than requiring a separate login), the friction to adopt them vanished, leading to the explosive 233% growth in daily use.

The data confirms that 2024-2025 marks the transition point where AI became a non-negotiable layer of the virtual workspace stack. The trend line suggests that the most successful teams are no longer just those with the best human talent, but those who effectively "hire" and manage AI agents to handle the overflow of digital collaboration. Leaders must now focus on "human-agent" team structures, as the adoption gap between AI-native employees and resisters is widening into a definitive productivity divide [6].