| Year | Total Cloud Security Market | CNAPP Market |

|---|---|---|

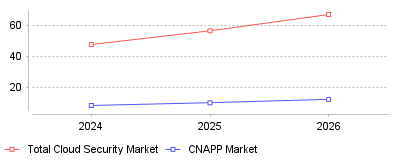

| 2024 | 47.8 | 8.28 |

| 2025 | 56.69 | 10.07 |

| 2026 | 67.24 | 12.25 |

This trend demonstrates a massive architectural pivot in the cybersecurity landscape, where enterprises are aggressively abandoning siloed, single-purpose security tools in favor of unified Cloud-Native Application Protection Platforms (CNAPP) and Data Security Posture Management (DSPM) systems [1]. Survey data indicates that modern organizations are currently juggling an average of 17 discrete cloud defenses, leading to severe "tool sprawl" and fragmented data visibility [1]. As a direct response to this operational chaos, approximately 70% of Chief Information Security Officers (CISOs) are actively consolidating their software solutions into integrated platforms to regain control over their rapidly expanding multi-cloud environments [2].

On a micro level, this consolidation fundamentally transforms the day-to-day operations of security teams. By integrating code scanning, cloud security posture management (CSPM), and runtime protection into a single workflow, analysts experience significantly less context switching and can resolve incidents exponentially faster [3], [1]. Organizations utilizing integrated CNAPP solutions have reported reducing their security-related operational overhead by nearly 30% compared to those reliant on disparate, overlapping tools [3]. On a macro industry scale, this demand for end-to-end visibility is triggering a massive wave of market consolidation, mergers, and acquisitions. Large hyperscalers and dominant security vendors are acquiring smaller, specialized startups—such as 's $32 billion pursuit of Wiz and Rubrik's acquisition of Laminar—to build comprehensive platform ecosystems [4]. Consequently, the global CNAPP market, valued at roughly $8.28 billion in 2024, is projected to surge past $71 billion by 2035, fundamentally narrowing the competitive landscape for standalone security vendors [5], [4].

This transition is critical because the attack surface of modern enterprises has expanded beyond human capacity to monitor manually, largely due to the proliferation of multi-cloud architectures and generative AI [6]. With 88% of organizations now operating across hybrid or multi-cloud setups, consistent policy enforcement has become nearly impossible using legacy perimeter-based defenses [7], [6]. Furthermore, industry experts predict that through 2025, 99% of cloud security failures will be the direct result of customer-driven misconfigurations, highlighting the urgent need for automated, intelligent guardrails that only unified platforms can provide [8]. Without consolidated visibility, security teams face critical blind spots, allowing threats like AI-driven autonomous agents and credential theft to persist undetected in fragmented cloud environments [9], [10].

The root cause of this trend likely traces back to the rapid, often chaotic digital transformations organizations undertook during the pandemic, immediately followed by the explosion of enterprise AI adoption [11]. In the rush to migrate workloads to the cloud, development teams rapidly deployed diverse infrastructure components, prompting security teams to quickly buy niche, point-solution tools to patch immediate vulnerabilities [1]. Over time, this reactionary procurement strategy created a tangled web of overlapping tools that generated thousands of daily alerts—many of them false positives—resulting in severe "alert fatigue" and burnout among cybersecurity professionals [8], [3]. Additionally, the increasing stringency of global data privacy regulations has forced organizations to seek holistic platforms that can simultaneously guarantee compliance, maintain data residency, and enforce threat detection across complex architectures [12]. Ultimately, the financial pressure of maintaining dozens of disparate software licenses combined with the operational friction of siloed workflows created an unsustainable breaking point for enterprise security budgets.

The era of "grafting" isolated security tools onto diverse cloud infrastructure is decisively ending, replaced by a mandate for unified, predictive resilience. As threat actors increasingly leverage autonomous AI to exploit minor misconfigurations across sprawling multi-cloud environments, organizations must adopt consolidated platforms like CNAPP and DSPM to survive and effectively scale [13]. The most prominent takeaway is that platform consolidation is no longer merely a cost-saving procurement strategy; it is a foundational necessity for achieving the real-time visibility, automated remediation, and operational efficiency required to secure the future of digital business.

| Year | Total Cloud Security Market | CNAPP Market |

|---|---|---|

| 2024 | 47.8 | 8.28 |

| 2025 | 56.69 | 10.07 |

| 2026 | 67.24 | 12.25 |

This trend demonstrates a massive architectural pivot in the cybersecurity landscape, where enterprises are aggressively abandoning siloed, single-purpose security tools in favor of unified Cloud-Native Application Protection Platforms (CNAPP) and Data Security Posture Management (DSPM) systems [1]. Survey data indicates that modern organizations are currently juggling an average of 17 discrete cloud defenses, leading to severe "tool sprawl" and fragmented data visibility [1]. As a direct response to this operational chaos, approximately 70% of Chief Information Security Officers (CISOs) are actively consolidating their software solutions into integrated platforms to regain control over their rapidly expanding multi-cloud environments [2].

On a micro level, this consolidation fundamentally transforms the day-to-day operations of security teams. By integrating code scanning, cloud security posture management (CSPM), and runtime protection into a single workflow, analysts experience significantly less context switching and can resolve incidents exponentially faster [3], [1]. Organizations utilizing integrated CNAPP solutions have reported reducing their security-related operational overhead by nearly 30% compared to those reliant on disparate, overlapping tools [3]. On a macro industry scale, this demand for end-to-end visibility is triggering a massive wave of market consolidation, mergers, and acquisitions. Large hyperscalers and dominant security vendors are acquiring smaller, specialized startups—such as 's $32 billion pursuit of Wiz and Rubrik's acquisition of Laminar—to build comprehensive platform ecosystems [4]. Consequently, the global CNAPP market, valued at roughly $8.28 billion in 2024, is projected to surge past $71 billion by 2035, fundamentally narrowing the competitive landscape for standalone security vendors [5], [4].

This transition is critical because the attack surface of modern enterprises has expanded beyond human capacity to monitor manually, largely due to the proliferation of multi-cloud architectures and generative AI [6]. With 88% of organizations now operating across hybrid or multi-cloud setups, consistent policy enforcement has become nearly impossible using legacy perimeter-based defenses [7], [6]. Furthermore, industry experts predict that through 2025, 99% of cloud security failures will be the direct result of customer-driven misconfigurations, highlighting the urgent need for automated, intelligent guardrails that only unified platforms can provide [8]. Without consolidated visibility, security teams face critical blind spots, allowing threats like AI-driven autonomous agents and credential theft to persist undetected in fragmented cloud environments [9], [10].

The root cause of this trend likely traces back to the rapid, often chaotic digital transformations organizations undertook during the pandemic, immediately followed by the explosion of enterprise AI adoption [11]. In the rush to migrate workloads to the cloud, development teams rapidly deployed diverse infrastructure components, prompting security teams to quickly buy niche, point-solution tools to patch immediate vulnerabilities [1]. Over time, this reactionary procurement strategy created a tangled web of overlapping tools that generated thousands of daily alerts—many of them false positives—resulting in severe "alert fatigue" and burnout among cybersecurity professionals [8], [3]. Additionally, the increasing stringency of global data privacy regulations has forced organizations to seek holistic platforms that can simultaneously guarantee compliance, maintain data residency, and enforce threat detection across complex architectures [12]. Ultimately, the financial pressure of maintaining dozens of disparate software licenses combined with the operational friction of siloed workflows created an unsustainable breaking point for enterprise security budgets.

The era of "grafting" isolated security tools onto diverse cloud infrastructure is decisively ending, replaced by a mandate for unified, predictive resilience. As threat actors increasingly leverage autonomous AI to exploit minor misconfigurations across sprawling multi-cloud environments, organizations must adopt consolidated platforms like CNAPP and DSPM to survive and effectively scale [13]. The most prominent takeaway is that platform consolidation is no longer merely a cost-saving procurement strategy; it is a foundational necessity for achieving the real-time visibility, automated remediation, and operational efficiency required to secure the future of digital business.