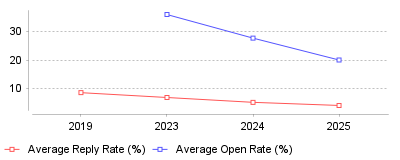

The following research highlights a significant downturn in cold outreach engagement metrics, driven by inbox saturation and stricter provider regulations. This data reveals a critical pivot point for the sales industry: the "volume-first" era is ending, necessitating a shift toward "infrastructure-first" strategies and signal-based targeting.

| Year | Average Reply Rate (%) | Average Open Rate (%) |

|---|---|---|

| 2019 | 8.5 | |

| 2023 | 6.8 | 36 |

| 2024 | 5.1 | 27.7 |

| 2025 | 4 | 20 |

The data reveals a stark, year-over-year decline in the effectiveness of cold email outreach. Specifically, the average cold email reply rate has plummeted from a high of 8.5% in 2019 to approximately 4–5% in 2025 [1]. Simultaneously, open rates have seen a sharp correction, dropping from roughly 36% in 2023 to 27.7% in 2024, with 2025 projections dipping into the 15–20% range due to stricter filtering and image-blocking defaults [2].

On a macro level, this signals the death of the "spray and pray" method that dominated the sales industry from 2020 to 2023. As response rates halve, the cost of customer acquisition (CAC) via outbound channels effectively doubles for teams that refuse to adapt their infrastructure. On a micro level, this trend has birthed a new software category: "Infrastructure-First" sending tools like Instantly.ai and Smartlead.ai, which are rapidly displacing legacy giants like Outreach and Salesloft for pure cold outreach [3]. Sales teams are moving away from single-domain sending toward "inbox rotation" systems—utilizing dozens of secondary domains to spread volume and mitigate the risk of landing in spam [4].

This trend is critical because it fundamentally alters the economics of B2B lead generation. With Alphabet and Yahoo enforcing a strict 0.3% spam complaint threshold as of February 2024, the margin for error has vanished [5]. Companies can no longer solve low performance by simply adding more leads to the funnel; doing so now accelerates domain blacklisting. The market is forcing a quality-over-quantity reset, where success is determined by technical deliverability setups (SPF/DKIM/DMARC) and "signal-based" segmentation rather than raw volume.

The primary driver is the "AI-generated noise" loop: Generative AI lowered the barrier to writing emails, leading to a flood of 361 billion emails sent daily, which overwhelmed decision-makers and triggered "inbox blindness" [6]. In response, major providers like Alphabet and Yahoo implemented the most aggressive anti-spam updates in a decade, specifically targeting bulk senders who fail to authenticate or maintain low complaint rates [7]. Additionally, the saturation of "personalization at scale"—where everyone uses the same AI icebreakers—has desensitized prospects, causing them to ignore messages that would have worked two years ago.

The era of easy outbound wins is over, but cold email remains a viable channel for those who prioritize infrastructure and relevance. The prominent takeaway is that 2025 is the year of "Inbox Protection": teams must adopt multi-domain infrastructures and aim for reply rates above 5% to remain viable [8]. Those who continue to rely on high-volume, single-domain blasts will see their campaigns—and revenue—disappear into the spam folder.

The sales development model that fueled a decade of B2B growth faces a mathematical reckoning. For years, revenue leaders solved pipeline deficits by adding headcount and increasing activity quotas. If open rates dropped, the directive was simple: send more emails. That operational logic collapsed in 2024. Gartner data projects that by 2025, 80% of B2B sales interactions will occur in digital channels [1]. Yet, the efficiency of those channels has degraded inversely to their adoption.

Three structural forces have collided to dismantle the high-volume outreach playbook. First, mailbox providers like Google and Yahoo enforced strict authentication standards in February 2024, converting deliverability from an IT concern into a revenue cap. Second, buyer behavior has shifted toward anonymity; Forrester research indicates that average buying groups now include 13 internal stakeholders, making single-threaded sequencing ineffective [2]. Third, the economics of the Sales Development Representative (SDR) role have inverted. With turnover costs exceeding $97,000 per rep and average tenure stalling at 1.8 years, the cost of acquisition via manual sequencing now frequently exceeds the lifetime value of the customer [3].

We are witnessing a market correction. The sector is moving from capacity-based growth—hiring more bodies to send more messages—to capability-based efficiency. This shift drives the current consolidation in the sales technology sector, exemplified by the merger of Clari and Salesloft, which aims to unify revenue workflows rather than merely accelerating them [4].

Google and Yahoo fundamentally altered the mechanics of cold outreach in February 2024. The new requirements mandate that bulk senders (defined as those sending 5,000+ messages daily) authenticate emails using DKIM, SPF, and DMARC standards. More critically, these providers established a clear spam complaint threshold of 0.3% [5]. This is not a soft target. Exceeding this limit results in domain-wide blocking, effectively silencing a sales team’s primary communication channel.

The operational fallout was immediate. Sales operations leaders were forced to dismantle volume-heavy cadences. A complaint rate of 0.3% means that if three recipients out of 1,000 mark a message as spam, the sender enters the danger zone. This regulatory change killed the viability of buying large, unverified lead lists. Organizations that previously relied on high-velocity activity metrics found their domains burnished. To survive, revenue teams now prioritize email outreach tools with deliverability and warmup features that can throttle sending volume automatically based on engagement signals.

This technical enforcement has economic consequences. Belkins reported that average B2B reply rates dipped to 5.8% in 2024, down from 6.8% the previous year [6]. Martal Group data paints a bleaker picture, citing average response rates between 1% and 5%, with 95% of cold emails failing to generate engagement [7]. The correlation is clear: as inbox providers tighten filters, the "spray" approach results in zero "pray" returns.

The human component of sales sequencing is under intense financial scrutiny. The Bridge Group reports that the average tenure of an SDR is approximately 1.8 years, with a ramp time of over three months [8]. When combined with an annual turnover rate hovering around 39%, organizations face a constant, expensive cycle of hiring and training [9].

The math is unforgiving. If an organization spends $97,690 to replace a rep, and that rep only operates at full productivity for 15 months, the margin for error in pipeline generation is nonexistent. Yet, metrics from Salesforce indicate that 67% of sales reps do not expect to meet their quotas [10].

Companies are responding by automating the bottom of the funnel. The role of the SDR is bifurcating. Entry-level tasks—list building, initial outreach, and qualification—are increasingly handled by AI agents. This necessitates sales email sequencing tools for SDR teams that support "rep-in-the-loop" workflows rather than manual entry. The goal is to reduce the headcount required to generate the same volume of opportunities, shifting budget from salaries to software.

The fragmentation of the sales technology market is ending. Growth Market Reports values the global sales engagement platform market at $8.2 billion in 2024, projecting it to reach $32.7 billion by 2033 [11]. This growth is not being driven by new point solutions but by the expansion of existing platforms. Buyers now prefer consolidated stacks; G2 reports that 84% of software buyers prefer a single solution over multiple disparate tools [12].

The merger of Clari and Salesloft in 2025 exemplifies this trend. The combined entity manages over $10 trillion in revenue, signaling a shift from "sales engagement" to "revenue orchestration" [4]. The value proposition has moved beyond email automation. Enterprise buyers demand full-cycle visibility—from the first cold email to the final contract signature. Consequently, sales email outreach tools integrated with CRM systems are no longer optional; they are the baseline requirement for data integrity.

Smaller players are also adapting. Startups and SMBs, priced out of enterprise platforms, are seeking lightweight sales email tools for small teams that offer enterprise-grade compliance features without the five-figure implementation costs. The regulatory burden of GDPR and CCPA applies regardless of company size, forcing even budget tools to prioritize sophisticated data handling.

The greatest operational challenge facing sales teams today is the complexity of the buying committee. Forrester’s 2024 research highlights that the average buying group now consists of 13 internal stakeholders [2]. More disturbingly, 95% of buyers anticipate using generative AI to support their decision processes, often bypassing sales reps entirely until the final stages [13].

Linear email sequences—Email 1 on Day 1, Email 2 on Day 3—fail in this environment. A single contact cannot carry a deal. If an SDR targets one individual, the outreach is invisible to the other 12 stakeholders. Successful teams are moving toward "multithreaded" engagement strategies that target multiple contacts within an account simultaneously. This requires email sequencing tools with multichannel workflows capable of orchestrating complex plays across LinkedIn, email, and phone, synchronized by account rather than by individual lead.

Furthermore, buyers are exhausted. Gartner notes that 75% of B2B buyers prefer a rep-free sales experience [14]. Outreach must therefore be hyper-relevant to earn attention. The era of the "just bumping this to the top of your inbox" email is over. Value must be delivered in the first touch, often necessitating sales email tools with personalization and snippets that allow reps to inject specific industry insights or company news into automated templates at scale.

In response to declining engagement, sophisticated sales organizations are adopting "signal-based" selling. Instead of targeting cold lists based on static firmographics (e.g., industry, company size), teams target accounts exhibiting dynamic intent signals—hiring surges, funding rounds, or website visits. G2 reports that buyers only engage with salespeople after 69% of the decision-making process is complete [15].

Capturing demand requires intercepting the buyer during that research phase. Tools that integrate intent data directly into sequencing workflows are seeing higher adoption. This is particularly critical for outbound email tools for B2B SaaS prospecting, where the window of opportunity is narrow. A generic sequence sent to a company that just bought a competitor's product is a wasted effort. A sequence triggered by a prospect visiting a "pricing" page, however, yields significantly higher conversion.

The next 24 months will define the "Agentic Era" of sales technology. HubSpot’s launch of "Breeze" and Salesforce’s "Agentforce" indicate that major players are betting on autonomous AI agents to handle the majority of prospecting work [16]. These agents do not just write emails; they research prospects, determine the optimal time to send, and even manage initial replies.

This automation will drive a wedge between high-quality, research-driven outreach and low-quality spam. As AI lowers the cost of generating content, the volume of noise in inboxes will increase. Spam filters will respond with even stricter AI-driven screening. The human seller's role will shift from "generator of volume" to "curator of strategy," overseeing a fleet of AI agents while stepping in only for high-value interactions. Success will depend not on how many emails a team can send, but on how effectively their technology stack can navigate the deliverability and relevance gauntlet.

The following research highlights a significant downturn in cold outreach engagement metrics, driven by inbox saturation and stricter provider regulations. This data reveals a critical pivot point for the sales industry: the "volume-first" era is ending, necessitating a shift toward "infrastructure-first" strategies and signal-based targeting.

| Year | Average Reply Rate (%) | Average Open Rate (%) |

|---|---|---|

| 2019 | 8.5 | |

| 2023 | 6.8 | 36 |

| 2024 | 5.1 | 27.7 |

| 2025 | 4 | 20 |

The data reveals a stark, year-over-year decline in the effectiveness of cold email outreach. Specifically, the average cold email reply rate has plummeted from a high of 8.5% in 2019 to approximately 4–5% in 2025 [1]. Simultaneously, open rates have seen a sharp correction, dropping from roughly 36% in 2023 to 27.7% in 2024, with 2025 projections dipping into the 15–20% range due to stricter filtering and image-blocking defaults [2].

On a macro level, this signals the death of the "spray and pray" method that dominated the sales industry from 2020 to 2023. As response rates halve, the cost of customer acquisition (CAC) via outbound channels effectively doubles for teams that refuse to adapt their infrastructure. On a micro level, this trend has birthed a new software category: "Infrastructure-First" sending tools like Instantly.ai and Smartlead.ai, which are rapidly displacing legacy giants like Outreach and Salesloft for pure cold outreach [3]. Sales teams are moving away from single-domain sending toward "inbox rotation" systems—utilizing dozens of secondary domains to spread volume and mitigate the risk of landing in spam [4].

This trend is critical because it fundamentally alters the economics of B2B lead generation. With Alphabet and Yahoo enforcing a strict 0.3% spam complaint threshold as of February 2024, the margin for error has vanished [5]. Companies can no longer solve low performance by simply adding more leads to the funnel; doing so now accelerates domain blacklisting. The market is forcing a quality-over-quantity reset, where success is determined by technical deliverability setups (SPF/DKIM/DMARC) and "signal-based" segmentation rather than raw volume.

The primary driver is the "AI-generated noise" loop: Generative AI lowered the barrier to writing emails, leading to a flood of 361 billion emails sent daily, which overwhelmed decision-makers and triggered "inbox blindness" [6]. In response, major providers like Alphabet and Yahoo implemented the most aggressive anti-spam updates in a decade, specifically targeting bulk senders who fail to authenticate or maintain low complaint rates [7]. Additionally, the saturation of "personalization at scale"—where everyone uses the same AI icebreakers—has desensitized prospects, causing them to ignore messages that would have worked two years ago.

The era of easy outbound wins is over, but cold email remains a viable channel for those who prioritize infrastructure and relevance. The prominent takeaway is that 2025 is the year of "Inbox Protection": teams must adopt multi-domain infrastructures and aim for reply rates above 5% to remain viable [8]. Those who continue to rely on high-volume, single-domain blasts will see their campaigns—and revenue—disappear into the spam folder.