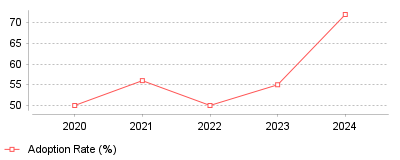

| Year | Adoption Rate (%) |

|---|---|

| 2020 | 50 |

| 2021 | 56 |

| 2022 | 50 |

| 2023 | 55 |

| 2024 | 72 |

This trend illustrates a hyper-accelerated integration of advanced Artificial Intelligence into supply chain analytics platforms over the last 12 months. After hovering around 50% for several years, general enterprise AI adoption surged to 72% in early 2024, while the specific use of Generative AI (GenAI) nearly doubled from 33% to 65% [1] [2, 3]. Concurrently, industry analysts project that software spending on GenAI-enabled supply chain applications will skyrocket from $2.7 billion today to $55 billion by 2029 [2] [4].

At a micro level, this means a fundamental change in the daily workflow of supply chain professionals. Currently, operations leaders spend up to 60% of their time rubber-stamping routine decisions that a system should ideally automate [5] [6]. Early adopters of AI-enabled unified platforms are achieving 2 to 3 times better ROI, reducing logistics costs by 15%, and improving inventory levels by 35% [7] [1, 2]. On a macro scale, the industry is transitioning from passive predictive dashboards—which only offer visibility into what has already happened—toward autonomous "agentic" systems. These agentic tools act independently on real-time data to correct routing errors, reorder stock, and align disparate supply and demand signals without human latency [5] [6, 8].

The global supply chain currently suffers from a massive $1.7 trillion annual cost driven by manual decision-making, suboptimal inventory positions, and excess operational overhead [5] [6, 9]. Traditional supply chain software is severely fragmented, operating on cyclical planning models that fail to respond to real-world volatility. By embedding GenAI and autonomous agents directly into the analytics layer, organizations can process billions of daily data signals to dynamically adjust inventory, optimize transportation routes, and preserve margins. This represents a critical evolution from merely surviving supply chain disruptions to structurally preventing them [10] [9, 11].

The pandemic exposed the fragility of just-in-time logistics and proved that periodic, siloed planning is obsolete in a highly volatile global market. Furthermore, the explosion in capabilities and accessibility of Large Language Models (LLMs) in late 2022 and 2023 provided the technological foundation necessary to handle unstructured supply chain data. The sheer volume of this data—often exceeding 4,000 supply chain signals captured per day by mid-market companies—surpasses human cognitive capacity, mandating algorithmic intervention [5] [6]. Finally, as early adopters deploy these learning loops, they establish a compounding data advantage, forcing competitors to rapidly adopt AI simply to survive [1] [2, 6].

The supply chain and operations analytics sector is experiencing a massive inflection point, defined by the rapid shift toward Generative and Agentic AI. This transition is not just an incremental software update; it is a structural overhaul aimed at solving trillions of dollars in inventory and logistics inefficiencies. The prominent takeaway is that companies clinging to manual decision-making and passive visibility tools will inevitably lose their competitive edge to organizations leveraging unified, autonomous AI platforms.

The software sector continues a rapid expansion phase. Global sales for logistics technology will grow from $5.2 billion in 2022 to $13.5 billion by 2027 [1]. This represents an annual growth rate of 21%. Buyers face severe operational pressures that justify these software investments. Supply network disruptions cost individual organizations an average of $184 million annually [2].

Major incidents at the Panama Canal and the Red Sea forced executives to rethink their routing strategies. KPMG reported in 2024 that sustained logistical bottlenecks could reduce industrial production by 4% to 5% in the near term [3]. Financial losses from these global events demand strict oversight over enterprise operations. Small companies and large corporations alike suffer when raw materials sit stranded on ocean freighters.

Organizations purchase business intelligence software to compile this corporate data. These broad corporate systems often fail to manage specific routing rules or vendor contracts. As a result, companies deploy dedicated specialized analytics platforms to track physical goods. The shift toward cloud infrastructure enables these targeted applications to process information faster than legacy server deployments.

Small and medium enterprises represent a massive growth segment for vendors. Market analysts attribute this expansion to the declining cost of cloud computing and the availability of subscription pricing models. Smaller distributors previously relied on manual spreadsheets to manage complex international freight movements. They now rent processing power from remote data centers to execute complex routing mathematics.

Target reduced its fourth-quarter inventory levels by 12% in 2023 following a period of excessive stock accumulation [4]. Gap reported a 21% year-over-year stock reduction in 2022 to reach $2.4 billion, but paid a steep price to clear its warehouses. The apparel brand saw merchandise margins fall five percentage points due to heavy promotional discounting [5]. Operating income drops significantly when stores slash prices to empty their backrooms.

Retailers misjudged consumer behavior following the pandemic. They ordered excess products to avoid stockouts, which created massive warehouse bottlenecks. Planners now use tools to monitor stock levels in real time. These digital applications trigger automatic reorder alerts and flag obsolete products before markdowns become necessary.

Historical sales data no longer guarantees accurate future projections. Gartner sets the median forecast error rate for durable consumer products at an astonishing 50% [6]. Food and beverage companies fare slightly better with a 25% median error rate. To combat these expensive miscalculations, procurement teams implement predictive models that estimate future sales using external variables like weather patterns and local economic indicators.

Machine learning algorithms deliver measurable improvements to these basic planning workflows. Artificial intelligence reduces forecasting errors by 20% to 50% [7]. Danone utilized these statistical techniques to predict customer requirements and achieved a 30% reduction in lost sales. Similarly, SupChains conducted a pilot program for an international grocery chain and lowered prediction errors by 33% using algorithmic processing [8].

Store operators face additional pressures from consumer price sensitivity. The National Retail Federation noted that inflation fundamentally changed how shoppers evaluate discretionary purchases. Buyers actively seek applications built for retail logistics to replicate successful financial outcomes and protect their gross margins.

U.S. Customs and Border Protection detained 4,619 shipments in 2024 under the Uyghur Forced Labor Prevention Act [9]. Enforcement actions increased substantially in the electronics sector, which accounted for 56% of all targeted containers. Only 17% of the denied shipments originated directly from China [10]. The vast majority arrived from Vietnam, Malaysia, and Thailand.

Government agencies require importers to prove the origin of every component within their finished goods. This strict regulatory environment forces chief operating officers to map their entire vendor networks. Companies deploy software to measure vendor compliance across multiple geographical tiers. These tracking applications log audit results and flag specific factories associated with prohibited labor practices.

The enforcement strategy expands every year. Federal authorities added five specific target sectors to their priority list in 2025, including copper, lithium, and steel [11]. The official entity list grew to 144 organizations, representing a sharp escalation in trade scrutiny. Supply chain managers scramble to replace prohibited partners before border agents seize incoming freighters.

Environmental regulations present another massive compliance burden for public corporations. The Securities and Exchange Commission approved rules requiring large accelerated filers to disclose Scope 1 and Scope 2 emissions beginning in 2026 [12]. The federal agency excluded Scope 3 emissions due to cost complaints, but state legislators quickly filled that gap. California passed Senate Bill 253 to force large organizations to report Scope 3 network emissions by 2027 [13].

Executives face personal liability for inaccurate public disclosures. They mandate the use of systems that identify network vulnerabilities before external auditors discover them. Algorithms scan bills of lading and cross-reference them against government watchlists to prevent illegal imports from docking at domestic ports.

Technology enthusiasm currently masks severe structural deficits within factory environments. A 2024 McKinsey survey revealed that 65% of organizations use generative artificial intelligence regularly, which represents a massive spike from the previous year [14]. Conversely, 90% of logistics executives admit their companies lack the digital talent required to meet their actual transformation goals [15].

Industrial leaders want to optimize physical production floors rather than just automate office tasks. The World Economic Forum added 21 advanced facilities to its Global Lighthouse Network in 2023 to showcase successful mechanical integrations [16]. Plant managers use software to monitor production floors and eliminate machine downtime. These facilities treat entire factories as pilot programs rather than testing isolated features.

Agilent Technologies provides a clear blueprint for this operational shift. The laboratory equipment manufacturer deployed connected sensors and predictive models at its Waldbronn facility. This technical overhaul generated a 35% increase in manufacturing quality [17]. The company also reported a 44% productivity boost and a 48% rise in total output while navigating severe component shortages.

Physical execution requires clean sensor data. Factory operators install cameras equipped with computer vision to inspect products moving across conveyor belts. These automated systems detect microscopic defects that human inspectors miss. Defect reduction lowers material waste and improves overall gross margins for the enterprise.

Sustainability targets align directly with these mechanical efficiency gains. Facilities in the Lighthouse Network use digital twins to simulate energy consumption. One recognized site reduced water intake by 35% and cut energy-related emissions by 34% over a five-year period [16]. Machine learning schedules container loading to minimize empty truck miles, proving that environmental stewardship generates tangible financial returns.

Blue Yonder acquired One Network Enterprises for $839 million in early 2024 [18]. This massive transaction pushed the software vendor's total acquisition spending past $1 billion over a nine-month period. Competitors watch these investments closely as enterprise buyers demand unified software suites rather than fragmented point solutions. The preceding acquisitions of flexis AG and Doddle confirm a clear strategy to dominate every logistical touchpoint.

Software developers want to own the entire data lifecycle from raw material extraction to final customer delivery. One Network gave Blue Yonder access to a digital network featuring 150,000 active trading partners. This pre-built community allows buyers to instantly connect with suppliers without undergoing lengthy technical integrations. Planners instantly shift orders from one factory to another when regional disruptions occur.

Established software giants generate massive revenue from this exact consolidation trend. SAP reported a 33% increase in its Cloud ERP Suite revenue for the 2024 fiscal year [19]. The German technology firm reached €14.2 billion in cloud revenue as legacy clients finally migrated away from older server deployments. Cloud architecture allows developers to push algorithmic updates globally without requiring local IT departments to install manual patches.

Financial markets reward vendors that successfully transition to subscription billing models. SAP grew its total cloud backlog to €63.3 billion, representing a 43% increase over the previous year. Technology buyers write massive checks for these platforms because disjointed systems fail to provide adequate visibility during geopolitical crises.

Data governance dictates the success of every algorithmic software deployment. Gartner identified strict supply chain data governance as a primary technology trend for 2024 [20]. Machine learning models fail completely when companies feed them unstructured or inaccurate vendor records. Algorithms require clean inputs to output actionable mathematical recommendations.

Cyber extortion poses a direct threat to physical logistics networks. Criminal syndicates deploy ransomware to halt factory operations and delay port shipments. Gartner notes that two-thirds of global businesses suffer ransomware attacks, resulting in severe revenue losses [21]. Modern software must include strict access controls and encrypted databases to prevent catastrophic operational shutdowns.

Analysts expect vendors to blend multiple mathematical techniques rather than relying on single statistical models. This composite approach allows planners to cross-reference weather forecasts, port strike probabilities, and historical sales trends within a single dashboard. Software buyers will reward vendors that deliver verifiable cost reductions rather than empty marketing promises.

Hardware innovations will soon merge with these analytical platforms. Next-generation humanoid robots stand ready to automate warehouse picking tasks [22]. These mechanical units require continuous data feeds from central software networks to function efficiently. The separation between physical labor and digital analytics will disappear entirely over the next five years.

| Year | Adoption Rate (%) |

|---|---|

| 2020 | 50 |

| 2021 | 56 |

| 2022 | 50 |

| 2023 | 55 |

| 2024 | 72 |

This trend illustrates a hyper-accelerated integration of advanced Artificial Intelligence into supply chain analytics platforms over the last 12 months. After hovering around 50% for several years, general enterprise AI adoption surged to 72% in early 2024, while the specific use of Generative AI (GenAI) nearly doubled from 33% to 65% [1] [2, 3]. Concurrently, industry analysts project that software spending on GenAI-enabled supply chain applications will skyrocket from $2.7 billion today to $55 billion by 2029 [2] [4].

At a micro level, this means a fundamental change in the daily workflow of supply chain professionals. Currently, operations leaders spend up to 60% of their time rubber-stamping routine decisions that a system should ideally automate [5] [6]. Early adopters of AI-enabled unified platforms are achieving 2 to 3 times better ROI, reducing logistics costs by 15%, and improving inventory levels by 35% [7] [1, 2]. On a macro scale, the industry is transitioning from passive predictive dashboards—which only offer visibility into what has already happened—toward autonomous "agentic" systems. These agentic tools act independently on real-time data to correct routing errors, reorder stock, and align disparate supply and demand signals without human latency [5] [6, 8].

The global supply chain currently suffers from a massive $1.7 trillion annual cost driven by manual decision-making, suboptimal inventory positions, and excess operational overhead [5] [6, 9]. Traditional supply chain software is severely fragmented, operating on cyclical planning models that fail to respond to real-world volatility. By embedding GenAI and autonomous agents directly into the analytics layer, organizations can process billions of daily data signals to dynamically adjust inventory, optimize transportation routes, and preserve margins. This represents a critical evolution from merely surviving supply chain disruptions to structurally preventing them [10] [9, 11].

The pandemic exposed the fragility of just-in-time logistics and proved that periodic, siloed planning is obsolete in a highly volatile global market. Furthermore, the explosion in capabilities and accessibility of Large Language Models (LLMs) in late 2022 and 2023 provided the technological foundation necessary to handle unstructured supply chain data. The sheer volume of this data—often exceeding 4,000 supply chain signals captured per day by mid-market companies—surpasses human cognitive capacity, mandating algorithmic intervention [5] [6]. Finally, as early adopters deploy these learning loops, they establish a compounding data advantage, forcing competitors to rapidly adopt AI simply to survive [1] [2, 6].

The supply chain and operations analytics sector is experiencing a massive inflection point, defined by the rapid shift toward Generative and Agentic AI. This transition is not just an incremental software update; it is a structural overhaul aimed at solving trillions of dollars in inventory and logistics inefficiencies. The prominent takeaway is that companies clinging to manual decision-making and passive visibility tools will inevitably lose their competitive edge to organizations leveraging unified, autonomous AI platforms.