| Year | Microsoft Teams DAU | Zoom DAU |

|---|---|---|

| 2020 | 20 | 300 |

| 2021 | 75 | 300 |

| 2022 | 145 | 300 |

| 2023 | 270 | 300 |

| 2024 | 320 | 300 |

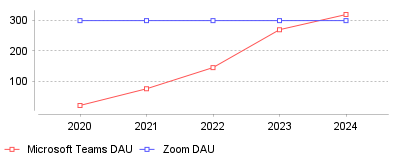

This trend tracks the daily active users (DAU) of two major UCaaS platforms, Microsoft Teams and Zoom, between the years 2020 and 2024 [1]. It illustrates that while Zoom experienced an immediate explosion to 300 million DAU during the initial pandemic shift and plateaued, Microsoft Teams exhibited sustained, compounding growth from 20 million to 320 million DAU, ultimately surpassing Zoom's daily active user count [2].

At a micro level, this data means individual organizations are increasingly migrating away from fragmented communication tech stacks in favor of centralized platforms. Companies are finding substantially more value in systems that natively bundle chat, voice, video, and document collaboration into a single, cohesive interface. On a macro industry level, this signifies a structural shift in the UCaaS market toward enterprise-wide ecosystems, heavily favoring tech giants that already own the broader productivity suite [3]. Consequently, standalone communication applications are being forced to pivot their strategies, often emphasizing external communications, API flexibility, or specialized AI features to maintain relevance against these bundled mega-platforms [4].

This evolution is critical because it dictates how billions of dollars in enterprise IT budgets are allocated across the globe. The convergence of UCaaS with broader productivity and artificial intelligence tools means software lock-in is becoming stronger, making it significantly harder and more expensive for companies to switch providers once they are fully embedded [5]. Furthermore, it highlights the fundamentally changing nature of modern work, where seamless internal collaboration, workflow automation, and persistent workspaces are prioritized over simple, ad-hoc video meeting capabilities [6].

The initial catalyst for both platforms was undeniably the sudden global shift to remote work, which rapidly inflated the user bases of all cloud communication platforms almost overnight. However, Microsoft Teams' sustained and superior growth can largely be attributed to its strategic bundling within the Microsoft 365 suite, effectively making it a cost-free or default option for millions of enterprise users who already utilize Microsoft products [7]. Additionally, the deep integration of next-generation AI-powered tools, such as Microsoft Copilot, has created a powerful productivity loop that keeps users engaged within a single ecosystem rather than switching contexts to external applications [8]. Finally, as organizations moved past the emergency deployment phase of remote work, IT leaders likely sought to consolidate enterprise software spending, naturally favoring comprehensive, all-in-one platforms over paying premium licensing fees for separate, disparate communication tools [9].

The trajectory of Microsoft Teams' DAU compared to Zoom reveals a maturing UCaaS market that heavily rewards bundled, deeply integrated enterprise ecosystems over niche or standalone video solutions. As artificial intelligence continues to be woven into the fabric of these platforms, the technical and financial barrier to entry for new challengers will only grow steeper. The prominent takeaway is that the future of UCaaS lies not merely in facilitating communication, but in serving as the centralized, automated nervous system for the entire digital workplace.

Microsoft reported that its Copilot software reached 100 million monthly active users across commercial and consumer segments in the fourth quarter of fiscal year 2025 [1]. Adoption rates for enterprise communication platforms stabilized following rapid expansion periods in previous years. Technology buyers face new operational hurdles managing software deployments at scale. Unified communications software no longer functions solely as a replacement for physical desk phones. Voice, video, and text channels act as primary data inputs for artificial intelligence models. This architectural change forces network administrators to evaluate vendors based on application programming interfaces rather than basic call routing features.

Enterprise communication relies heavily on continuous uptime and secure data transmission. Platform inconsistencies cause severe operational delays for distributed workforces. Industry analysts track shifting procurement requirements as companies attempt to centralize their digital communication environments. Software vendors respond by merging disparate product categories into unified platform interfaces. This article analyzes current financial metrics, regulatory compliance challenges, and operational shifts affecting modern communication architectures.

Worldwide revenues for unified communications reached $69.2 billion in 2024. This figure represents a 7.8% year-over-year increase according to International Data Corporation [2]. Market analysts expect cumulative revenues to reach $85.4 billion by 2029, representing a 3.9% compound annual growth rate [2]. Microsoft controls the largest portion of this revenue pool. The software provider generated $31.5 billion in sector revenue during 2024 [3]. This total captured 45.6% of global market share, marking a 2.4% gain over the previous calendar year [3]. Zoom followed with $4.3 billion in annual revenue and a 6.2% market share [3]. Zoom's fourth-quarter fiscal 2025 earnings report showed total quarterly revenue of $1.18 billion, with enterprise clients contributing $706.8 million [4]. Cisco experienced a 4.6% revenue decline in 2024, bringing its total to $3.7 billion [3].

Corporate technology departments actively reduce their vendor counts. Nine hundred technology buyers named equal experience for remote and in-office staff as their primary procurement criterion in a 2024 Gartner survey [5]. This demand for operational parity outranked both cost optimization and vendor consolidation priorities. Organizations integrate voice systems directly into project management and productivity tools to maintain constant employee connectivity. Gartner predicts that 90% of global organizations will run enterprise telephony through cloud platforms by 2028 [6]. This reflects a severe market shift from 30% adoption in 2025 [6]. Precedence Research calculates the total addressable market will expand to $494.9 billion by 2035 [7].

Hardware sales decline as software subscriptions capture IT budgets. Internet protocol desk phone revenues dropped 22.8% in recent market cycles, reducing the hardware category to $1.9 billion [8]. Conversely, hosted voice revenues increased 21.2% to reach $16.4 billion [8]. Buyers migrate away from physical infrastructure because on-premises private branch exchange systems require specialized maintenance personnel. Cloud providers automate security patches and feature updates across global deployments. This transition forces traditional hardware manufacturers to build software integrations or risk complete obsolescence.

Buying fewer software products frequently increases corporate spending if overlapping contracts remain active. Subscription sprawl occurs when isolated business units bypass technology approvals to purchase redundant communication applications. Finance teams struggle to forecast operating expenses due to consumption pricing models. Modern pricing structures combine base user licenses with feature add-ons and international toll rates. Companies routinely pay for inactive accounts long after employee departures. These ghost services artificially inflate monthly operating expenses without providing business value.

Weak expense oversight damages company valuations. Unmanaged telecommunications spending obscures actual operating costs for private equity firms auditing portfolio operations [9]. Proper expense centralization reduces structural connectivity costs by 10% to 30% [9]. Financial analysts track contact center applications closely because these tools introduce extreme usage volatility. High-volume call environments generate unpredictable toll charges during peak demand seasons. Finance departments require automated expense management software to audit monthly invoices against actual active user directories.

System downtime further compounds these financial leaks. Service inconsistencies and platform outages cost businesses $850 per employee annually [10]. Physical hardware maintenance drains capital budgets. Migrating to unified communications as a service platforms saves companies approximately $1,200 per user annually on physical network maintenance [10]. Cloud infrastructure allows network engineers to provision new geographic locations in minutes rather than weeks. This deployment speed accelerates merger integrations and standardizes corporate technology standards across newly acquired subsidiaries.

State and federal agencies strictly regulate telecommunications traffic. Telecom taxes and fees reached an average of 27.6% of monthly wireless bills in 2025 [11]. Certain jurisdictions impose localized surcharges exceeding 36%. These taxation variables require automated calculation tools to prevent serious audit liabilities. Service providers operating without certified tax automation engines routinely miscalculate regional tariffs. This negligence leaves end-user organizations responsible for retroactive tax payments and subsequent financial penalties.

Federal Communications Commission mandates enforce strict call authentication standards. The STIR/SHAKEN framework requires voice service providers to obtain cryptographic certificates to verify caller identities [11]. These rules took effect in September 2025. Mobile carriers also implemented mandatory 10-digit long code registration for business text messaging in February 2025 [11]. Carriers immediately block unregistered messaging traffic. This operational block paralyzes sales departments attempting to contact prospective clients via text message.

Compliance burdens disproportionately affect industries relying on high-volume outbound communication. Unregistered campaigns trigger automatic carrier blocks for staffing agencies managing outbound call volume. Platform architectures dictate compliance capabilities. Regulated organizations require end-to-end encryption, secure call recording, and strict data retention policies built directly into the software code [12]. Legal departments mandate administrative access controls to prevent unauthorized data extraction. Financial institutions require platforms capable of storing communication logs in compliant cloud servers for designated retention periods.

Administrators manage 26 million Microsoft Teams Phone users as of early 2026 [12]. Cisco Webex Calling supports 18 million users, and Zoom Phone exceeds 10 million seats [12]. Despite Microsoft's market dominance, organizations rarely deploy a single platform exclusively. Employees use Microsoft Teams as the primary interface for daily chat and internal video meetings. IT departments frequently route the actual voice traffic through backend enterprise telephony platforms like RingCentral or Zoom [13]. This dual-layer architecture provides advanced call routing and reliability without disrupting the familiar employee interface.

Mobile integration drives productivity gains for distributed teams. A 2024 Forrester Consulting study found that native mobile calling integration yields a 20% productivity increase per user annually [14]. Retiring redundant physical phone lines generates cost savings ranging from $1.6 million to $3.3 million over three years for large enterprises [14]. Mobile applications must support cellular data handoffs without dropping active voice sessions. Reliable mobile connectivity allows commercial contractors coordinating field personnel to maintain centralized communication records regardless of employee location.

Hardware compatibility dictates successful deployment strategies. Enterprise meeting rooms require specialized video conferencing equipment certified for specific cloud platforms. Purchasing uncertified hardware forces technicians into complex manual configurations. Leading vendors offer certified device programs to guarantee audio quality and network stability. Open application programming interfaces allow independent software vendors to build custom workflow integrations. These technical connections prevent employees from manually switching between browser tabs to access customer data during live phone calls.

Thirty-three percent of market growth between 2025 and 2029 will originate from integrated customer engagement solutions [2]. Software vendors embed artificial intelligence models directly into call routing and transcription services. Generative models execute meeting summaries and extract action items from video transcripts. Zoom reported that its AI Companion feature served as the primary growth driver for its fiscal 2025 transformation [4]. The company intends to shift these tools toward independent capabilities that complete administrative tasks without human supervision.

Sales and support personnel waste hours manually updating customer records. Automation tools extract intent, competitor mentions, and objection data from live calls and push this structured data into Salesforce or HubSpot [13]. Artificial intelligence handles 95% of initial candidate screening interactions for specialized recruitment firms [15]. Voice analysis technology predicts success metrics and minimizes hiring biases for human resources departments [15]. Predictive algorithms analyze network packet loss to identify potential audio degradation before users experience dropped calls.

Information security professionals monitor artificial intelligence deployments closely. Transmitting sensitive corporate discussions to third-party language models introduces severe data privacy risks. Vendors must provide enterprise-grade models that process data within isolated cloud tenants. Administrators require granular control panels to disable artificial intelligence features for specific departments handling classified information. Microsoft 365 Copilot processes internal data without exposing proprietary information to public training sets. This architectural isolation secures confidential legal and financial communications.

Workplace experience correlates directly with employee retention. Replacing an employee costs between 50% and 200% of their annual salary due to lost output and disrupted client relationships [16]. Employees who report satisfaction with their digital workspace are three times more likely to remain with their employer [16]. Frustrating technology tools damage corporate morale and accelerate voluntary turnover rates. Human resources directors monitor software adoption metrics to identify departments struggling with communication bottlenecks.

Consolidated platforms accelerate onboarding timelines for new hires. Training employees on a single interface requires less administrative overhead than managing separate credentials for video, phone, and messaging applications. The Society for Human Resource Management provides specific operational ratios for staffing. Organizations require one human resources representative for every 100 employees in mid-market environments [17]. Technology automation allows lean human resources teams to support larger employee populations without adding headcount.

Analytics dashboards provide operational visibility into workforce habits. Administrators track active meeting minutes, file sharing frequency, and message volume across departments. These metrics highlight collaboration patterns and identify isolated teams. Real-time data feeds allow managers to adjust staffing schedules based on actual communication volume rather than historical estimates. Support leaders monitor agent status indicators to route urgent client inquiries to available personnel immediately. This operational visibility prevents customer service delays during peak contact periods.

Omdia values the specific unified communications market segment at $33.4 billion, predicting a moderate 1.1% compound annual growth rate through 2029 [18]. Market definitions blend as internal collaboration software merges with external contact center applications. Communications platform as a service segments provide application programming interfaces to embed messaging directly into consumer applications. This specific platform segment reached $16.7 billion in 2024 and expands at a 9.3% annual rate [2]. Developers use these toolkits to build custom notification systems for specialized industry requirements.

Legacy telephony providers form strategic alliances with cloud specialists to survive. Mitel partnered with RingCentral and Zoom to maintain market relevance as physical hardware sales decline [18]. Avaya executes similar cloud partnership strategies. These corporate integrations signal terminal decline for isolated on-premises communication architectures. Organizations evaluating communication vendors must prioritize data privacy, mobile accessibility, and integration architecture over basic feature lists.

Telecommunications strategy requires coordination between finance, security, and operations departments. Isolated software purchasing creates severe network vulnerabilities and financial waste. Enterprise architecture teams must design communication networks capable of supporting artificial intelligence workloads securely. Future market leaders will deliver platforms that process external customer inquiries and internal employee collaboration through a single, compliant data architecture. This convergence eliminates data silos and provides immediate operational context for every business interaction.

| Year | Microsoft Teams DAU | Zoom DAU |

|---|---|---|

| 2020 | 20 | 300 |

| 2021 | 75 | 300 |

| 2022 | 145 | 300 |

| 2023 | 270 | 300 |

| 2024 | 320 | 300 |

This trend tracks the daily active users (DAU) of two major UCaaS platforms, Microsoft Teams and Zoom, between the years 2020 and 2024 [1]. It illustrates that while Zoom experienced an immediate explosion to 300 million DAU during the initial pandemic shift and plateaued, Microsoft Teams exhibited sustained, compounding growth from 20 million to 320 million DAU, ultimately surpassing Zoom's daily active user count [2].

At a micro level, this data means individual organizations are increasingly migrating away from fragmented communication tech stacks in favor of centralized platforms. Companies are finding substantially more value in systems that natively bundle chat, voice, video, and document collaboration into a single, cohesive interface. On a macro industry level, this signifies a structural shift in the UCaaS market toward enterprise-wide ecosystems, heavily favoring tech giants that already own the broader productivity suite [3]. Consequently, standalone communication applications are being forced to pivot their strategies, often emphasizing external communications, API flexibility, or specialized AI features to maintain relevance against these bundled mega-platforms [4].

This evolution is critical because it dictates how billions of dollars in enterprise IT budgets are allocated across the globe. The convergence of UCaaS with broader productivity and artificial intelligence tools means software lock-in is becoming stronger, making it significantly harder and more expensive for companies to switch providers once they are fully embedded [5]. Furthermore, it highlights the fundamentally changing nature of modern work, where seamless internal collaboration, workflow automation, and persistent workspaces are prioritized over simple, ad-hoc video meeting capabilities [6].

The initial catalyst for both platforms was undeniably the sudden global shift to remote work, which rapidly inflated the user bases of all cloud communication platforms almost overnight. However, Microsoft Teams' sustained and superior growth can largely be attributed to its strategic bundling within the Microsoft 365 suite, effectively making it a cost-free or default option for millions of enterprise users who already utilize Microsoft products [7]. Additionally, the deep integration of next-generation AI-powered tools, such as Microsoft Copilot, has created a powerful productivity loop that keeps users engaged within a single ecosystem rather than switching contexts to external applications [8]. Finally, as organizations moved past the emergency deployment phase of remote work, IT leaders likely sought to consolidate enterprise software spending, naturally favoring comprehensive, all-in-one platforms over paying premium licensing fees for separate, disparate communication tools [9].

The trajectory of Microsoft Teams' DAU compared to Zoom reveals a maturing UCaaS market that heavily rewards bundled, deeply integrated enterprise ecosystems over niche or standalone video solutions. As artificial intelligence continues to be woven into the fabric of these platforms, the technical and financial barrier to entry for new challengers will only grow steeper. The prominent takeaway is that the future of UCaaS lies not merely in facilitating communication, but in serving as the centralized, automated nervous system for the entire digital workplace.