Mini article

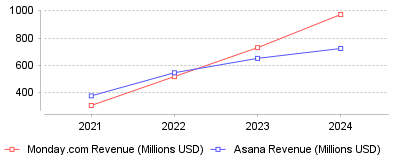

| Year | Monday.com Revenue (Millions USD) | Asana Revenue (Millions USD) |

|---|---|---|

| 2021 | 308 | 378 |

| 2022 | 519 | 547 |

| 2023 | 730 | 652 |

| 2024 | 972 | 724 |

The data visualizes a dramatic reversal of fortunes between two industry giants, effectively illustrating the market's shift in preference. In 2021, Asana held a comfortable lead with $378 million in revenue compared to Monday.com's $308 million [1] [2]. However, by the close of 2024, Monday.com not only erased that gap but surged ahead to $972 million, while Asana trailed at $724 million [3] [4]. This represents a "crossover" point where the challenger’s growth velocity (approx. 33% YoY) significantly outpaced the incumbent’s stabilization (approx. 11% YoY).

This trend signifies a macro shift from "task management" to "Work Operating Systems" (WorkOS). Buyers are no longer looking for standalone punch list or task tracking tools; they are seeking consolidated platforms that can replace multiple software subscriptions. Asana has maintained a focus on being a premier, high-design project management tool for knowledge workers [5]. In contrast, Monday.com pivoted to a "multi-product" strategy, explicitly launching separate vertical products for CRM (Sales), Development, and Service management [3]. The market has rewarded the latter approach, indicating that in a tighter economic environment, businesses prefer adaptable, "all-in-one" ecosystems over specialized best-of-breed tools.

For users and investors, this trend highlights the importance of "efficiency" and "scalability" over pure features. It suggests that the future of this category lies in flexibility—tools that allow a construction manager to handle a punch list in the same ecosystem where the sales team tracks bids. Furthermore, Monday.com’s ability to achieve profitability while growing faster suggests that the "growth at all costs" model is dead; reliable, profitable platforms are becoming the standard for enterprise adoption [5].

The divergence was likely driven by Monday.com's aggressive expansion into adjacent markets (CRM and Dev tools) which unlocked budgets outside of traditional IT or Project Management departments [5]. Conversely, Asana’s strategy focused heavily on the "Work Graph" and AI integration within the core project management interface, which, while innovative, did not open up entirely new budget pools as quickly [6]. Additionally, the broader economic downturn in 2022-2023 forced companies to consolidate vendors, favoring platforms that could kill two birds (e.g., PM and CRM) with one stone.

The data indicates a clear winner in the current cycle of the Task Management evolution: the multi-product platform. The crossover in revenue between Monday.com and Asana proves that flexibility and vendor consolidation are currently more valuable to the market than specialized depth. For decision-makers, this suggests that selecting a tool capable of spanning multiple departments (Sales, Dev, Ops) is a safer long-term bet than buying niche point solutions.

Construction rework costs the U.S. industry over $65 billion annually [1]. This figure, representing approximately 5% of total construction spending, drives the aggressive adoption of digital task management and punch list software. General contractors and specialty trades no longer view these tools as optional administrative conveniences but as essential risk mitigation assets. The global task management software market, valued at $4.45 billion in 2024, is projected to reach $5.14 billion by 2025, growing at a CAGR of 15.4% [2]. Within the construction sector specifically, the punch list software segment is rapidly maturing, with valuations estimated between $600 million and $680 million in 2025 [3].

Capital efficiency now dictates software procurement strategies. With interest rates squeezing margins throughout 2023 and 2024, firms prioritize task and punch list management tools that offer direct ROI through rework reduction and accelerated closeout times. The operational focus has shifted from simple digitization—moving paper checklists to tablets—to intelligent execution, where field data directly influences payment cycles and liability defense.

Procore Technologies signaled a distinct shift in operational expectations during its Groundbreak conference in November 2024. The company introduced "Procore Agents," an artificial intelligence framework designed to automate routine workflows rather than simply recording them [4]. These agents handle tasks such as managing RFIs (Requests for Information) and scheduling, actively flagging risks before they become schedule delays. This moves the category beyond passive project management platforms into active project intervention.

Autodesk followed a similar trajectory with the beta release of "Autodesk Assistant" within the Autodesk Construction Cloud. This tool allows users to query specification documents using natural language, reducing the time project engineers spend searching for installation requirements [5]. The operational implication is immediate: field teams can verify compliance in real-time without returning to the trailer, directly attacking the communication gaps that cause 52% of rework [1].

Adoption rates for these advanced features vary by firm size. While large general contractors pilot AI-driven scheduling, mid-market trade partners often struggle with basic data discipline. The challenge for 2025 lies not in the technology's capability but in the field adoption curve. Software vendors now pitch "predictive" capabilities, but these features require structured data input that many job sites still lack.

Defect management remains the primary operational use case for punch list tools. Rework erodes 5% to 20% of contract value depending on project complexity [6]. Visual documentation has emerged as the standard of care for mitigating these costs. Modern platforms now require photo evidence for task completion, creating an immutable record of work in place.

Specialized trades face unique documentation burdens. Task management tools for roofing companies must now integrate drone imagery and satellite measurements. Manual inspections are becoming obsolete as drones reduce inspection times by up to 75% while keeping adjusters and estimators safely on the ground [7]. The operational workflow has evolved: a drone captures the site, software generates an automated deficiency map, and the project manager assigns punch list items to specific crews before the inspection drone even lands.

Plumbing contractors face similar pressure regarding concealed work. Leaks remain a leading cause of loss in construction, with non-weather water damage costing the industry $16 billion annually [8]. Insurers increasingly demand photo documentation of pressure tests and firestop installations before walls are closed. Consequently, task management tools for plumbers are evolving into compliance repositories. Fieldwire and similar platforms report that structured data collection—forcing a photo upload before a task can be marked "complete"—reduces rework by 18% [9].

Payment delays cost the construction industry $280 billion in 2024 [10]. This inefficiency stems largely from the disconnect between field progress and back-office billing. General contractors often withhold payment until punch list items are verified, yet the verification process remains disjointed from the payment application.

Autodesk's acquisition of Payapps in January 2024 addresses this friction point directly [11]. By embedding payment applications within the project management environment, the software links task completion to line-item requisitions. This integration forces a shift in operations: field superintendents must maintain real-time punch list hygiene to ensure subcontractor liquidity. 82% of contractors reported payment delays exceeding 30 days in 2024, up from 49% two years prior [10]. Tools that fail to bridge the gap between "work done" and "invoice approved" will likely lose market share to integrated platforms.

Federal regulations effective January 1, 2024, have forced digital adoption among firms that previously relied on paper logs. The Occupational Safety and Health Administration (OSHA) now requires construction employers with 100 or more employees to electronically submit detailed injury and illness data (Forms 300 and 301) annually [12]. This mandate pushes firms to adopt task management tools for contractors that include safety modules.

The operational burden of manual data entry for these federal reports is significant. Platforms like Raken and HammerTech have expanded their offerings to automate this reporting, transforming safety observations into compliance data points [13]. The punch list has thus expanded beyond quality control to include safety hazards. A loose guardrail is no longer just a task to fix; it is a potential data point in a federal database. This transparency raises the stakes for documentation accuracy.

Digitization introduces new vulnerabilities. Ransomware attacks against the construction sector increased by 41% between late 2023 and late 2024 [14]. Construction firms often lack the sophisticated IT infrastructure of financial or healthcare organizations, making them attractive targets. As task management tools move to the cloud and integrate with financial systems, they become vectors for cyber extortion.

Credential exposure now accounts for 75% of digital risk alerts in the sector [14]. Field staff often share login credentials for tablet-based punch list apps, creating security gaps. Operational protocols must evolve to enforce multi-factor authentication (MFA) and single sign-on (SSO) even for transient subcontractors. The cost of a breach extends beyond the ransom; project shutdowns and data loss can trigger liquidated damages clauses in owner contracts.

The construction industry faces a chronic labor shortfall, with 94% of firms reporting open positions for craft workers in 2024 [15]. This shortage directly impacts task management strategies. Firms cannot rely on experienced foremen to catch every detail; there simply aren't enough of them. Punch list software acts as a force multiplier, allowing a single superintendent to oversee quality across larger areas through digital delegation.

FMI’s 2023 Labor Productivity Study indicates that 45% of contractors saw declining labor productivity over the prior 12 to 18 months [16]. Poor planning and communication are cited as top internal factors dragging down efficiency. The trend for 2025 involves using task data to benchmark sub-trade performance. General contractors now analyze punch list density—the number of defects per square foot—to evaluate subcontractors for future bids. This data-driven vetting process penalizes trades that consistently fail to self-correct.

The convergence of project management, financial controls, and field execution tools will accelerate through 2025. Standalone punch list apps will likely be absorbed by broader platforms or forced to specialize deeply in vertical niches like heavy civil or industrial construction. AI agents will move from novelty to necessity as the volume of project data exceeds human processing capacity.

We expect to see insurers play a more active role in software mandates. Just as telematics became standard for fleet insurance, verifiable digital punch list history may soon become a prerequisite for favorable General Liability rates. For the industry analyst, the key metric to watch is not just software adoption, but the "time to close"—the speed at which a digital punch item translates into an approved invoice. In a high-interest environment, speed is the only metric that matters.

Mini article

| Year | Monday.com Revenue (Millions USD) | Asana Revenue (Millions USD) |

|---|---|---|

| 2021 | 308 | 378 |

| 2022 | 519 | 547 |

| 2023 | 730 | 652 |

| 2024 | 972 | 724 |

The data visualizes a dramatic reversal of fortunes between two industry giants, effectively illustrating the market's shift in preference. In 2021, Asana held a comfortable lead with $378 million in revenue compared to Monday.com's $308 million [1] [2]. However, by the close of 2024, Monday.com not only erased that gap but surged ahead to $972 million, while Asana trailed at $724 million [3] [4]. This represents a "crossover" point where the challenger’s growth velocity (approx. 33% YoY) significantly outpaced the incumbent’s stabilization (approx. 11% YoY).

This trend signifies a macro shift from "task management" to "Work Operating Systems" (WorkOS). Buyers are no longer looking for standalone punch list or task tracking tools; they are seeking consolidated platforms that can replace multiple software subscriptions. Asana has maintained a focus on being a premier, high-design project management tool for knowledge workers [5]. In contrast, Monday.com pivoted to a "multi-product" strategy, explicitly launching separate vertical products for CRM (Sales), Development, and Service management [3]. The market has rewarded the latter approach, indicating that in a tighter economic environment, businesses prefer adaptable, "all-in-one" ecosystems over specialized best-of-breed tools.

For users and investors, this trend highlights the importance of "efficiency" and "scalability" over pure features. It suggests that the future of this category lies in flexibility—tools that allow a construction manager to handle a punch list in the same ecosystem where the sales team tracks bids. Furthermore, Monday.com’s ability to achieve profitability while growing faster suggests that the "growth at all costs" model is dead; reliable, profitable platforms are becoming the standard for enterprise adoption [5].

The divergence was likely driven by Monday.com's aggressive expansion into adjacent markets (CRM and Dev tools) which unlocked budgets outside of traditional IT or Project Management departments [5]. Conversely, Asana’s strategy focused heavily on the "Work Graph" and AI integration within the core project management interface, which, while innovative, did not open up entirely new budget pools as quickly [6]. Additionally, the broader economic downturn in 2022-2023 forced companies to consolidate vendors, favoring platforms that could kill two birds (e.g., PM and CRM) with one stone.

The data indicates a clear winner in the current cycle of the Task Management evolution: the multi-product platform. The crossover in revenue between Monday.com and Asana proves that flexibility and vendor consolidation are currently more valuable to the market than specialized depth. For decision-makers, this suggests that selecting a tool capable of spanning multiple departments (Sales, Dev, Ops) is a safer long-term bet than buying niche point solutions.