| Year | Revenue USD Millions |

|---|---|

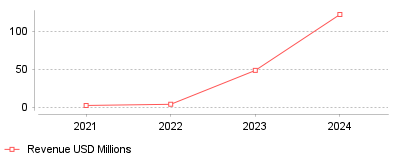

| 2021 | 3 |

| 2022 | 4.5 |

| 2023 | 48.7 |

| 2024 | 121.6 |

The data demonstrates an exponential surge in both the overarching AI video generation market and the specific commercial success of AI motion graphics platforms like Runway ML. Between 2021 and 2024, Runway ML's revenue catapulted from $3 million to over $121 million, mirroring the broader market's expansion to a $6.2 billion valuation by 2025 [1][2].

On a micro level, this indicates that motion graphics professionals and small creative teams are rapidly transitioning away from exclusively traditional workflows. Tools that automate highly manual tasks, such as rotoscoping, are dramatically reducing production times, allowing single artists or small studios to output high-fidelity visual effects that previously required large teams [3]. On a macro level, the software industry is experiencing a massive reallocation of capital and enterprise spending toward generative AI solutions. Software vendors that fail to integrate AI-assisted rendering, style transfer, or text-to-video capabilities risk obsolescence as consumer expectations for speed and cost-efficiency evolve [4].

This trend is democratizing high-end animation and motion graphics, significantly lowering the barrier to entry for content creators, marketers, and independent filmmakers. Traditional barriers, such as the high cost of rendering farms and the steep learning curves of legacy software, are being bypassed by intuitive text-to-video and image-to-video models [5]. Consequently, the global digital video and animation economy is scaling at an unprecedented rate, opening up new creative possibilities and disrupting traditional agency models that rely on high-cost, time-intensive production cycles [6].

A primary catalyst for this shift is the rapid advancement of multimodal foundation models and large language models, which have finally reached a threshold of visual fidelity acceptable for commercial use. Furthermore, aggressive venture capital investment has allowed startups to subsidize the immense cloud-computing costs associated with training these models, making them surprisingly affordable for end-users [3]. The shift to remote work and distributed digital marketing teams over the last few years likely accelerated the demand for faster, cloud-based content creation pipelines. Finally, one can speculate that the intense algorithmic demand for continuous, high-volume video content on platforms like TikTok and YouTube Shorts forced creators to seek automation tools simply to keep pace with algorithmic expectations [7].

The animation and motion graphics software category has permanently entered the AI-driven era, with generative tools proving to be viable commercial solutions rather than just experimental novelties. As market leaders continue to experience triple-digit revenue growth, we can expect AI features to become the default standard in all creative software suites. The prominent takeaway is that adopting AI motion graphics tools is no longer a competitive advantage, but a fundamental requirement for survival in the modern video production industry.

Vendors recorded massive revenue gains across media production segments in late 2024. The global animation software market reached $141.63 billion in 2023 [1]. Projections push that valuation to $182.42 billion by 2030 [1]. North America controls the largest regional segment with a 37.7% revenue share [1]. Three-dimensional products hold 45% of that global market [1]. This capital influx masks deep operational friction. Studios face rising compute costs. Labor unions demand strict production rules. Automated models break traditional rendering pipelines.

Financial disclosures reveal specific segment performance among major suppliers. Autodesk reported fourth-quarter fiscal 2025 revenue of $1.64 billion [2]. The company saw media and entertainment revenue hit $84 million during that period [3]. Autodesk drives 97% of its total revenue from recurring subscriptions [3]. A new transaction model contributed $46 million to fourth-quarter revenue, shifting buyer commitments toward annual billing cycles [4]. Direct revenue increased 35% in constant currency during that timeframe [4].

Hardware suppliers extract equal value from visual effects houses. Nvidia posted $511 million in professional visualization revenue for the fourth quarter of fiscal 2025 [5]. That figure represents a 10% year-over-year increase [5]. Annual revenue for that division rose 21% to $1.9 billion [5]. Nvidia expanded its Omniverse integration to handle robotics and autonomous vehicle data, pulling enterprise graphics software into heavy industrial applications [5]. Buyers struggle to align these expensive platform licenses with tightening project budgets.

Artificial intelligence features increase total production costs before they yield savings. Adobe integrated video generation into Premiere Pro in late 2024 [6]. The Firefly model allows editors to extend clips and generate secondary footage directly on the timeline [7]. Resolution caps at 1080p for five-second intervals [8]. Generative Extend handles audio adjustments by creating artificial room tone to mask dead audio space [8]. Users generated 13 billion images using Firefly between March 2023 and October 2024 [7]. Directors integrate applications featuring generated media into standard timelines to accelerate delivery. This processing scale requires vast server resources.

McKinsey researchers surveyed 1,993 companies regarding artificial intelligence performance [9]. Only 5.5% of respondents attributed significant financial value to these implementations [9]. High performers dedicate at least 20% of their digital budgets to artificial intelligence [9]. Product development teams resist autonomous operations. Data shows 73% of engineering respondents avoid autonomous agents entirely [9]. Automated platforms require high initial capital. Organizations deploy these capabilities within marketing and sales departments first. Reported adoption in those units doubled between 2023 and 2024 [10]. Corporate videographers deploy software designed for marketing departments when facing strict procurement limits.

Forrester data shows 67% of technology leaders plan to increase artificial intelligence investments over the next year [11]. The global market for generative models in media reached $1.97 billion in 2024 [12]. Analysts project that figure will climb to $6.48 billion by 2029 [12]. Despite the spending surge, software reliability remains poor. Researchers at the Tow Center for Digital Journalism found top models failed 60% of assigned queries [13]. Carnegie Mellon tested enterprise agents against 175 standard corporate tasks. Top models completed only 24% of those tasks autonomously [13]. When researchers added complex parameters, failure rates spiked past 70% [13].

Union agreements dictate how studios deploy rendering software. The Animation Guild ratified a critical three-year contract in December 2024 [14]. Approval reached 76.1% among voting members [14]. The agreement guarantees a 7% wage increase in the first year [14]. Subsequent years mandate 4% and 3.5% base increases [14]. Employers must fund these higher labor costs while simultaneously paying elevated software licensing fees.

The Bureau of Labor Statistics tracks 12,280 special effects artists working directly in motion picture industries [15]. The median annual wage for this occupation was $99,800 in May 2024 [16]. Income distribution reveals sharp disparities. The lowest decile earns less than $57,220, while the highest decile earns over $174,630 [16]. Job growth projections sit at a minimal 2% through 2034 [16]. Federal economists expect 5,000 industry openings annually [16]. Industry advocates commission studies highlighting severe disruption risks. One report estimated 62,000 entertainment jobs could face elimination due to automated rendering tools within three years [17]. Guild negotiators forced studios to accept written notification requirements whenever productions use automated generators [14].

These labor dynamics influence enterprise software procurement. Operations directors procure motion design platforms that comply with union mandates. Contracts forbid studios from training proprietary models on union-created assets without strict permissions. The 2024 Guild agreement increased specific pension premiums from $12.37 per hour to $14.02 per hour [18]. Required CSATF contributions rose from $0.10 to $0.63 per hour [18]. Pay for on-call employees working a seventh day increased to twice their weekly prorated rate [18]. Health plan costs rise alongside base wages. Directors offset these expenses by adopting automated post-production features. Producers use machine algorithms to dub international releases and clip footage libraries [19]. McKinsey forecasts that $10 billion of domestic original content spend will intersect with automated workflows by 2030 [19].

Epic Games dominates virtual production environments. Unreal Engine usage reached 28% across relevant professional markets in 2024 [20]. Perforce surveyed technology leaders regarding engine adoption. Results showed 14% use game engines for industrial visualization [21]. Another 12% apply these platforms directly in television production [21]. Wētā FX used Unreal Engine to produce the Academy Award-winning animated short film War Is Over! [22]. Production teams used the exact same software to map sun patterns during the desert filming of Dune: Part Two [22]. Real-time rendering eliminates costly post-production delays. Directors adjust lighting and camera angles instantly on LED volume sets.

The global virtual production market exceeded $3.5 billion in 2024 [23]. Live-action series require massive server infrastructure. Medical institutions use identical software to build surgical simulators [24]. Medical instructors evaluate tools for visualizing educational data before purchasing enterprise licenses. This cross-industry demand alters product development roadmaps. Unity holds a 53% adoption rate among surveyed development leaders [21]. Godot continues to gain traction rapidly. Its usage reached 21% in automotive and manufacturing sectors by early 2025 [21].

Software vendors release updates targeting physical environment simulation. Independent creators utilize preset-driven timeline editors to bypass custom modeling steps. High-end workstations handle local rendering, but complex physics simulations force studios onto external servers. Infrastructure availability determines project completion speeds. Small studios cannot buy outright hardware upgrades to match iteration cycles. They must rent capacity from central cloud providers.

Amazon Web Services charges strict fees for external rendering. Studios use AWS Deadline Cloud to manage massive frame sequences. A single hour of server rendering across multiple nodes costs between $50 and $200 [25]. Spot instance pricing fluctuates based on server demand [26]. If supply drops, Amazon bills the higher rate for subsequent compute hours [26]. Financial unpredictability hurts independent production houses. Freelancers seek cheaper alternatives like RunPod or Paperspace to avoid enterprise markup [25].

Software licensing complicates remote infrastructure deployment. Operators must purchase specific usage-based licenses for applications like Autodesk Maya or Foundry Nuke [26]. Studios pay for the base server instance, the storage volume, and the software license simultaneously. Amazon bills customers based on fleet type, instance size, and exact job duration [26]. A benchmark test rendering 400 frames on standard AWS spot instances generated a $176.60 bill [26]. Rendering 600 frames using a hybrid on-premises approach cost $91.78 [26]. Technical directors spend considerable time configuring gateway nodes and tracking data transfer fees.

Mismanaged cloud resources drain production accounts rapidly. Artists occasionally leave server instances running after tasks finish. Amazon bills continuously until operators terminate the virtual machines [27]. Small studios report losing thousands of dollars on single projects due to improper resource tracking [27]. Technical barriers prevent many designers from scaling their work. The market requires simplified burst rendering options that connect local workstations to external servers without command-line configuration. The base gateway node handles resource routing for $0.60 per hour, adding baseline overhead before any actual rendering begins [27].

Gartner tracks vendor performance in the content creation sector. Sitecore, Sprinklr, and Adobe operate as dominant providers [28]. Sprinklr achieved Leader status in the 2024 Magic Quadrant for Content Marketing Platforms [29]. Brands demand platforms that unify campaign execution with asset performance analysis. Traditional formats face severe competition. Static white papers generate less engagement than interactive videos and social graphics [28].

Salesforce added localized intelligence tools to its multichannel marketing hub [30]. Automation algorithms adjust timing and format based on audience segment data [30]. Content management systems require heavy databases to track iteration histories. Media managers test operating models using these centralized hubs. B2B organizations deploy solutions like Upland Kapost to distribute complex visual assets [31]. Brands measure success by tracking return on marketing investment through integrated dashboards.

Security protocols remain weak across new visual tools. Generative outputs contain hidden flaws. Veracode tested 80 corporate tasks across multiple programming languages and found high failure rates [13]. Exactly 45% of generated code introduced Open Worldwide Application Security Project vulnerabilities [13]. Language performance varied widely. Java tasks achieved only a 28.5% security pass rate [13]. Python fared better at 55.3%, while JavaScript hit 61.7% [13]. Forrester analysts warn that visual generation software creates new false positive risks during incident response [13]. A mapping application confidently placed shark attacks in landlocked Wyoming [13]. Companies must audit generated media before public distribution. Legal departments flag copyright vulnerabilities when vendors train models on unauthorized digital assets [11].

Production spending faces a slight contraction. Analysts project a 2% annual decline in original content expenditure over the next five years [19]. Buyers redirect capital toward live sports programming and licensed catalogs [19]. The United States accounts for $101 billion of the $180 billion global content spend [19]. Distributors capture maximum margin by forcing production studios to absorb technology overhead. Large software vendors adapt by transitioning customers to consumption-based billing.

Autodesk focuses entirely on securing multi-year enterprise contracts. The company reported $1.2 billion in design segment revenue during the fourth quarter of 2024 [32]. Deferred revenue decreased 7% to $4.3 billion due to the intentional transition from upfront to annual billing structures [33]. By early 2025, total subscription counts reached 7.79 million users [3]. This platform consolidation limits the negotiating power of individual studios. Animation directors face a market where core applications like Maya and 3ds Max remain indispensable but increasingly expensive to maintain across entire departments.

Hardware constraints dictate rendering timelines. Nvidia expects data center expansion to drive future growth. The company reported $35.58 billion in quarterly data center revenue for Q4 2025 [34]. Compute revenue alone hit $32.5 billion, representing a 116% increase from the prior year [34]. Blackwell architecture deployment accelerates processing capabilities for complex physical environments. Visual artists rely on these local GPU units to calculate light refraction and motion blur. Independent creators without local hardware must pay cloud premiums or face rendering bottlenecks. The technical capabilities of motion graphics software far exceed the financial resources of average users.

| Year | Revenue USD Millions |

|---|---|

| 2021 | 3 |

| 2022 | 4.5 |

| 2023 | 48.7 |

| 2024 | 121.6 |

The data demonstrates an exponential surge in both the overarching AI video generation market and the specific commercial success of AI motion graphics platforms like Runway ML. Between 2021 and 2024, Runway ML's revenue catapulted from $3 million to over $121 million, mirroring the broader market's expansion to a $6.2 billion valuation by 2025 [1][2].

On a micro level, this indicates that motion graphics professionals and small creative teams are rapidly transitioning away from exclusively traditional workflows. Tools that automate highly manual tasks, such as rotoscoping, are dramatically reducing production times, allowing single artists or small studios to output high-fidelity visual effects that previously required large teams [3]. On a macro level, the software industry is experiencing a massive reallocation of capital and enterprise spending toward generative AI solutions. Software vendors that fail to integrate AI-assisted rendering, style transfer, or text-to-video capabilities risk obsolescence as consumer expectations for speed and cost-efficiency evolve [4].

This trend is democratizing high-end animation and motion graphics, significantly lowering the barrier to entry for content creators, marketers, and independent filmmakers. Traditional barriers, such as the high cost of rendering farms and the steep learning curves of legacy software, are being bypassed by intuitive text-to-video and image-to-video models [5]. Consequently, the global digital video and animation economy is scaling at an unprecedented rate, opening up new creative possibilities and disrupting traditional agency models that rely on high-cost, time-intensive production cycles [6].

A primary catalyst for this shift is the rapid advancement of multimodal foundation models and large language models, which have finally reached a threshold of visual fidelity acceptable for commercial use. Furthermore, aggressive venture capital investment has allowed startups to subsidize the immense cloud-computing costs associated with training these models, making them surprisingly affordable for end-users [3]. The shift to remote work and distributed digital marketing teams over the last few years likely accelerated the demand for faster, cloud-based content creation pipelines. Finally, one can speculate that the intense algorithmic demand for continuous, high-volume video content on platforms like TikTok and YouTube Shorts forced creators to seek automation tools simply to keep pace with algorithmic expectations [7].

The animation and motion graphics software category has permanently entered the AI-driven era, with generative tools proving to be viable commercial solutions rather than just experimental novelties. As market leaders continue to experience triple-digit revenue growth, we can expect AI features to become the default standard in all creative software suites. The prominent takeaway is that adopting AI motion graphics tools is no longer a competitive advantage, but a fundamental requirement for survival in the modern video production industry.