| Year | Average App Count |

|---|---|

| 2022 | 130 |

| 2023 | 112 |

| 2024 | 106 |

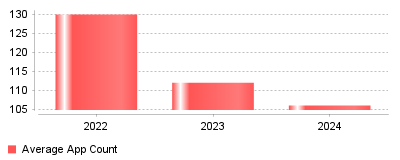

For the first time in the history of the "SaaS explosion," the sheer volume of applications within corporate tech stacks is shrinking. Data from 2024 indicates that the average number of SaaS applications per company dropped to 106, a continued decline from the peak of 130 applications recorded in 2022 [1] [2]. However, this contraction in volume has not resulted in cheaper IT budgets; conversely, the average SaaS spend per employee surged by nearly 22% in the last year, reaching $4,830 [3] [4].

This trend signifies a maturation of the market where "SaaS Sprawl" is no longer being ignored but actively managed through aggressive consolidation strategies. On a micro level, IT departments are eliminating redundant tools—such as having Trello, Asana, and Monday.com all active within one organization—and standardizing on single platforms to reduce complexity [5]. On a macro level, this represents a pivot toward "SaaS value realization," where companies are willing to pay more for fewer, more powerful tools. The rise in spend despite the drop in app count suggests that vendors are successfully shifting their revenue models from simple seat-based pricing to consumption-based models, often driven by new AI features that command premium fees [6].

This shift is critical because it fundamentally changes the mandate of IT Asset Management (ITAM) platforms from simple discovery to complex cost control. With 53% of SaaS licenses reportedly inactive and billions wasted annually, the focus has moved to identifying "zombie" accounts and redundant functions [7]. Furthermore, as shadow IT still accounts for 30-40% of IT spending, the consolidation trend highlights a security imperative: fewer apps mean a smaller attack surface, which is vital given that nearly half of cyberattacks are linked to unauthorized shadow IT [8].

The primary driver is likely the economic pressure that began in late 2022, forcing CFOs to scrutinize recurring operational expenses more rigorously than before [9]. Simultaneously, major vendors like Microsoft and have bundled more features into their core suites, effectively cannibalizing the market for single-point solutions. We can also speculate that the "AI Boom" is displacing legacy software budget; companies are cutting niche productivity apps to free up funds for expensive GenAI subscriptions, which saw a 75% increase in spending year-over-year [3]. This suggests a "replacement" cycle where low-value legacy apps are being swapped for high-cost AI tools.

The era of unchecked SaaS adoption has ended, replaced by a period of strategic consolidation and high-stakes AI investment. IT Asset Management is no longer just about counting licenses; it is about navigating the "SaaS Paradox" where using fewer tools costs more money. Organizations that fail to centralize their visibility into this new high-cost, high-risk environment risk losing millions to price hikes and unused AI entitlements [10].

The global Information Technology (IT) landscape is undergoing a radical expansion, with worldwide IT spending projected to reach $6.15 trillion in 2026, an increase of 10.8% from 2025 [1]. However, this massive investment is accompanied by a critical operational failure: a profound lack of visibility. According to the Flexera 2024 State of ITAM Report, 53% of IT teams report significant challenges in gaining or maintaining complete visibility of their technology investments [2]. This "visibility gap" prevents organizations from effectively managing costs, mitigating security risks, and ensuring compliance, transforming IT Asset Management (ITAM) from a back-office administrative task into a critical boardroom governance strategy.

Modern ITAM platforms are no longer simple inventory databases; they are complex governance engines required to track assets across hybrid environments, including on-premise hardware, cloud infrastructure, and a sprawling ecosystem of SaaS applications. The operational challenges facing IT leaders today are not merely about tracking where a laptop is located, but about managing the financial and legal risks of a decentralized, rapid-growth technology stack.

Contrary to the belief that the shift to cloud computing would eliminate software audits, vendor scrutiny has intensified. As software publishers transition to complex hybrid licensing models, the financial penalties for non-compliance have escalated. Research indicates that 22% of global IT leaders have paid more than $5 million in audit costs over the past three years, a figure that has risen from 15% in the previous year [2].

The operational challenge lies in the complexity of modern entitlements. ITAM teams must now reconcile traditional device-based licenses with user-based subscriptions and consumption-based cloud metrics. The top vendors initiating these audits remain industry stalwarts like Microsoft, IBM, and Oracle, but SaaS providers are increasingly adopting aggressive audit tactics [3]. For enterprises, this necessitates IT Asset Management Platforms that possess sophisticated license reconciliation engines capable of interpreting complex product use rights automatically.

While organizations invest heavily in audit defense, the most successful ITAM functions are shifting their focus toward cost optimization. However, the operational burden of audit preparation—data gathering, baseline verification, and entitlement mapping—continues to consume disproportionate resources. This detracts from strategic initiatives such as negotiating better contract terms or optimizing cloud spend. The trend is moving toward "audit readiness" rather than "audit defense," requiring real-time compliance data rather than periodic snapshots.

The democratization of IT procurement has led to an explosion of "Shadow IT," where business units and individuals purchase software without IT oversight. It is estimated that nearly half of an average company's digital solutions are the result of Shadow IT [4]. This decentralization creates two primary operational risks: wasted spend and security vulnerabilities.

From a cost perspective, organizations are bleeding budget through redundant applications and unused licenses. Estimates suggest that wasted IT spending remains between 20% and 30% of total tech budgets, with desktop software and SaaS being the primary culprits [2]. Without a centralized platform to detect overlapping toolsets—such as multiple project management tools or redundant video conferencing subscriptions—companies lose leverage in vendor negotiations.

This challenge is particularly acute for high-growth technology sectors. For example, IT Asset Management Platforms for SaaS Companies must prioritize the discovery of API integrations and OAuth tokens. When an employee connects a third-party app to corporate data using their work credentials, they bypass traditional firewalls. If that third-party vendor is breached, the organization is exposed. Therefore, modern ITAM must integrate deeply with Cybersecurity, Privacy & Compliance Software to identify not just what software is owned, but what data that software can access.

A dominant trend in the current market is the convergence of ITAM with FinOps (Cloud Financial Management). As infrastructure shifts from capital expenditure (CapEx) data centers to operating expenditure (OpEx) cloud services, the distinction between "asset management" and "cloud cost management" is blurring. Gartner predicts that by 2025, 50% of organizations will unify Software Asset Management (SAM) and FinOps into a consolidated discipline [5].

This convergence addresses the "Cloud+" reality, where organizations must manage spend across SaaS, software licenses, and hybrid infrastructure simultaneously [6]. Operational challenges here include:

While software and cloud garner significant attention, Hardware Asset Management (HAM) remains a foundational challenge, complicated significantly by remote and hybrid work models. The logistics of deploying, maintaining, and retrieving physical assets from a distributed workforce have introduced new friction points.

For organizations with high employee turnover, the inability to efficiently retrieve hardware represents a significant financial loss and security risk. This is a specific pain point for contingent workforces. IT Asset Management Platforms for Staffing Agencies are now essential for tracking the chain of custody. When a contractor leaves, the organization must ensure the device is locked, the data is wiped, and the physical asset is returned. Failure to execute this lifecycle results in "ghost assets"—devices that appear in the inventory but cannot be accounted for physically.

The security implications of lost hardware are severe. A laptop missing from a secure office is a problem; a laptop missing from a remote contractor’s home is a potential data breach. Consequently, IT Asset Management Platforms for Contractors are evolving to include robust integration with Mobile Device Management (MDM) solutions. These integrations allow for automated remote wiping and geo-fencing, ensuring that even if the physical asset is lost, the intellectual property it contains is secured.

Furthermore, "Bring Your Own Device" (BYOD) policies add another layer of complexity. Managing corporate data on personal devices requires a delicate balance between security and privacy. ITAM platforms must distinguish between corporate-owned assets and employee-owned devices that merely access corporate networks, a distinction that is often blurred in practice [7].

Two major regulatory trends are reshaping the requirements for ITAM platforms: enhanced security standards and sustainability mandates.

ITAM is increasingly viewed as a prerequisite for security compliance frameworks like SOC 2 and ISO 27001. You cannot secure what you do not know you have. SOC 2 compliance specifically requires organizations to demonstrate thorough asset management, including classification, access control, and incident response capabilities for all system components [8]. The 2024 update to the ISO/IEC 19770-1 standard further codifies these requirements, introducing new process areas for enhanced granularity and explicitly incorporating sustainability as a process area [9]. This shifts ITAM from a passive tracking exercise to an active compliance control.

Sustainability is moving from a corporate social responsibility (CSR) initiative to a regulatory requirement. In the European Union, the introduction of the Digital Product Passport (DPP) will mandate the collection of data regarding the origin, materials, and end-of-life handling of electronics [10]. This regulation aims to promote a circular economy by ensuring devices are repaired, reused, or recycled rather than discarded.

For ITAM operations, this means tracking carbon footprints and e-waste metrics alongside financial depreciation. Platforms must now support "Green IT" dashboards that calculate the environmental impact of the IT estate. This includes tracking the energy efficiency of data centers and the lifecycle extension of end-user computing devices. Organizations are increasingly asked to report on these metrics to stakeholders, making data accuracy in HAM a brand reputation issue.

Looking ahead to 2026 and beyond, the role of ITAM will be fundamentally altered by Artificial Intelligence and the rise of "Machine Customers."

Data quality remains the Achilles' heel of ITAM. Inconsistent naming conventions (e.g., "Msft," "Microsoft," "MS Corp") plague inventory databases. By 2026, AI is expected to automate the normalization of this data, cleaning up inconsistencies in hardware models and software titles without human intervention [11]. Furthermore, predictive analytics will transition ITAM from reactive to proactive. Instead of waiting for a server to fail or a license to expire, AI models will forecast maintenance needs and renewal probabilities based on usage patterns.

A profound shift is occurring in who—or what—is consuming IT services. Gartner predicts that by 2026, 20% of inbound customer service contact volume will come from "machine customers"—non-human economic actors (like IoT devices or AI agents) that obtain goods or services [12]. In an ITAM context, this means software agents may autonomously negotiate license upgrades, purchase cloud capacity, or schedule hardware maintenance. ITAM platforms must evolve to govern these autonomous transactions, ensuring that machine-driven purchasing does not violate budget constraints or procurement policies.

The fragmentation of the ITAM market—where organizations use separate tools for SaaS management, cloud costing, and hardware tracking—is unsustainable. The future lies in platform consolidation. IT leaders are expected to move away from multi-tool chaos toward primary platforms that serve as the "single source of truth" for all asset data [11]. This consolidation will likely drive mergers and acquisitions in the ITAM software market, as vendors race to offer a unified "Cloud+" governance solution.

The operational challenges in IT Asset Management today differ vastly from those of a decade ago. The discipline has graduated from spreadsheet-based inventory tracking to a sophisticated governance function essential for financial health and security posture. The visibility gap remains the primary adversary; without seeing the full spectrum of hybrid assets—from physical laptops in a contractor's home to ephemeral containers in the cloud—organizations cannot control costs or secure their data.

To succeed, organizations must leverage ITAM platforms that prioritize integration over isolation. They must bridge the divide between Finance and IT through FinOps, automate the lifecycle of remote hardware, and prepare for a future where assets are managed not just by people, but by intelligent agents. As regulations like the EU's Digital Product Passport and standards like ISO 19770-1 evolve, ITAM will become the central nervous system of the sustainable, secure, and efficient digital enterprise.

| Year | Average App Count |

|---|---|

| 2022 | 130 |

| 2023 | 112 |

| 2024 | 106 |

For the first time in the history of the "SaaS explosion," the sheer volume of applications within corporate tech stacks is shrinking. Data from 2024 indicates that the average number of SaaS applications per company dropped to 106, a continued decline from the peak of 130 applications recorded in 2022 [1] [2]. However, this contraction in volume has not resulted in cheaper IT budgets; conversely, the average SaaS spend per employee surged by nearly 22% in the last year, reaching $4,830 [3] [4].

This trend signifies a maturation of the market where "SaaS Sprawl" is no longer being ignored but actively managed through aggressive consolidation strategies. On a micro level, IT departments are eliminating redundant tools—such as having Trello, Asana, and Monday.com all active within one organization—and standardizing on single platforms to reduce complexity [5]. On a macro level, this represents a pivot toward "SaaS value realization," where companies are willing to pay more for fewer, more powerful tools. The rise in spend despite the drop in app count suggests that vendors are successfully shifting their revenue models from simple seat-based pricing to consumption-based models, often driven by new AI features that command premium fees [6].

This shift is critical because it fundamentally changes the mandate of IT Asset Management (ITAM) platforms from simple discovery to complex cost control. With 53% of SaaS licenses reportedly inactive and billions wasted annually, the focus has moved to identifying "zombie" accounts and redundant functions [7]. Furthermore, as shadow IT still accounts for 30-40% of IT spending, the consolidation trend highlights a security imperative: fewer apps mean a smaller attack surface, which is vital given that nearly half of cyberattacks are linked to unauthorized shadow IT [8].

The primary driver is likely the economic pressure that began in late 2022, forcing CFOs to scrutinize recurring operational expenses more rigorously than before [9]. Simultaneously, major vendors like Microsoft and have bundled more features into their core suites, effectively cannibalizing the market for single-point solutions. We can also speculate that the "AI Boom" is displacing legacy software budget; companies are cutting niche productivity apps to free up funds for expensive GenAI subscriptions, which saw a 75% increase in spending year-over-year [3]. This suggests a "replacement" cycle where low-value legacy apps are being swapped for high-cost AI tools.

The era of unchecked SaaS adoption has ended, replaced by a period of strategic consolidation and high-stakes AI investment. IT Asset Management is no longer just about counting licenses; it is about navigating the "SaaS Paradox" where using fewer tools costs more money. Organizations that fail to centralize their visibility into this new high-cost, high-risk environment risk losing millions to price hikes and unused AI entitlements [10].