Recent market data highlights a decisive shift in the eSignature landscape from simple document signing to "Intelligent Agreement Management" (IAM), driven by the commoditization of basic e-signatures and the rise of Generative AI. While DocuSign and Adobe Document Cloud have both seen revenue growth, the industry leader, DocuSign, has aggressively pivoted to an AI-first platform strategy, amassing over 25,000 IAM customers within months of launch. This trend indicates that the market value has migrated from the act of signing to the extraction of data and automation of workfl

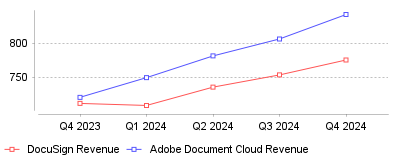

| Calendar Quarter | DocuSign Revenue | Adobe Document Cloud Revenue |

|---|---|---|

| Q4 2023 | 712 | 721 |

| Q1 2024 | 709 | 750 |

| Q2 2024 | 736 | 782 |

| Q3 2024 | 754 | 807 |

| Q4 2024 | 776 | 843 |

The data reveals a bifurcation in the digital document industry where sustainable growth is no longer driven solely by the volume of envelopes sent, but by the intelligence applied to those documents. Specifically, DocuSign’s revenue trajectory shows a return to growth acceleration in late 2024 and 2025, directly correlating with the launch and rapid adoption of its Intelligent Agreement Management (IAM) platform, which grew from zero to over 25,000 enterprise customers in under 18 months [1][2]. Simultaneously, Adobe Document Cloud has consistently outperformed in year-over-year growth (ranging from 17-18%), leveraging its massive ecosystem and AI integration to monetize document workflows beyond simple signatures [3][4].

For the micro-industry, this signals the end of "eSignature" as a standalone software category; it is effectively becoming a feature within broader Contract Lifecycle Management (CLM) and intelligent workflow systems. The rapid uptake of IAM solutions—where AI extracts data from contracts to automate downstream actions—suggests that enterprises are now prioritizing "agreement utility" over simple digitization [5]. On a macro level, this represents a maturing of the SaaS productivity sector, where vendors must layer Generative AI to prevent commoditization. Adobe's ability to generate $843 million in a single quarter from Document Cloud alone proves that integrating PDF management with AI-driven editing and signing creates a compounding revenue moat that specialized competitors struggle to breach without significant pivots [6].

This trend is critical because it addresses the "Agreement Trap"—a phenomenon where businesses digitize contracts but leave the data trapped inside static PDFs, leading to estimated billions in lost economic value [7]. The shift impacts IT purchasing decisions significantly; buyers are no longer looking for the cheapest way to get a signature, but rather for platforms that can ingest agreements into a "system of record" that talks to CRMs like Salesforce [8]. Furthermore, the 25,000+ customer adoption figure for DocuSign IAM validates that companies are willing to pay a premium for AI that can summarize terms, flag risks, and automate verification [9].

The primary driver is likely the maturation of Large Language Models (LLMs), which finally gave software the ability to "read" legal text with high accuracy, transforming static documents into structured data sources without human data entry [10]. Additionally, the post-pandemic normalization of remote work forced providers to find new growth engines as the "COVID bump" in simple e-signature volume flattened out; DocuSign’s stock decline from its 2021 peak forced a strategic reinvention beyond the "sign here" button [7]. Increasing competition from lower-cost providers like PandaDoc, which offer similar basic signing features, likely pressured market leaders to move up-market into complex, high-value enterprise workflows to protect their margins [11].

The data confirms that the eSignature market has evolved into an "Intelligent Agreement" market, where value is derived from AI analytics rather than digital ink. With DocuSign IAM sales on track to represent a double-digit percentage of its subscription business and Adobe Document Cloud growing at nearly 20% annually, the clear takeaway is that the future winner will be the platform that best integrates signing with data extraction and workflow automation [2][3]. Investors and buyers should view standalone e-signature tools as legacy tech, while focusing capital on platforms building "systems of record" for agreements.

Recent market data highlights a decisive shift in the eSignature landscape from simple document signing to "Intelligent Agreement Management" (IAM), driven by the commoditization of basic e-signatures and the rise of Generative AI. While DocuSign and Adobe Document Cloud have both seen revenue growth, the industry leader, DocuSign, has aggressively pivoted to an AI-first platform strategy, amassing over 25,000 IAM customers within months of launch. This trend indicates that the market value has migrated from the act of signing to the extraction of data and automation of workfl

| Calendar Quarter | DocuSign Revenue | Adobe Document Cloud Revenue |

|---|---|---|

| Q4 2023 | 712 | 721 |

| Q1 2024 | 709 | 750 |

| Q2 2024 | 736 | 782 |

| Q3 2024 | 754 | 807 |

| Q4 2024 | 776 | 843 |

The data reveals a bifurcation in the digital document industry where sustainable growth is no longer driven solely by the volume of envelopes sent, but by the intelligence applied to those documents. Specifically, DocuSign’s revenue trajectory shows a return to growth acceleration in late 2024 and 2025, directly correlating with the launch and rapid adoption of its Intelligent Agreement Management (IAM) platform, which grew from zero to over 25,000 enterprise customers in under 18 months [1][2]. Simultaneously, Adobe Document Cloud has consistently outperformed in year-over-year growth (ranging from 17-18%), leveraging its massive ecosystem and AI integration to monetize document workflows beyond simple signatures [3][4].

For the micro-industry, this signals the end of "eSignature" as a standalone software category; it is effectively becoming a feature within broader Contract Lifecycle Management (CLM) and intelligent workflow systems. The rapid uptake of IAM solutions—where AI extracts data from contracts to automate downstream actions—suggests that enterprises are now prioritizing "agreement utility" over simple digitization [5]. On a macro level, this represents a maturing of the SaaS productivity sector, where vendors must layer Generative AI to prevent commoditization. Adobe's ability to generate $843 million in a single quarter from Document Cloud alone proves that integrating PDF management with AI-driven editing and signing creates a compounding revenue moat that specialized competitors struggle to breach without significant pivots [6].

This trend is critical because it addresses the "Agreement Trap"—a phenomenon where businesses digitize contracts but leave the data trapped inside static PDFs, leading to estimated billions in lost economic value [7]. The shift impacts IT purchasing decisions significantly; buyers are no longer looking for the cheapest way to get a signature, but rather for platforms that can ingest agreements into a "system of record" that talks to CRMs like Salesforce [8]. Furthermore, the 25,000+ customer adoption figure for DocuSign IAM validates that companies are willing to pay a premium for AI that can summarize terms, flag risks, and automate verification [9].

The primary driver is likely the maturation of Large Language Models (LLMs), which finally gave software the ability to "read" legal text with high accuracy, transforming static documents into structured data sources without human data entry [10]. Additionally, the post-pandemic normalization of remote work forced providers to find new growth engines as the "COVID bump" in simple e-signature volume flattened out; DocuSign’s stock decline from its 2021 peak forced a strategic reinvention beyond the "sign here" button [7]. Increasing competition from lower-cost providers like PandaDoc, which offer similar basic signing features, likely pressured market leaders to move up-market into complex, high-value enterprise workflows to protect their margins [11].

The data confirms that the eSignature market has evolved into an "Intelligent Agreement" market, where value is derived from AI analytics rather than digital ink. With DocuSign IAM sales on track to represent a double-digit percentage of its subscription business and Adobe Document Cloud growing at nearly 20% annually, the clear takeaway is that the future winner will be the platform that best integrates signing with data extraction and workflow automation [2][3]. Investors and buyers should view standalone e-signature tools as legacy tech, while focusing capital on platforms building "systems of record" for agreements.