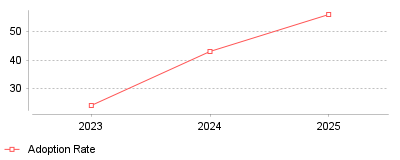

| Year | Adoption Rate |

|---|---|

| 2023 | 24 |

| 2024 | 43 |

| 2025 | 56 |

The data highlights a massive acceleration in the adoption of Artificial Intelligence within sales workflows, transitioning from a niche advantage to a majority standard. According to HubSpot's research, adoption rates among sales representatives jumped from 24% in 2023 to 43% in 2024, with 2025 data from LinkedIn indicating that 56% of sales professionals now use AI daily [1]. Furthermore, McKinsey reports that 65% of organizations are now regularly using generative AI in at least one business function, with marketing and sales leading this charge [2].

This trend signifies a fundamental change in the "Revenue Intelligence" software category: platforms are evolving from descriptive analytics (showing what happened) to agentic workflows (doing the work). In the micro view, individual sellers are offloading administrative tasks—which traditionally consumed up to 75% of their time—to AI agents that can automate research and data entry [3]. On a macro industry level, this creates a performance bifurcation; Gartner found that sellers who effectively partner with AI tools are 3.7 times more likely to meet their quotas than those who do not [4]. Consequently, software vendors are rapidly consolidating point solutions into unified "revenue platforms" that combine forecasting, conversation intelligence, and auto-execution to capture this value [5].

The implications for revenue efficiency are critical, as early AI deployments in sales have been shown to boost win rates by over 30% [3]. As B2B buying cycles stretch longer and budgets tighten, the ability to process signals and personalize outreach at scale is becoming the primary differentiator between growth and stagnation. Additionally, forecast accuracy—a historical pain point for revenue leaders—has seen improvements of up to 10x in companies utilizing AI to crunch deal data rather than relying on manual rep inputs [6].

The primary driver is the commoditization and accessibility of Large Language Models (LLMs), which lowered the technical barrier for sales teams to use advanced intelligence without needing data scientists. Simultaneously, economic pressure to "do more with less" has forced Revenue Operations (RevOps) leaders to seek technology that offers immediate productivity gains rather than just better reporting [7]. The shift was further accelerated by the realization that manual CRM data entry was unreliable; automating data capture through AI became the only way to ensure the data quality necessary for accurate forecasting [8].

We have crossed the chasm from AI experimentation to essential reliance in sales intelligence. The data suggests that by the end of 2025, AI integration will be "table stakes," with the market penalizing organizations that rely solely on intuition-based selling. The prominent takeaway is that the "AI Advantage" is real and quantifiable: a 3.7x higher probability of hitting quota isn't just an incremental improvement—it is a competitive necessity.

The separation between sales intelligence data and revenue execution workflow has collapsed. For the better part of a decade, organizations maintained distinct budgets for data providers (finding the contact) and revenue operations platforms (managing the deal). That dichotomy ended in late 2025 when Clari and Salesloft finalized their merger, creating a singular entity managing $10 trillion in revenue data [1]. This consolidation signals the maturity of the Business Intelligence & Analytics Software sector, specifically within revenue operations, where buyers no longer tolerate fragmented point solutions.

The market for sales intelligence software reached $3.31 billion in 2024 and is on a trajectory to hit $9.02 billion by 2034 [2]. Simultaneously, the revenue operations (RevOps) software sector, valued at $4.39 billion in 2024, is accelerating at a 16.6% CAGR [3]. These growth rates mask a turbulent operational reality: while spending increases, effectiveness often lags. Organizations face a trifecta of pressures—accelerating data decay, strict liability for AI agents, and a mandated consolidation of the sales technology stack. This analysis explores the operational friction points defining the Revenue Analytics & Sales Intelligence Software market in 2026.

The foundational asset of sales intelligence—the contact record—is deteriorating faster than most organizations can repair it. In 2024, B2B contact data decayed at an annualized rate of up to 70.3%, depending on the industry and role volatility [4]. More alarmingly, specific segments saw unprecedented spikes in obsolescence; email address decay hit 3.6% in a single month in late 2024 [5]. This acceleration stems from increased job mobility, corporate restructuring, and the widespread adoption of AI-based email filters that invalidate traditional verification methods.

The financial penalty for ignoring this erosion is severe. Poor data quality costs the average organization $12.9 million annually [6]. For a mid-sized enterprise, this manifests in wasted marketing spend and lower seller productivity. Sales representatives spend only 36.6% of their time selling; the remainder is consumed by administrative tasks, including verifying incorrect data in CRM systems [7]. When inaccurate data enters the forecasting model, the downstream effects include missed guidance and misallocated resources. Modern forecast accuracy and pipeline analytics tools now require continuous, automated hygiene layers rather than periodic manual cleansing to remain viable.

The era of the disconnected sales stack is over. In 2024, 66% of sales representatives reported feeling overwhelmed by the number of tools required to close a deal [8]. This tool fatigue drove a massive shift toward platform consolidation in 2025. Buyers now prefer single vendors that can handle the entire revenue lifecycle—from prospecting to forecasting—rather than stitching together disparate applications.

The merger of Clari and Salesloft in December 2025 exemplifies this shift. By combining Clari's forecasting rigor with Salesloft's engagement capabilities, the new entity addresses the full "Revenue Action Orchestration" spectrum [1]. This aligns with Gartner’s new categorization of Revenue Action Orchestration platforms, where vendors like Gong and Outreach also secured Leader positions by demonstrating they could unify data signals with execution workflows [9]. For revenue analytics platforms for RevOps teams, the value proposition has moved from "visibility" to "control." It is no longer enough to see the revenue leak; the platform must automatically trigger the actions to plug it.

As revenue platforms integrate generative AI agents to automate outreach and negotiation, organizations face new liability frontiers. The legal precedent set in the 2024 Air Canada case established that companies are liable for the "hallucinations" or incorrect promises made by their AI chatbots [10]. The tribunal rejected the defense that the chatbot was a "separate legal entity," forcing the airline to pay damages for a fabricated bereavement fare policy [11].

This ruling has profound implications for B2B sales. If an autonomous sales agent promises a discount, service level agreement (SLA), or contract term that does not exist, the vendor may be legally bound to honor it. With 40% of software expected to use task-specific AI agents by 2026, the risk surface has expanded [12]. Hallucinations in procurement bots have already generated phantom vendor contracts, creating fraud risks and unauthorized spending [13]. Consequently, revenue analytics platforms for SaaS companies must now include rigorous "guardrails" and audit trails to verify AI-generated communications before they reach the buyer.

Data privacy regulations have transitioned from a compliance checklist to a direct cost of doing business. The General Data Protection Regulation (GDPR) and California Consumer Privacy Act (CCPA) have fundamentally altered how B2B data providers collect and sell information. In 2024, ZoomInfo agreed to a $29.55 million settlement to resolve class action claims regarding its use of personal information in California, Illinois, Indiana, and Nevada [14]. This settlement underscores the legal exposure inherent in scraping or aggregating professional profiles without explicit consent.

The operational challenge for revenue teams is twofold. First, they must ensure their data providers indemnification against privacy claims. Second, they must navigate a shrinking pool of compliant third-party data. The enforcement of these laws has led to a 20% drop in algorithm precision for some analytics models due to restricted data sharing [15]. Successful revenue leaders are responding by investing in first-party data strategies and platforms that can model intent without relying solely on third-party cookies or non-compliant scraped data.

Despite the operational headwinds, the financial performance of top-tier vendors demonstrates the sector's resilience. Gong surpassed $300 million in Annual Recurring Revenue (ARR) by early 2025, driven by a 50% increase in the usage of its AI capabilities [16]. Similarly, ZoomInfo reported Q4 2024 revenue of $309 million with an adjusted operating income margin of 37%, although it faces challenges in the small business segment [17]. The stark divergence in net revenue retention (NRR)—with some platforms struggling to maintain 90% while others expand—indicates that customers are ruthlessly cutting tools that cannot prove immediate ROI.

The "Revenue Leak" crisis remains a primary driver for software investment. RevOps leaders report losing 26% of annual revenue due to breakdowns in the revenue process, such as slipped deals or missed upsell opportunities [18]. Platforms that frame their value proposition around stopping this leak—rather than just "providing insights"—are capturing the majority of enterprise budget.

The role of Revenue Operations has shifted from back-office support to strategic executive function, and compensation structures have evolved to reflect this. In 2025, the median total compensation for RevOps professionals reached approximately $129,000, with directors and specialized AI-Ops roles commanding salaries between $187,000 and $300,000 [19]. A significant trend is the introduction of variable pay; 64% of RevOps leaders now have performance-based incentives tied to revenue outcomes [20].

However, an "AI divide" has emerged in the talent market. RevOps professionals capable of building and managing AI workflows earn up to $60,000 more than their generalist peers [21]. Organizations struggle to find talent that possesses both the technical acumen to manage complex tech stacks and the strategic vision to align sales, marketing, and customer success. This skills gap is a critical bottleneck; without capable operators, even the most sophisticated revenue software fails to deliver value.

Looking toward 2027, the market is moving toward "Autonomous Revenue Systems" where human sellers collaborate with AI agents that handle the majority of administrative and top-of-funnel work. Gartner predicts that by 2028, 60% of B2B seller work will be executed through conversational user interfaces via generative AI sales technologies [22].

Success in this new environment requires a rigorous focus on data hygiene and governance. As AI agents take more autonomous actions, the quality of the underlying data becomes the primary safety mechanism. Organizations that solve the data decay problem and consolidate their tech stacks into unified execution platforms will see non-linear productivity gains. Those that fail to modernize will find themselves managing liability rather than revenue.

| Year | Adoption Rate |

|---|---|

| 2023 | 24 |

| 2024 | 43 |

| 2025 | 56 |

The data highlights a massive acceleration in the adoption of Artificial Intelligence within sales workflows, transitioning from a niche advantage to a majority standard. According to HubSpot's research, adoption rates among sales representatives jumped from 24% in 2023 to 43% in 2024, with 2025 data from LinkedIn indicating that 56% of sales professionals now use AI daily [1]. Furthermore, McKinsey reports that 65% of organizations are now regularly using generative AI in at least one business function, with marketing and sales leading this charge [2].

This trend signifies a fundamental change in the "Revenue Intelligence" software category: platforms are evolving from descriptive analytics (showing what happened) to agentic workflows (doing the work). In the micro view, individual sellers are offloading administrative tasks—which traditionally consumed up to 75% of their time—to AI agents that can automate research and data entry [3]. On a macro industry level, this creates a performance bifurcation; Gartner found that sellers who effectively partner with AI tools are 3.7 times more likely to meet their quotas than those who do not [4]. Consequently, software vendors are rapidly consolidating point solutions into unified "revenue platforms" that combine forecasting, conversation intelligence, and auto-execution to capture this value [5].

The implications for revenue efficiency are critical, as early AI deployments in sales have been shown to boost win rates by over 30% [3]. As B2B buying cycles stretch longer and budgets tighten, the ability to process signals and personalize outreach at scale is becoming the primary differentiator between growth and stagnation. Additionally, forecast accuracy—a historical pain point for revenue leaders—has seen improvements of up to 10x in companies utilizing AI to crunch deal data rather than relying on manual rep inputs [6].

The primary driver is the commoditization and accessibility of Large Language Models (LLMs), which lowered the technical barrier for sales teams to use advanced intelligence without needing data scientists. Simultaneously, economic pressure to "do more with less" has forced Revenue Operations (RevOps) leaders to seek technology that offers immediate productivity gains rather than just better reporting [7]. The shift was further accelerated by the realization that manual CRM data entry was unreliable; automating data capture through AI became the only way to ensure the data quality necessary for accurate forecasting [8].

We have crossed the chasm from AI experimentation to essential reliance in sales intelligence. The data suggests that by the end of 2025, AI integration will be "table stakes," with the market penalizing organizations that rely solely on intuition-based selling. The prominent takeaway is that the "AI Advantage" is real and quantifiable: a 3.7x higher probability of hitting quota isn't just an incremental improvement—it is a competitive necessity.