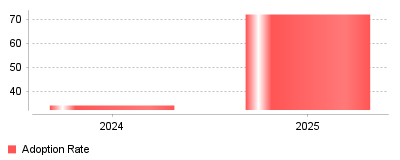

Recent data reveals a seismic shift in the financial technology landscape, marking a decisive "tipping point" for Artificial Intelligence adoption within the Office of the CFO. Specifically, the utilization of AI tools by finance leaders for core functions like cash flow forecasting and process automation has more than doubled in just twelve months, surging from 34% in 2024 to 72% in 2025. This explosion in adoption is mirrored by a massive 49.7% year-over-year increase in venture capital funding for CFO tech stack startups, indicating that automated, predictive budgeting is r

| Year | Adoption Rate |

|---|---|

| 2024 | 34 |

| 2025 | 72 |

According to the 2025 Global Finance Trends Survey by Protiviti, the percentage of CFOs and finance leaders employing AI tools has more than doubled in a single year, jumping from 34% in 2024 to 72% in 2025 [1]. This massive spike in adoption is not merely experimental; the data indicates that 58% of these leaders are specifically applying AI to financial forecasting and 66% to process automation [2]. Furthermore, investment capital is chasing this demand, with funding for "CFO Stack" startups in the U.S. rising by nearly 50% to $5.54 billion in 2025 [3].

This trend signifies that the finance industry has crossed the chasm from "cautious observation" to "strategic integration." For decades, cash flow forecasting was synonymous with manual spreadsheets—a method prone to human error and data silos. The rapid climb to 72% adoption suggests that AI-driven tools are no longer viewed as futuristic novelties but as essential infrastructure for the modern enterprise [4]. On a macro level, this indicates a widespread digitization of the "Office of the CFO," where reliance on historical data is being replaced by predictive, real-time modeling. For mid-market companies specifically, this democratizes access to sophisticated treasury tools that were previously accessible only to large conglomerates [5].

The implications for accuracy and risk management are profound. Traditional manual forecasting methods often result in error rates that can jeopardize liquidity; conversely, AI-powered models have been shown to reduce these error rates by up to 50% [6]. In an environment where 43% of mid-market companies have historically relied on unreliable forecasts that lead to cash shortfalls [7], the ability to automate data ingestion from ERPs and bank feeds offers a critical safety net. This shift allows finance teams to pivot from data entry to strategic analysis, enhancing their ability to navigate economic volatility.

Several converging factors likely triggered this aggressive adoption curve. First, persistent global economic volatility and fluctuating interest rates have made static spreadsheets insufficient for managing liquidity risk [8]. Second, the maturity of Generative AI has lowered the technical barrier to entry, allowing finance professionals to interact with complex data using natural language rather than coding [2]. Finally, the "Trust Gap" is closing; as major institutions like JPMorgan validate these tools with significant success stories—such as saving clients thousands of hours in manual work—hesitant CFOs are feeling the pressure to modernize to remain competitive [9].

The doubling of AI adoption in just twelve months marks the end of the spreadsheet-dominant era for cash flow management. Finance leaders who fail to integrate these tools face a competitive disadvantage, burdened by slower reaction times and higher operational costs. The prominent takeaway is that AI in financial forecasting has graduated from a "nice-to-have" to a "must-have," with the market punishing those who cannot predict their liquidity with algorithmic precision.

The landscape of corporate finance is undergoing a structural transformation, driven by economic volatility and rapid technological advancement. Cash flow forecasting and budgeting—once periodic, compliance-driven exercises—have evolved into critical strategic capabilities. As organizations navigate high interest rates, inflationary pressures, and supply chain disruptions, the demand for precision in liquidity management has never been higher. The market for Cash Flow Forecasting & Budgeting Tools is projected to grow significantly, with estimates suggesting a rise from $1.34 billion in 2024 to over $1.5 billion by 2025 [1]. This growth reflects a broader shift within the Accounting & Finance Software sector, moving from historical reporting to predictive analytics.

Operational challenges, however, remain pervasive. Despite the availability of sophisticated tools, a significant portion of finance teams continue to rely on fragmented data and manual processes. This report analyzes the current state of the industry, highlighting the operational bottlenecks impeding financial agility and the emerging technologies reshaping how businesses predict their financial future.

A fundamental operational challenge in modern financial planning is the continued reliance on spreadsheets. While familiar and flexible, manual spreadsheet-based forecasting is increasingly viewed as a liability in a high-speed business environment. Research indicates that approximately 94% of business spreadsheets contain critical errors that risk financial losses and operational mistakes [2]. Furthermore, finance teams spend a disproportionate amount of time on data collection rather than analysis. It is estimated that using spreadsheets to analyze global cash positions consumes nearly 1,300 hours per year for some teams, a massive drain on resources that could be allocated to strategic decision-making [3].

The operational risk is compounded by the static nature of spreadsheet data. In an era where market conditions change daily, monthly or quarterly forecasts based on manual inputs are often obsolete by the time they are finalized. Leading organizations are transitioning toward automated solutions to mitigate these risks, yet adoption barriers remain. The challenge for many CFOs is not merely selecting a tool but orchestrating the cultural and operational shift away from legacy manual workflows to integrated, automated systems.

The accuracy of a cash flow forecast is directly proportional to the quality and timeliness of the data it consumes. A major hurdle for mid-market and enterprise organizations is the "data silo" problem, where critical financial information is trapped within disparate systems—CRM, ERP, bank portals, and billing platforms. Without a unified view, creating a reliable forecast is virtually impossible.

To address this, there is a surging demand for Cash Flow Forecasting Tools with Bank Feed Integrations. These solutions automate the ingestion of transaction data, allowing for real-time reconciliation and visibility into cash positions across multiple entities and currencies. By eliminating manual CSV exports and bank statement reconciliation, finance teams can reduce the latency between a transaction occurring and it being reflected in the forecast. This capability is crucial for liquidity management, ensuring that decision-makers are working with "cash in bank" reality rather than accounting abstractions [4].

The integration of bank feeds also facilitates the move toward direct method forecasting (tracking actual cash inflows and outflows) rather than relying solely on the indirect method (adjusting net income). This shift provides a more granular and accurate picture of short-term liquidity, which is essential for managing working capital during periods of economic stress.

While the need for accurate forecasting is universal, the specific operational levers vary significantly across industries. Generalist tools often fail to capture the nuances of distinct business models, driving the adoption of specialized solutions.

For software-as-a-service (SaaS) companies, cash flow forecasting is inextricably linked to recurring revenue metrics. The primary challenge here is accurately modeling churn and its compound effect on future cash flows. A simple linear projection of Annual Recurring Revenue (ARR) fails to account for the volatility of customer retention. In 2025, the average churn rate for B2B SaaS is projected to be around 4.9%, but this varies wildly by contract term and company size [5].

Operational leaders in this space require Cash Flow Forecasting Tools for Subscription and SaaS Companies that can integrate with billing engines (like Stripe or Chargebee) to automate the calculation of metrics such as Net Revenue Retention (NRR) and Customer Lifetime Value (LTV). Forecasting tools must effectively distinguish between bookings (contract signed) and collections (cash received), a discrepancy that often leads to "liquidity mirages" where a company appears profitable on an accrual basis but faces a cash crunch due to payment delays or high churn [6].

E-commerce businesses face a distinct set of cash flow challenges centered on the cash conversion cycle. The delay between paying suppliers for inventory and receiving cash from customers creates a working capital gap that must be carefully managed. Overstocking leads to "frozen" cash sitting on warehouse shelves, while understocking results in missed revenue opportunities. In 2026, inventory-related cash flow challenges, including overstocking and rising shipping costs, are expected to be primary threats to online retailers [7].

To navigate this, merchants are turning to Cash Flow Forecasting Tools for E-Commerce and Inventory Businesses. These tools ingest data from platforms like Shopify or Amazon Seller Central to predict sales seasonality and inventory depletion rates. By correlating sales forecasts with supplier lead times and payment terms, these systems help businesses optimize their purchasing schedules, ensuring liquidity is not unnecessarily tied up in slow-moving stock [8].

Service-based businesses, such as digital agencies and consultancies, operate in a "lumpy" cash flow environment. Revenue is often tied to project milestones or net-30/60 payment terms, making monthly inflows unpredictable. A common operational mistake in this sector is overestimating revenue timing—assuming a project will close and pay out in Q1 when it may slip to Q2 [4].

Agencies require Cash Flow Forecasting Tools for Agencies and Services Firms that bridge the gap between project management and finance. These tools often integrate with time-tracking and project management software to forecast billing based on resource utilization and project progress. This visibility allows agency owners to foresee "cash valleys" between major project payments and manage payroll obligations accordingly.

Artificial Intelligence (AI) and Machine Learning (ML) are redefining the benchmarks for forecasting accuracy. Traditional variance analysis looks backward to explain why a forecast was wrong; AI looks forward to identify patterns that humans might miss. By analyzing vast historical datasets, ML algorithms can identify non-linear correlations between cash flow and external factors such as seasonality, macroeconomic indicators, and customer payment behaviors [9].

Research suggests that AI-powered forecasting models can reduce error rates by up to 50% compared to traditional statistical methods [10]. These systems are particularly effective at predicting Accounts Receivable (AR) timing. Instead of assuming a standard "Net 30" collection period for all clients, AI tools analyze the specific payment history of each customer to predict the exact date funds are likely to settle. This granular level of detail transforms cash flow management from a defensive posture to a proactive strategic advantage [11].

Furthermore, AI facilitates dynamic budgeting. Traditional static budgets often become obsolete the moment they are finalized due to market shifts. AI enables "rolling forecasts" that continuously update based on real-time data, allowing organizations to reallocate resources dynamically. This agility is essential in the current economic climate where 2025 forecasts must account for fluctuating interest rates and potential supply chain disruptions [12].

As economic volatility becomes the "new normal," the ability to stress-test financial plans is no longer optional. Operational challenges in 2024 and 2025 include high interest rates, inflationary pressures on expenses, and unpredictable consumer spending [13]. Businesses that rely on a single "base case" forecast are vulnerable to external shocks.

This has driven the adoption of Cash Flow Forecasting Tools with Scenario and What-If Modeling. These platforms allow finance teams to run multiple simulations—such as "Best Case," "Worst Case," and "Recession Case"—in parallel. Users can adjust variables like sales growth, churn rate, or supplier costs to visualize the impact on cash reserves. For example, a CFO can instantly model the impact of a 10% increase in raw material costs or a 5% drop in customer retention.

Scenario planning transforms the forecast from a static document into a strategic playbook. By identifying the break-even points and liquidity thresholds for various scenarios, businesses can establish contingency plans (e.g., delaying capital expenditures or securing a line of credit) before a crisis hits [14].

The efficacy of any forecasting tool is ultimately limited by its integration with the core accounting system (General Ledger). Disconnected tools require manual data imports, which introduces latency and the risk of transcription errors. Modern best practices dictate that forecasting modules should have a seamless, bi-directional sync with the ERP or accounting software.

For small to mid-sized businesses (SMBs), Cash Flow Forecasting Tools Integrated with Accounting Software like Xero, QuickBooks, or NetSuite are essential. These integrations ensure that the forecast is built on the same "source of truth" as the financial statements. When a bill is paid or an invoice is issued in the accounting system, the cash flow forecast is updated automatically. This synchronization reduces the administrative burden on finance teams and ensures that stakeholders are always viewing the most current financial position [15].

The operational shift toward automated, AI-driven forecasting has profound business implications. Firstly, it enhances liquidity risk management. With only 28% of companies currently achieving cash forecasts within 10% accuracy, there is significant room for improvement [16]. Accurate forecasting reduces the need for excessive cash buffers, allowing capital to be deployed more efficiently into growth initiatives or debt reduction.

Secondly, it elevates the role of the finance function. By automating low-value tasks like data entry and reconciliation, finance professionals can focus on strategic business partnering. They transform from "scorekeepers" into strategic advisors who provide forward-looking insights that drive business growth. In fact, 83% of businesses using advanced forecasting tools report having better relationships with their banks and easier access to credit, as lenders have greater confidence in their financial visibility [17].

However, the transition is not without challenges. Implementing these tools requires a clean data foundation. If the underlying data in the ERP or CRM is inaccurate ("garbage in"), the AI forecast will be equally flawed ("garbage out"). Therefore, the adoption of advanced forecasting tools often necessitates a broader data governance initiative to ensure data hygiene across the organization [18].

Looking ahead to 2025 and 2026, the convergence of AI, open banking, and cloud computing will continue to accelerate. We can expect forecasting tools to become increasingly autonomous. Rather than just predicting cash shortages, future systems will likely recommend and even execute corrective actions, such as initiating a transfer from a line of credit or sending automated payment reminders to late-paying customers [11].

The market for these services is predicted to expand at a Compound Annual Growth Rate (CAGR) of over 12% through 2025 [1]. This growth will be fueled by the democratization of enterprise-grade features. Capabilities like Monte Carlo simulations and machine learning, once accessible only to large corporations with dedicated treasury teams, are becoming available to SMBs through intuitive SaaS platforms.

Furthermore, the scope of forecasting is expanding beyond pure finance. "Integrated Business Planning" (IBP) is gaining traction, where cash flow forecasts are tightly coupled with operational plans for HR, sales, and supply chain. This holistic approach ensures that financial goals are aligned with operational realities, reducing the friction between departments and creating a more resilient organization [19].

In conclusion, the operational challenges in cash flow forecasting are shifting from problems of calculation to problems of integration and interpretation. The tools available today offer unprecedented visibility and predictive power. The competitive advantage in the coming years will belong to organizations that successfully leverage these tools to navigate uncertainty, turning cash flow forecasting from a back-office burden into a strategic asset.

Recent data reveals a seismic shift in the financial technology landscape, marking a decisive "tipping point" for Artificial Intelligence adoption within the Office of the CFO. Specifically, the utilization of AI tools by finance leaders for core functions like cash flow forecasting and process automation has more than doubled in just twelve months, surging from 34% in 2024 to 72% in 2025. This explosion in adoption is mirrored by a massive 49.7% year-over-year increase in venture capital funding for CFO tech stack startups, indicating that automated, predictive budgeting is r

| Year | Adoption Rate |

|---|---|

| 2024 | 34 |

| 2025 | 72 |

According to the 2025 Global Finance Trends Survey by Protiviti, the percentage of CFOs and finance leaders employing AI tools has more than doubled in a single year, jumping from 34% in 2024 to 72% in 2025 [1]. This massive spike in adoption is not merely experimental; the data indicates that 58% of these leaders are specifically applying AI to financial forecasting and 66% to process automation [2]. Furthermore, investment capital is chasing this demand, with funding for "CFO Stack" startups in the U.S. rising by nearly 50% to $5.54 billion in 2025 [3].

This trend signifies that the finance industry has crossed the chasm from "cautious observation" to "strategic integration." For decades, cash flow forecasting was synonymous with manual spreadsheets—a method prone to human error and data silos. The rapid climb to 72% adoption suggests that AI-driven tools are no longer viewed as futuristic novelties but as essential infrastructure for the modern enterprise [4]. On a macro level, this indicates a widespread digitization of the "Office of the CFO," where reliance on historical data is being replaced by predictive, real-time modeling. For mid-market companies specifically, this democratizes access to sophisticated treasury tools that were previously accessible only to large conglomerates [5].

The implications for accuracy and risk management are profound. Traditional manual forecasting methods often result in error rates that can jeopardize liquidity; conversely, AI-powered models have been shown to reduce these error rates by up to 50% [6]. In an environment where 43% of mid-market companies have historically relied on unreliable forecasts that lead to cash shortfalls [7], the ability to automate data ingestion from ERPs and bank feeds offers a critical safety net. This shift allows finance teams to pivot from data entry to strategic analysis, enhancing their ability to navigate economic volatility.

Several converging factors likely triggered this aggressive adoption curve. First, persistent global economic volatility and fluctuating interest rates have made static spreadsheets insufficient for managing liquidity risk [8]. Second, the maturity of Generative AI has lowered the technical barrier to entry, allowing finance professionals to interact with complex data using natural language rather than coding [2]. Finally, the "Trust Gap" is closing; as major institutions like JPMorgan validate these tools with significant success stories—such as saving clients thousands of hours in manual work—hesitant CFOs are feeling the pressure to modernize to remain competitive [9].

The doubling of AI adoption in just twelve months marks the end of the spreadsheet-dominant era for cash flow management. Finance leaders who fail to integrate these tools face a competitive disadvantage, burdened by slower reaction times and higher operational costs. The prominent takeaway is that AI in financial forecasting has graduated from a "nice-to-have" to a "must-have," with the market punishing those who cannot predict their liquidity with algorithmic precision.